The Federal Government’s $3.4 million commitment to address affordability in the home insurance sector offers little hope for those seeking relief today from what is often an unavoidable expense.

The commitment, to be spent over the next four years, is part of last week’s Federal Budget “to support and develop measures that place downward pressure on property insurance costs and reduce unintentional underinsurance.”

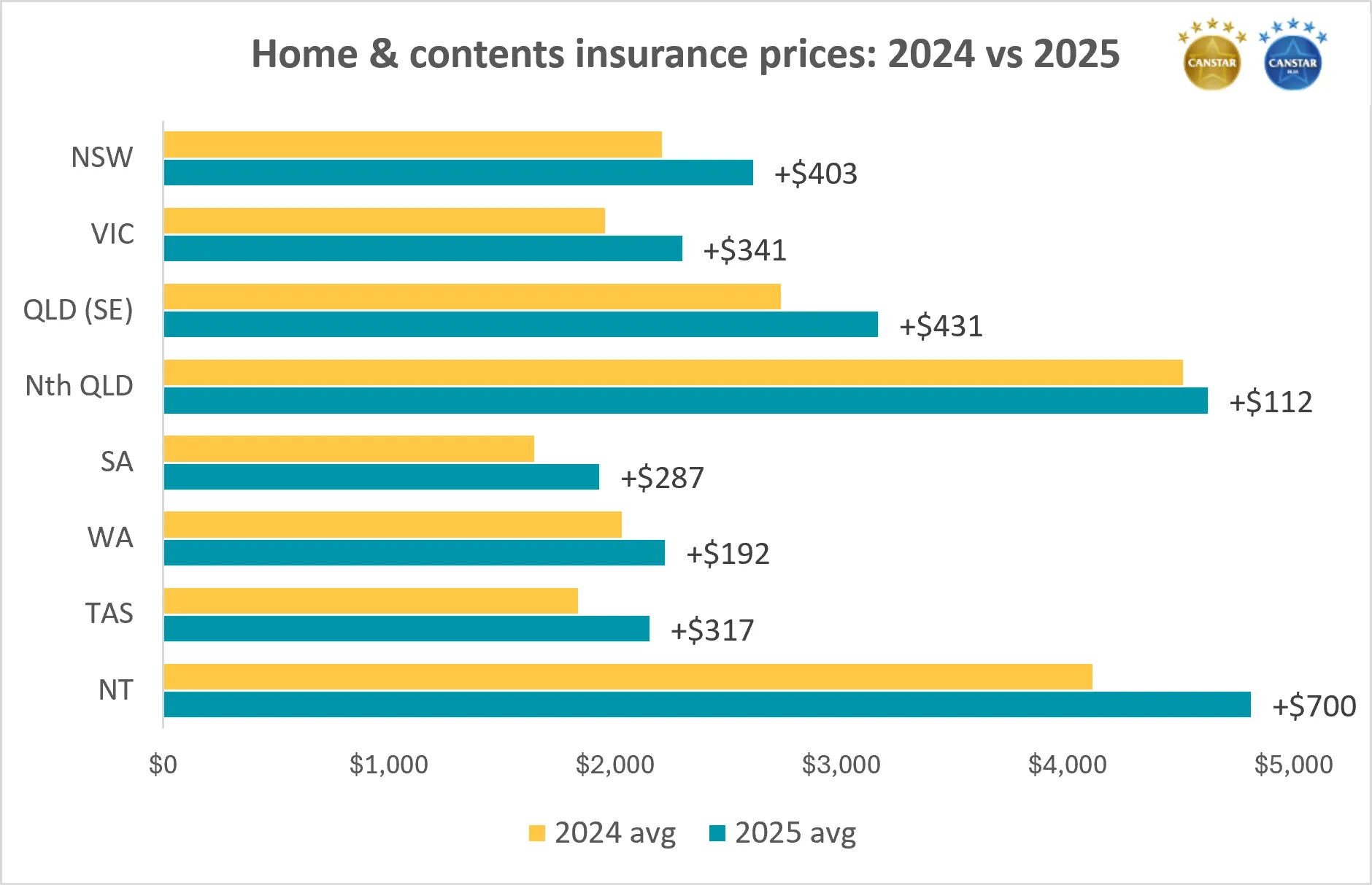

Home insurance is fast becoming one of the biggest financial burdens for many households across the country. Canstar research shows nationally, the average annual home and contents premium jumped by 14% in the 12 months to September 2025.

