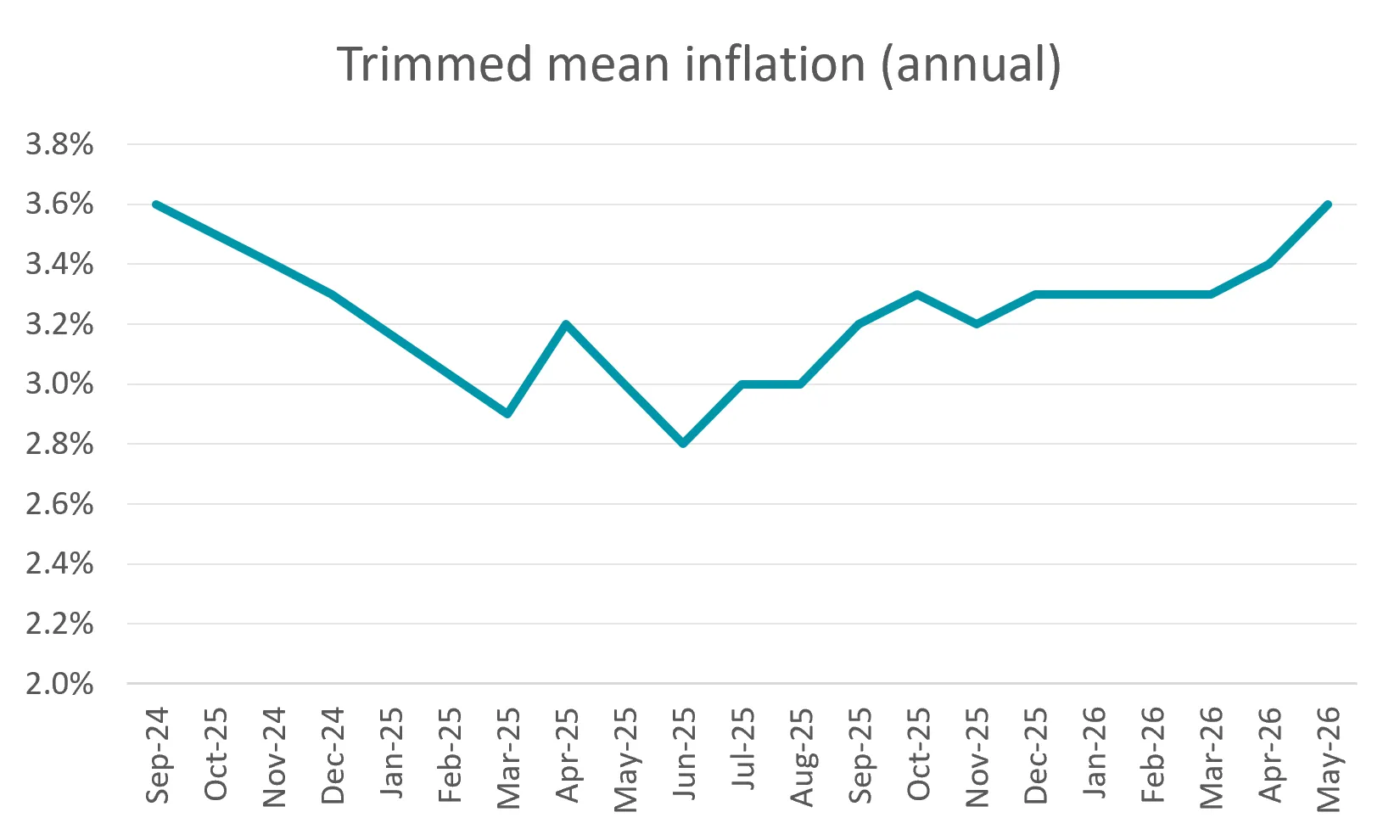

The RBA is unlikely to abandon the prospect of further cash rate hikes despite today’s drop to headline inflation, with the Board’s preferred measure, trimmed mean inflation, moving in the opposite direction.

ABS figures released today saw CPI clock in at 4.0% in the year to May, a far cry from the 5%+ rate predicted at the start of the war, yet core inflation rose to an annual rate of 3.6%, the highest rate in almost two years.

Some of the largest drivers in the inflation data were housing costs including electricity (+21.1%), new dwellings (5.6%), and rents (+3.6%).

Food prices rose from 2.8% to 3.3% in annual terms, on the back of months of supply chain pressures arising from the war in the Middle East.

