COVID-19 crisis, two months in: What's the state of finances, property and our mood?

Two months after the first recorded death in Australia from COVID-19, the country is keenly feeling the economic fallout of the crisis, new statistics show. Here’s what’s happening to household finances, the property market and the mood of the nation in what has been called the most challenging economic climate in living memory. And it’s not all doom and gloom.

House Prices in Australia, April, 2020

How is the Australian property market reacting to COVID-19?

House prices across many parts of Australia have risen slightly in April, despite a sharp decline in market activity and consumer confidence since the coronavirus lockdown began, according to a new report.

Results from property research house CoreLogic’s Home Value Index found that most Australian cities recorded a small jump in home values through April, including a 0.4% increase in Sydney and a 0.3% rise in Brisbane.

Related story: How will coronavirus affect property prices in Australia?

CoreLogic’s head of research Tim Lawless said these findings show a “remarkably resilient” market despite the weakening economic conditions caused by the coronavirus.

However, while some Australian cities did see an increase in values in April, the national monthly pace of growth in the market more than halved, dropping from 0.7% in March to 0.3%, while prices in Melbourne and Hobart dipped slightly.

Mr Lawless said this overall weakening in housing activity began when social distancing policies were introduced, including a ban on open homes and on-site auctions.

Some of these restrictions have now been lifted in the Northern Territory and Western Australia and will soon be lifted in NSW, however they remain in place for all other states.

Related story: Online auctions: selling homes under a virtual hammer

The CoreLogic report also found that capital city markets generally showed a weaker performance than regional markets when it came to house price growth in April.

Mr Lawless said larger cities are at a higher risk of a downturn than other markets during the COVID-19 crisis, due in part to their dependence on foreign buyers to drive up demand, as well as “stretched housing affordability and already low rental yields”.

Canstar finance expert Steve Mickenbecker said that while the Reserve Bank’s recent cash rate cuts and the government COVID-19 support packages may have helped to provide a minor lift to house values, these measures are in place to assist Australian consumers and businesses during the pandemic, not to support the property market.

“We’ve only at this stage seen the start of a recession and recessions have always meant lower property prices and lower activity in the market. It looks inevitable that we will also see it this time around,” he said.

Where to from here for real estate?

Chief economist at AMP Capital, Shane Oliver, believes if the coronavirus lockdown starts to be eased domestically through this month, as expected, then the fall in average property prices is likely to be around 10% during the course of this crisis.

However, if the lockdown extends beyond six months and involves a second wave of coronavirus cases after an initial easing, then Dr Oliver said it could “overwhelm the ability of the JobKeeper program and the banks’ repayment holidays to protect the economy and the property market and hence average home prices could fall 20% or so.”

“This is looking less likely, but it’s a risk,” he said.

Mr Lawless agreed that downward pressure on markets will occur in coming months, and the magnitude of this downturn will hinge on the timing and extent of social distancing policies being lifted, however he said there are positive signs ahead.

“The good news is that Australia has managed to flatten the spread of the virus more effectively and efficiently than expected and we are already seeing a subtle easing of social distancing policies in some states. An early return of economic activity should support a lift in consumer spirits, which in turn should see housing market activity sparking back to life,” he said.

Is now a good time to buy?

While there is still a lot of uncertainty as to when the downturn in the market from the coronavirus may end, Mr Mickenbecker said sooner or later, home buyers will be ready to “jump back in looking for bargains”.

For some buyers whose income has remained stable and secure during this pandemic, lower property prices and the historically low interest rates currently on offer may place them in a more advantageous position.

“We are seeing great deals in fixed-rate home loans right now due in part to the quantitative easing announced from the RBA,” Canstar money expert, Effie Zahos said.

“And there is a lot of variation in variable rates between the cheapest and the dearest.”

For instance, the lowest variable rate home loan on Canstar’s database is currently 2.39% (comparison rate 2.40%) and the highest is 5.39% (comparison rate 5.66%), for principal and interest-paying owner-occupiers taking out a $400,000, 80% LVR home loan.

However, while interest rates are low right now, some banks have tightened their lending policies during the pandemic, which means it may be harder for some to secure a home loan at this time.

Related story: How hard is it really to get a home loan right now?

For those who already have a home loan, Ms Zahos said it may be a good time to look at what your current interest rate is and compare it with other home loans on the market to see if yours is still competitive.