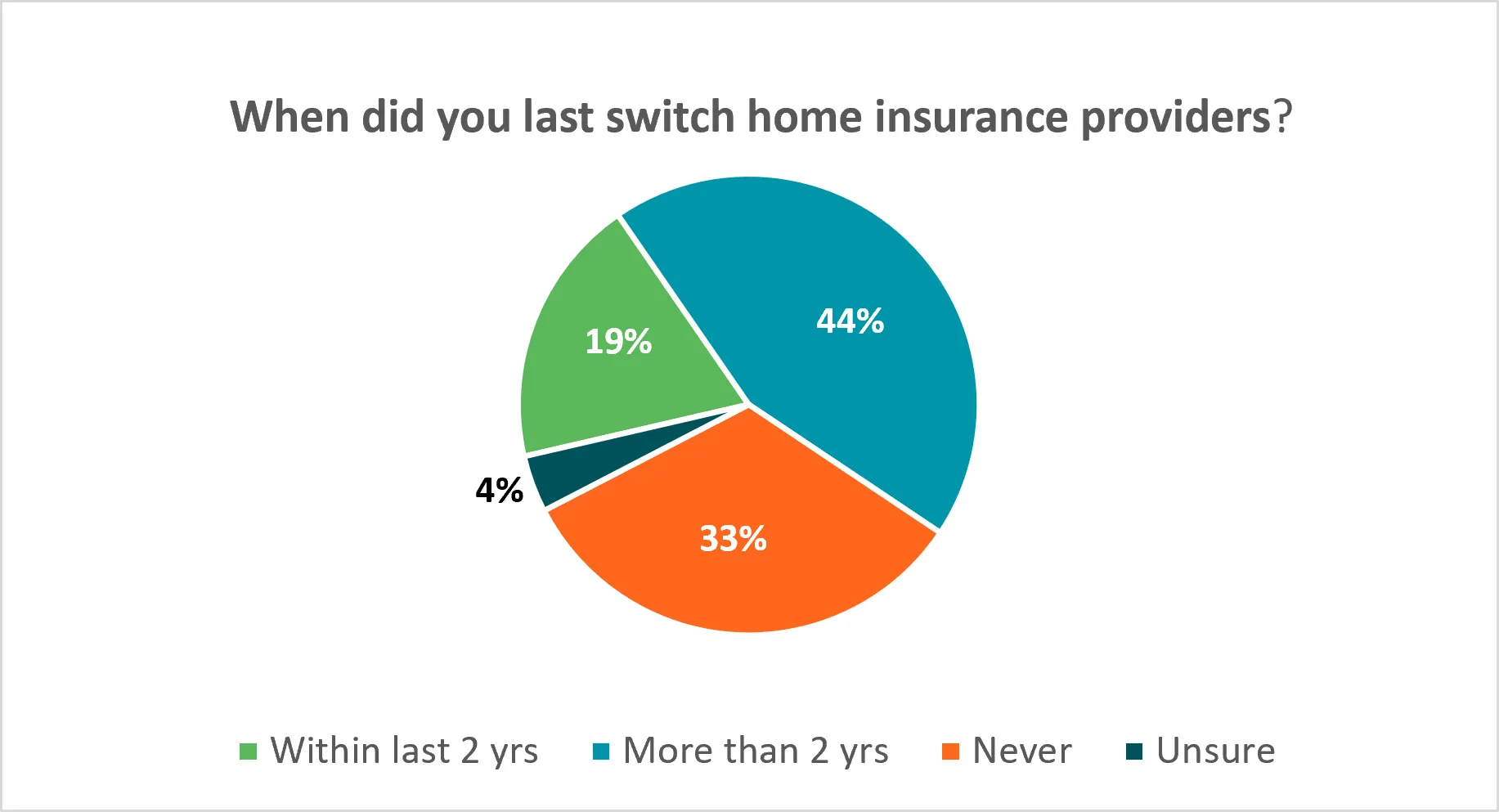

One-third of insured homeowners could find the answer under their noses

A new Canstar survey of 5,484 Australians with home and/or contents insurance shows just 19% have switched providers in the last two years, with the majority of recent switchers unlocking savings as a result.

Concerningly, however, 33% have never changed providers and are likely to be missing out.

Shopping around could drop your premium price by 27%

Canstar research shows a homeowner with an average-priced home and contents policy who switched to a 5-Star Rated one could potentially reduce their costs by $766 a year – a 27% saving.

This analysis is based on around 25,000 quotes from 45 providers covering eight regions and three cover types, undertaken in September 2025.

Potential savings from | |||

|---|---|---|---|

| Market | 5-Star | Potential |

NSW | $2,613 | $1,881 | -$732 |

VIC | $2,299 | $1,664 | -$635 |

QLD* | $3,166 | $2,245 | -$921 |

North | $4,624 | $3,418 | -$1,206 |

SA | $1,933 | $1,325 | -$608 |

WA | $2,224 | $1,575 | -$649 |

TAS | $2,155 | $1,485 | -$670 |

NT | $4,814 | $3,642 | -$1,172 |

National | $2,795 | $2,029 | -$766 |

Source: Canstar. Premiums based on quotes obtained in September 2025 for a range of addresses, property assumptions, and building sum insured amounts between $300,000 and $1,500,000 and a contents sum insured of $50,000. *QLD excludes the portion of the state north of, but not including, Rockhampton.

Rising construction costs increase the risk of underinsurance

The cost to repair or rebuild a home is on the rise. House construction prices rose by 4.1% in the 12 months to March, and 47% compared to six years ago, just before COVID took hold, according to the latest Producer Price Indexes data from the ABS.

For homeowners who haven’t reviewed their sum insured amount recently, there is a real risk that their cover no longer reflects current rebuilding costs.

