RBA gives borrowers’ home buying budgets a boost of up to $71,000

The maximum amount the average Australian can borrow from the bank for a mortgage has jumped by an estimated $36,000 this year, after the three cash rate cuts from the RBA since February.

For a couple, both earning the average wage, their maximum borrowing capacity has increased by an estimated $71,000.

This analysis is based on the average full-time wage of $104,807, as recorded by the ABS.

← Mobile/tablet users, scroll sideways to view full table →

| Potential increase in maximum borrowing capacity after three cash rate cuts this year | |||

|---|---|---|---|

| Max borrowing capacity – Jan | Max borrowing capacity – today | Increase | |

| Single (av. wage) | $509,000 | $545,000 | +$36,000 |

| Couple (both on av. wage) | $1,019,000 | $1,090,000 | +$71,000 |

Source: Canstar.com.au. Based on an owner-occupier taking out a 30 year loan at the estimated average RBA new customer variable rates. Assumes $24k in expenses for the single person, $48k for the couple, no other debts, no dependents, average wage based on ABS data for May 2025 and assumes the person has not had a pay rise in this time. See full notes below.

What does this mean for potential buyers in each capital city?

Potential home buyers might see a boost to the maximum amount a bank will lend them with each rate cut, however, this doesn’t automatically mean they can afford the property they’re hoping to buy.

Canstar analysis of Cotality median property price data shows a single person earning the average wage still can’t afford the median-priced house in any capital city except Darwin, even with a 20% deposit.

A couple, both earning the average wage, could potentially afford a house in all capital cities with the exception of Sydney, assuming they have a 20% deposit, which is no mean feat in itself.

Can the average Australian afford a median-priced house in each capital city?

← Mobile/tablet users, scroll sideways to view full table →

| Median price house | Deposit (20%) | Single | Couple | |

|---|---|---|---|---|

| Sydney | $1,525,956 | $305,191 | ❌ | ❌ |

| Melbourne | $952,339 | $190,468 | ❌ | ✓ |

| Brisbane | $1,019,865 | $203,973 | ❌ | ✓ |

| Adelaide | $895,726 | $179,145 | ❌ | ✓ |

| Perth | $869,689 | $173,938 | ❌ | ✓ |

| Hobart | $714,691 | $142,938 | ❌ | ✓ |

| Canberra | $984,723 | $196,945 | ❌ | ✓ |

| Darwin | $641,997 | $128,399 | ✓ | ✓ |

Source: Canstar. Notes: based on borrowing capacity calculations above and median house price data from Cotality from July 2025. Assumes a 20% deposit.

Can the average Australian afford a median-priced apartment in each capital city?

← Mobile/tablet users, scroll sideways to view full table →

| Median price unit | Deposit (20%) | Single | Couple | |

|---|---|---|---|---|

| Sydney | $868,341 | $173,668 | ❌ | ✓ |

| Melbourne | $621,281 | $124,256 | ❌ | ✓ |

| Brisbane | $727,110 | $145,422 | ❌ | ✓ |

| Adelaide | $611,471 | $122,294 | ✓ | ✓ |

| Perth | $615,528 | $123,106 | ✓ | ✓ |

| Hobart | $552,352 | $110,470 | ✓ | ✓ |

| Canberra | $591,570 | $118,314 | ✓ | ✓ |

| Darwin | $390,863 | $78,173 | ✓ | ✓ |

Source: Canstar. Notes: based on borrowing capacity calculations above and median unit price data from Cotality from July 2025. Assumes a 20% deposit.

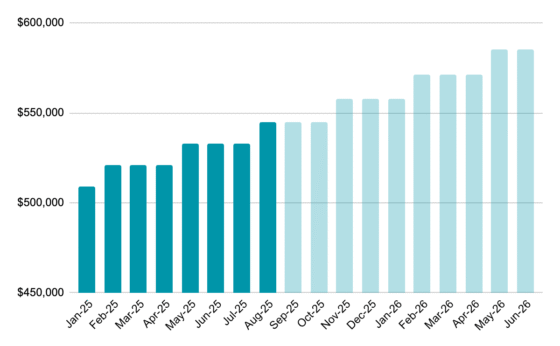

How much more can the average Australian borrow if we see further RBA cuts?

Should we get three more cuts in this cycle, as Westpac is predicting, then a single person on the average wage could see their maximum borrowing capacity increase by an estimated $76,000 through to mid-next year. This assumes the banks pass on each cut in full to new customer variable rates.

Another three rate cuts through to mid-next year is not a given. While the RBA has said at least one more cut is likely, economists are split on exactly how many that might be, with CBA and ANZ saying just one more cut in November, NAB expecting two more – one in November and another in February, while Westpac has the most cuts penciled in out of the big bank economic teams with three in November, February and May of next year.

Potential boost to borrowing capacity for the average person if we see three more cash rate cuts

- Feb + May + Aug + 1 more cut = +$49,000

- Feb + May + Aug + 2 more cuts = +$62,000

- Feb + May + Aug + 3 more cuts = +$76,000

Borrowing capacity notes apply.

Potential impact of RBA rate cut on maximum borrowing capacity for a single person on the average wage after a total of 6 cash rate cuts

Source: Canstar. Notes: based on the maximum borrowing capacity of someone on the average wage after the February. May, August rate cuts and three more rate cuts based on Westpac’s current cash rate forecast.

Couples are the biggest winners from borrowing power boost

Canstar data insights director, Sally Tindall, says: “Three rate cuts in six months have given home buyers a sizable leg-up, adding tens of thousands of dollars to what banks may be willing to lend. For a couple on the average wage, that’s around $71,000 more borrowing power than they had in January – a huge shift in such a short space of time.”

“While it’s tempting to see this as a green light to borrow more, remember it’s not free money, and taking on a big debt, even if the bank says it’s OK, doesn’t necessarily mean it’s the right decision for you.

“Even with this boost, singles on an average wage are still locked out of buying a median-priced house across most markets. Borrowing power might be rising, but in cities like Sydney and Melbourne, prices are still running ahead of people’s pay packets.

“Couples have a greater chance of getting a house that comes with a patch of grass, but in many cities they’re still going to have to sign on to an eye-watering amount of debt if they don’t have a decent deposit.

“If Westpac’s forecast of three more cuts plays out, the average single could have $76,000 more borrowing capacity by the middle of next year. That’s welcome news for buyers, but it also risks pouring more fuel on already-hot property prices.”

Notes on borrowing calculations: calculations are based on the current new owner-occupier variable rate of 6.00% which reduces by 0.25% pts, a loan term of 30 years, annual expenses of $24,000 for singles and $48,000 for couples, 90% of post-tax income available to service the loan and expenses, and a 3.00% interest rate buffer. Tax calculations based on the current financial year, excluding Medicare Levy. Assumes borrowers have no existing debts, minimal expenses and no dependents. Average wage is based on the ABS average full time ordinary time earnings wage of $103,024 p.a. and does not factor in pay rises. Borrowers should seek personal financial advice before deciding how much to borrow and know the actual amount will vary depending on their personal circumstances and between lenders.

This article was reviewed by our Editor-in-Chief Nina Rinella before it was updated, as part of our fact-checking process.