“Keep in mind the lowest rates right now may be from lenders you have never heard of,” she said.

Household finances in Australia, April 2020

Crisis is taking a toll, but it’s impacting people in different ways

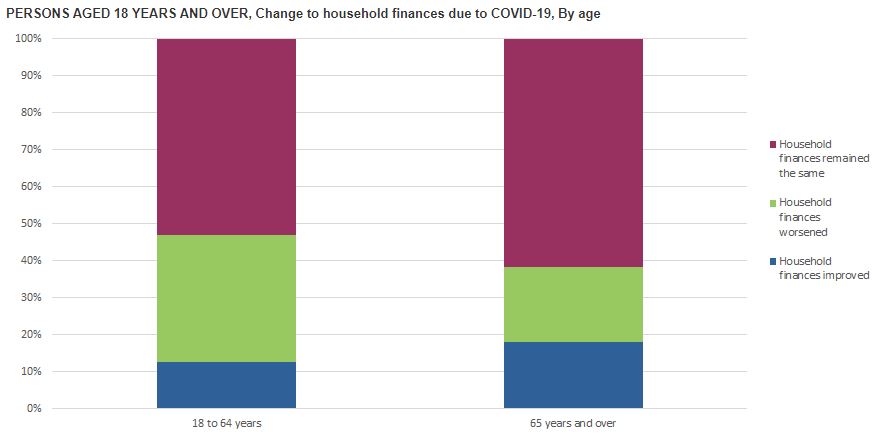

The fallout from the COVID-19 outbreak and subsequent lockdown in Australia has also caused financial stress among almost a third of all Australian households, according to an Australian Bureau of Statistics (ABS) COVID-19 survey, released on May 1.

However, the same stats show that 14% of households reported an improvement in their financial conditions, and more than half said that their finances remained unchanged. Social distancing policies designed to keep people from contracting coronavirus has also meant many people are unable to spend money on entertainment or on other discretionary purchases.

Related story: Your money and coronavirus: 10 steps to help protect your finances

However, Michelle Marquardt, ABS Program Manager for Household Surveys, said only “a small number of Australians reported experiencing financial hardship”.

“One in 13 Australians (7.5%) said their household lacked the money to pay one or more bills on time, and one in ten (10%) had to draw on accumulated savings to support basic living expenses,” Ms Marquardt said.

The stimulus payment has boosted bank balances

The ABS survey found that about one quarter of Australians received the first one-off $750 economic support payment, part of the Australian Government’s COVID-19 economic stimulus package.

“Those aged 65 years and over were more likely than those aged 18 to 64 to have received the first one-off $750 economic support payment (60% compared with 19%),” said Ms Marquardt.

“Around half (53%) of persons who received the economic support payment added it to savings, with persons aged 65 years and over more likely to do so than persons aged 18 to 64 (71% compared with 37%).”

Emotional wellbeing in Australia, April 2020

We are down, but not out

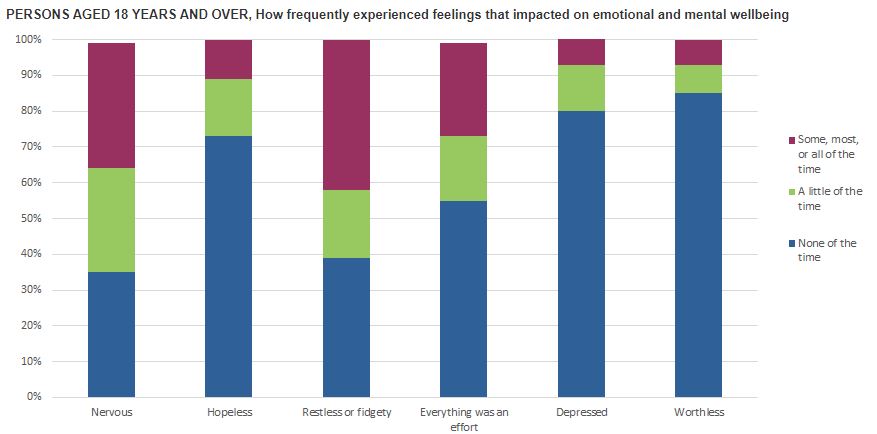

The crisis is causing emotional and mental stress, but there are promising signs that some of us are finding ways to cope. The ABS asked people about how they were feeling during this time of crisis, and compared those answers to its 2017-18 National Health Survey, which asked the same questions.