Consumer Price Index | ||

|---|---|---|

Month | Headline | Trimmed |

January | 3.8 | 3.3 |

February | 3.7 | 3.3 |

March | 4.6 | 3.3 |

April | 4.2 | 3.4 |

May | 4.0 | 3.6 |

Source: ABS Monthly Consumer Price Index.

What does this mean for interest rates?

Today’s core inflation results are likely to frustrate the RBA, with trimmed mean inflation rising for the second consecutive month, putting it back where it was in September 2024.

While the RBA has said it will do what is necessary to achieve price stability “including increasing the cash rate target further if required”, there are a number of data points still to come before the next Board meeting on 10-11 August including:

- 25 June: Labour Force, May and Monthly Household Spending Indicator, May

- 23 July: Labour Force, June

- 29 July: June quarter CPI

- 4 August: Monthly Household Spending Indicator, June

Impact of another 0.25 cash rate hike in 2026

For someone with a $600,000 mortgage and 25 years remaining at the start of the hikes, a 0.25 percentage point cash rate hike in August would increase a borrower’s monthly repayments by $92.

Across what would then be four hikes for the year in February, March, May, and potentially August, the total monthly increase would be $364.

Impact of a | ||

|---|---|---|

Loan size | Hike in | Cumulative |

$600,000 | +$92 | +$364 |

$800,000 | +$122 | +$485 |

$1 million | +$153 | +$606 |

Source: Canstar. Notes: based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2026 at the RBA avg variable rate. Assumes next rate hike falls in August. Calculations assume banks pass on the hikes the month after. Changes are to minimum repayments.

Who will struggle the most under higher rates?

The three RBA hikes this year have already wiped out the buffers many borrowers had built up in their mortgage by keeping their repayments the same following the cuts in 2025.

If the RBA hikes the cash rate once more to 4.60% it will be the highest cash rate setting the country has seen since 2011, a level of pressure many borrowers have never experienced.

Our research shows on average, around 13% of big four bank home loan customers do not have a repayment buffer, including in offset accounts, while a small proportion of these customers are already falling behind on their repayments.

Big four bank | ||

|---|---|---|

Accounts | Accounts | |

CBA | 87% | 13% |

Westpac | 86% | 14% |

NAB | 86% | 14% |

ANZ | 88% | 12% |

Source: Big four bank investor packs. CBA - 31 Dec 25, Westpac - 31 Mar 26, NAB - 31 Mar 26, ANZ - 31 Mar 26. Extra repayments include offset balances.

It’s these customers that need to pull out all stops now before they get hit with another rate hike.

Here’s how:

- Run the numbers: Work out what your repayments would look like if the RBA hikes again in August.

- Ask for a better rate: While these customers are unlikely to be in a position to refinance, they can still negotiate a rate cut with their bank. If you can, keep your repayments the same, even after the rate cut.

- Funnel every spare dollar into the mortgage: This could include making some big family decisions such as cancelling the next holiday or selling a second car.

- Switch other bills: You might be in mortgage prison, but other bills are worth switching if you can find a cheaper offer.

- Consider taking on extra work: Extra money coming in, even temporarily, can help build up that all-important buffer.

- Know your support options: If repayments are becoming difficult ask your lender about hardship assistance. Also seek independent financial advice via the National Debt Helpline: 1800 007 007.

Housing remains major inflation headache

Canstar's Data Insights Director, Sally Tindall, says, “A 5 per cent inflation rate is yet to materialise but that doesn’t mean the RBA’s going to dismiss the prospect of further hikes.”

“Core inflation has risen for the second consecutive month, returning to September 2024 levels. This is a disappointing result given the central bank has been fighting it for four years.

“Housing remains a major inflation headache. Electricity prices surged over 21 per cent annually after the end of the rebates, rent and new home building costs have continued to climb, while food inflation is heating up again. Families hoped grocery prices were stabilising, but supply chain disruptions are pushing costs back up.

“Households with a mortgage should continue preparing for higher rates, particularly those with little or no buffer. Most borrowers have a handle on the pressure that comes from a cash rate setting of 4.35 per cent, but if it goes up another notch we’ll be in territory not seen since 2011, when debts were a lot lower.

“The most vulnerable borrowers are those who have no repayment buffers. Without that safety net, any further increase will immediately strain household budgets.

“There is still time for borrowers to take action. Even if you can’t refinance, you can often negotiate a lower rate with your current lender – and every basis point counts.

“If you’re stretched thin, it could be time to consider some tough lifestyle changes such as temporarily moving in with family, taking a second job, or selling a car. These don't have to be permanent, but acting early helps.”