How do corporate bonds work?

Australian Corporate Bond Company’s CEO Richard Murphy talks through the basics of investing in corporate bonds.

Most investors are familiar with the concept of diversification, or to quote an industry maxim, the notion of not having all your eggs in one basket. In other words, a diversified investment portfolio is typically spread across different asset classes. It often includes growth assets, such as shares and property, as well as defensive assets, such as fixed-income assets like corporate bonds and cash.

Since the Global Financial Crisis (GFC) some Australian investors have relied heavily on term deposits (TDs) for their defensive exposure. However, with rates now at their lowest since records began, numerous lenders have lowered their term deposit rates.

Fixed-income assets, such as bonds, are defensive and can play an anchoring role in a diversified portfolio, so their addition to a portfolio can reduce the expected variability of the portfolio returns over time. Regular interest payments can provide a steady and predictable source of income – and at the end of the bond’s term, the face value is generally returned to the holder.

Corporate bonds share many characteristics with other types of bonds. The main differentiator is that they are issued by companies rather than governments or statutory bodies.

Why do companies issue bonds?

There are times when companies need to raise money – whether it’s to fund an acquisition, upgrade technology, or new product development – few companies have the balance sheet to grow and innovate without some form of capital raising. Australian companies generally raise capital in two ways – via equity or debt.

Equity finance

Shares fall into the category of equity finance; this includes ordinary shares, preference shares, rights issues and other forms of capital raising in the equity market. Shares represent a proportional ownership stake in a company in exchange for capital. Unlike debt finance, the capital raised from the sale of equity does not need to be repaid. On the other hand, raising capital through equity puts ownership of the business into the hands of shareholders, who in return expect a share of the company’s profits.

Debt finance

Bonds and bank loans both fall into this category; the company borrows a sum of money, commits to repaying it at the end of a specified term, and makes interest payments along the way.

Although the terms of a bank loan may vary for each company, banks generally require companies to comply with a variety of terms to qualify for the loan.

From an investment perspective:

- Share investors OWN companies, bond investors are OWED money by companies.

- Share investors seek a return ON their capital; bond investors seek a return OF their capital and interest payments.

Related article: 4 Ways to Buy Bonds in Australia

How do corporate bonds work?

If you invest in a corporate bond, you are making a loan to that company. You give the company a specified sum of money for a specific period. In exchange, you can generally expect to receive regular coupons, or interest payments, at designated times. When the bond reaches maturity, you typically receive the face value of your investment.

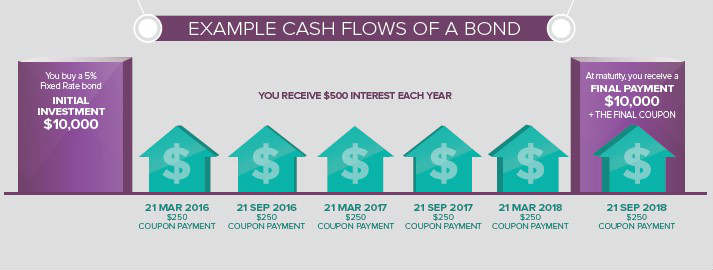

A bond is basically an IOU, with returns to investors determined by two factors as illustrated in figure one:

- The face value of the bond. This is the nominal value of the bond – the principal lent to the company, which it commits to repaying when it matures. If you were to purchase a bond at issue and hold it to maturity, the final payment will typically be the amount of your initial investment plus the final coupon payment – for example, $10,000 + $250.

- The coupon, or interest payments, usually made over the life of the bond. This is the annual income paid to investors, expressed as a percentage of the face value. When bonds first existed in paper form, investors would detach the coupon for that payment and take it to the company’s bank to receive payment, hence the term ‘coupon’.

Figure one: How a bond works

If you buy a bond after its issue date or sell before the maturity date, you may get more or less than the issue price because bond prices tend to have an inverse relationship to interest rates. As illustrated in the example in figure two, when interest rates decrease, the value of a bond will generally increase. Likewise, an increase in interest rates usually results in a decrease in the bond price.

Figure two: Interest rates and bond prices

| Interest rate | Bond price |

|---|---|

| 4% | $108.18 |

| 5% | $100 |

| 6% | $92.56 |

The investment thesis

Bonds have traditionally fulfilled three important roles in an investment portfolio:

- An income stream

Bonds can provide income from regular coupon payments, which are generally quarterly or half-yearly and occur on set dates. As a result, you can expect to plan to match outgoings with the income received from bonds. This feature can be of particular interest to retirees.

- Capital preservation

Bonds can provide capital stability. A bond’s face value is typically returned to the investor when it matures, which can make a bond an effective capital preservation tool – assuming the issuer doesn’t default.

- Diversification of returns

Bonds are classified as a defensive asset, with a different risk and return profile to shares; it’s this difference that provides the diversification benefit.

Investing in corporate bonds

Usually the domain of institutional or ‘sophisticated’ investors, until recently retail investors in Australia could only access corporate bonds through a managed fund or Exchange Traded Fund (ETF). Investors could not pick and choose which corporate bonds they’d like to buy in the same way they could select shares.

Recent innovations have made many investments more accessible to everyone, and this includes corporate bonds. Investors can now also buy Exchange Traded Bond units (otherwise known as XTBs), covering the bonds of many of Australia’s top corporates. They are available on the ASX in the same way you buy and sell those companies’ shares.

What to look for when choosing a corporate bond

Many investors choose the approach of selecting based on the highest yields possible. Most XTB bond issuers are investment grade and therefore investors can see them as being a low risk of default. While seeing this as low risk is a reasonable perspective, it is not zero risk. Generally, a higher yield can also mean higher risk.

Many other fixed features of bonds can be used to build a portfolio specific to your investment requirements. For example, do you want monthly income payments, do you want a portfolio where one of your bonds matures in each year, or do you have a specific amount of income you need to live off each year? All of these defined outcomes can be addressed by selecting the appropriate combination of bonds.

Risks of Exchange Traded Bonds (XTBs)

As with all investments, there are risks you should be aware of before making an investment decision. Some risks for XTBs include:

- Credit risk – the creditworthiness of the issuer of the underlying bonds

- Liquidity risk – the risk that you cannot sell at the price you want prior to maturity

- Concentration risk – investors holding a single XTB will not benefit from the diversification of having exposure to a number of bonds.

- Market risk – changes in market factors may cause the value of an underlying bond and the corresponding XTB to decline.

- Trust risk – includes the risk that XTBs could be terminated or the Responsible Entity is replaced.

You can read more about each of these risks on the XTB website.

This article was reviewed by our Content Producer Isabella Shoard before it was updated, as part of our fact-checking process.

Try our Investor Hub comparison tool to instantly compare Canstar expert rated options.