Australia’s total credit card bill attracting interest dropped in April, despite elevated spending as a result of price hikes flowing through from the Middle East conflict.

Canstar analysis of today’s RBA credit card figures for April 2026 show credit card debt accruing interest on personal cards dropped by $288 million from the previous month (-1.5%).

At an average rate of 18.59%, this drop equates to a collective saving in interest charges of $147,000 a day.

Total credit card bill | |

|---|---|

Amount - | $19.4 |

Monthly | -$288 million |

Source: RBA credit card statistics, April 2026, released 9 June 2026, original data terms, excludes commercial cards. Year-on-year analysis not available due to a series break in November 2025.

Spending dips, but still at second-highest level on record

Debit and credit card spending dropped noticeably in April, on the back of the temporary halving of the fuel excise. However, it still hit an eye-watering $88.5 billion — the second-highest on record, with the highest level recorded the month before.

This bumper spending across March and April comes on the back of surging costs for everyday essentials driven by the war in the Middle East.

Value of | |||

|---|---|---|---|

Amount | Monthly | Annual | |

Debit | $59.7 | -$1.1 | +$5.6 |

Credit | $28.8 | -$1.1 | +$338 |

Total | $88.5 | -$2.2 | +$6.0 |

Source: RBA credit card statistics, personal cards, April 2026, released 9 June 2026, seasonally adjusted data.

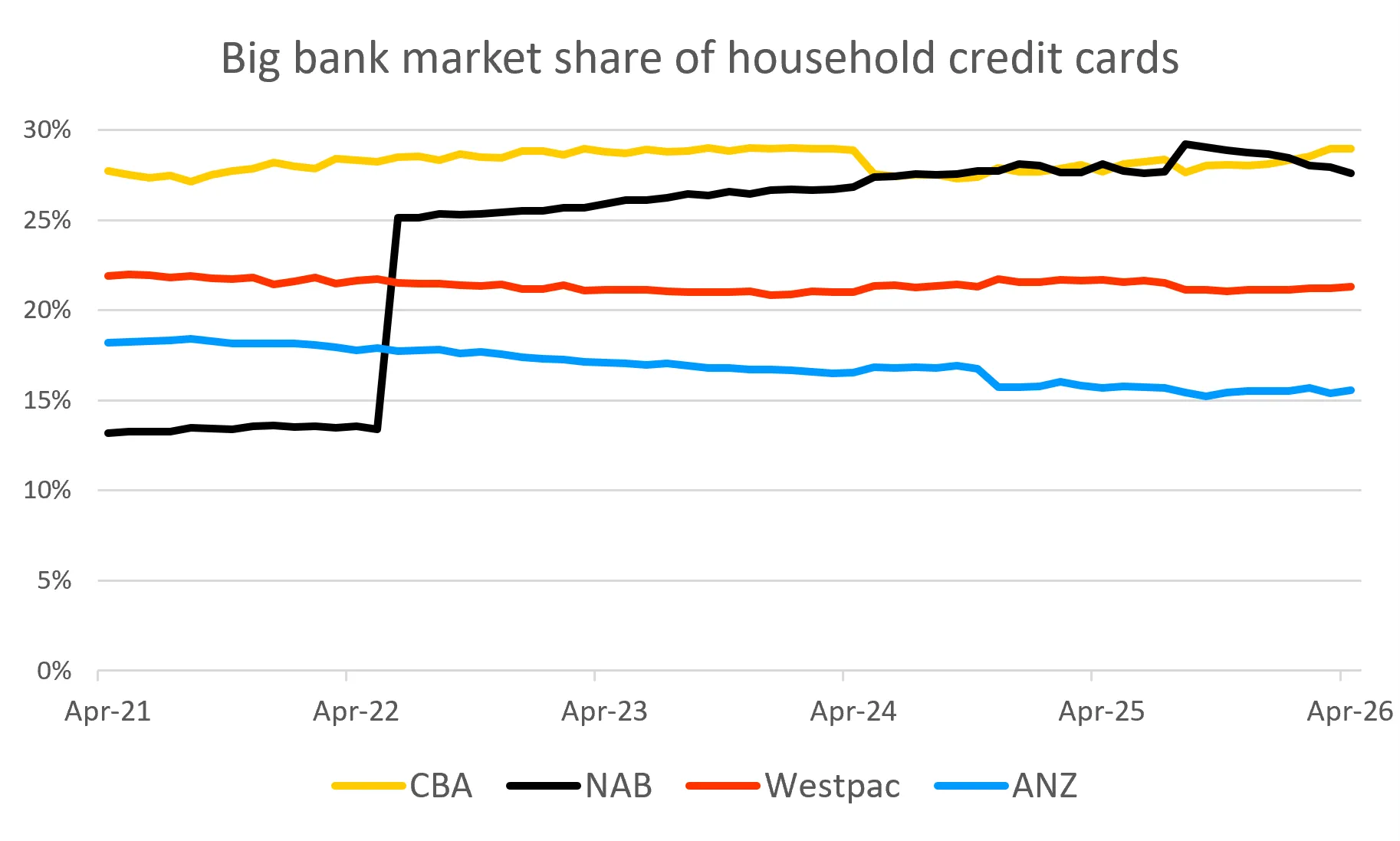

Big banks dominate, as CBA and NAB battle for top spot

The big four banks are keeping a tight hold on the credit card market, accounting for 93% of card balances held by authorised deposit-taking institutions, according to APRA’s latest banking statistics for April, released 29 May.

CBA has the largest share of personal credit cards, at 29%, closely followed by NAB with a 28% share.

Aussies have regained control over their credit cards

Canstar's Data Insights Director, Sally Tindall, says, “Households appear to have regained some control over their credit card debt after a turbulent start to the year.”

“While this drop is relatively minor, it would not have been an easy feat for some households to pull off, at a time when the cost of everyday living took a sharp rise.

“What we know from past experience is that when times get tough, Australians focus on getting themselves into a better financial position to weather the storm.

“This is particularly important when it comes to credit card debt, with the average rate sitting at 18.59 per cent, making it one of the most expensive forms of debt available.

“While spending dipped in April, Australians still put an enormous $88.5 billion through their debit and credit cards, making it the second-highest monthly spend on record.

“Households are still spending significantly more than they were a year ago, not necessarily because they’re splashing out, but because the cost of many everyday essentials remain elevated.

“Card spending is up 7 per cent from the previous year, well above the rate of inflation, but what’s interesting is that people are increasingly reaching for the debit card, not the credit card.

“The big four banks still have a vice-like grip on Australia’s credit card market, accounting for more than nine in every 10 dollars owed on credit cards across the banking sector.

“CBA and NAB are effectively running neck and neck, together holding well over half of all outstanding credit card balances, yet they are by no means offering the lowest cost cards.

“If you have existing credit card debt, know there are still five lenders offering interest rates under the 10 per cent mark.”