The results showed that on average, people were suffering from more emotional symptoms associated with “experiences of anxiety and depression” than they were a few years ago, although there were some silver linings to this.

The most commonly reported symptoms were nervousness and feeling restless and fidgety a little, some or most of the time. Those findings showed we were feeling those side effects to a much higher degree than a few years ago. We were feeling slightly more hopeless, but less depressed (7% felt so depressed that nothing could cheer them up at least some of the time, compared with 8% in the 2017-18 study).

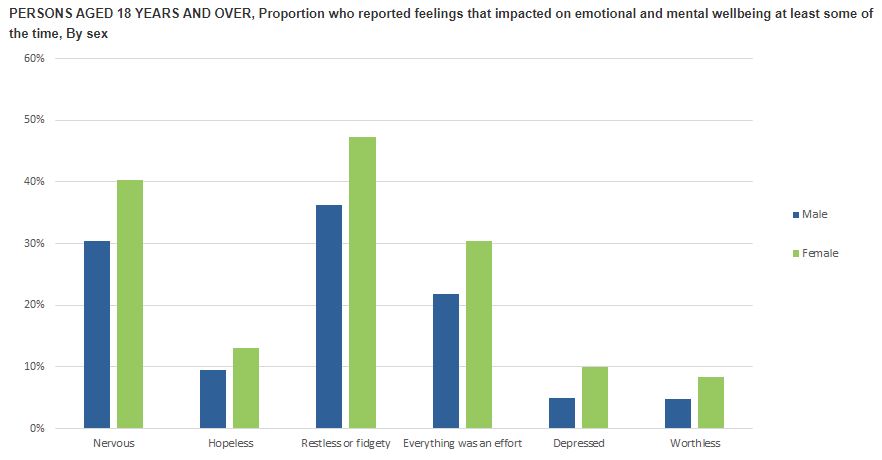

More women were reporting emotional symptoms than men.

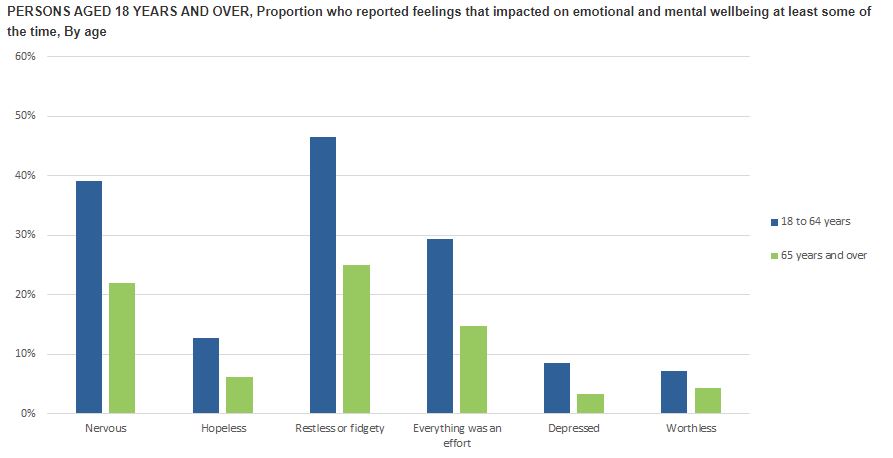

However, those aged older than 65 were doing better emotionally than younger people, the survey found.

Related story: Mental health: what is covered by Medicare and private health insurance?

We are alone, together

However, while social distancing rules may be keeping us apart physically, we are finding ways to stay in touch.

The survey found almost all Australians had had “non face-to-face contact with family or friends outside of their household in the first two weeks of April”. This included:

- Verbal only phone calls (92%);

- Text messaging or instant messaging (86%);

- Video calls e.g. Skype, Facebook Messenger, Zoom (67%); and

- Email (42%).

Related story: The best broadband and NBN plans for working from home

If you or someone you know needs support, call Lifeline on 13 11 14 or beyondblue on 1300 224 636. If it is an emergency, call 000.

Additional reporting by Amanda Horswill.

Follow Canstar on Facebook and X for regular financial updates.

Owner occupied

30% min deposit

Redraw facility

Owner occupied

30% min deposit

Redraw facility

Try our Home Loans comparison tool to instantly compare Canstar expert rated options.