Tips to review home insurance

- Don’t auto-renew – shop around each year.

- Check what is included and excluded, especially for key risks.

- Review your rebuild costs annually. Make sure they cover the rising cost of construction, any renovations you might have done, and even valuables that are new in your home.

- You can adjust your excess and/or sum-insured to lower your premium, but any savings come with higher risks should you need to make a claim.

- Check for loyalty and bundling discounts, but don’t accept the savings as fact. What ultimately matters is the price you pay for the level of cover you need.

Home insurance brings security, but at what cost?

Canstar’s Data Insights Director, Sally Tindall, says, “Home insurance remains one of the biggest cost pressures for households. While this Federal Budget measure to put downward pressure on prices is welcome, at an investment of just $3.4 million over the next four years, it’s hard to see it making an impact.”

“Some homeowners are increasingly finding themselves in a rock and a hard place when it comes to renewal time, particularly those living in higher-risk areas.

“It’s important to have the security that home insurance can bring, but for many households, they’re now grappling with the question of: at what price?

“It can also be a difficult hurdle to clear for those borrowers who have seen their premiums skyrocket, yet are required by their lender to have adequate insurance as a condition of their mortgage.

“The good news is shopping around can make a difference for most homeowners, with Canstar research showing a typical household could knock the cost of their insurance down by 27 per cent by switching from an average-priced policy to a 5-Star Rated one.

“While it’s great to see the government acknowledge and take steps to tackle the rising issue of insurance unaffordability, households should not wait for changes to flow through the system, but instead take control themselves.”