Headlines don't tell the whole savings interest rate story

Deposit holders are being urged to look below the headline rate (the advertised rate), as the base rate you’re in for later can dwindle down to below the cash rate if you’re not paying attention.

That’s right – the average base rate on online savings accounts (1.69%) is now less than the official cash rate (1.75%).

Less than five years ago, we were seeing steady growth in the difference margin between promotional rates and base rates, which is a way for banks to maintain an attractive headline rate while paying a lower ongoing rate after the promotional period ends. Unsuspecting consumers could be in for a shock when the promotion ends and the interest they earned was considerably less than they were expecting.

However, these days, base rates for online savings accounts are languishing around 1.69% on average and headline rates are being advertised at an average of 2.14%, which is a mere 45 basis points above that amount. Back in 2012, the difference between base rates and headline rates was more substantial, at 143 basis points. (Of course, back then competition for banks to hold your savings was fierce and base rates were quite healthy on their own without any promotional bonus rate, at a whopping 4.90% in late 2011.)

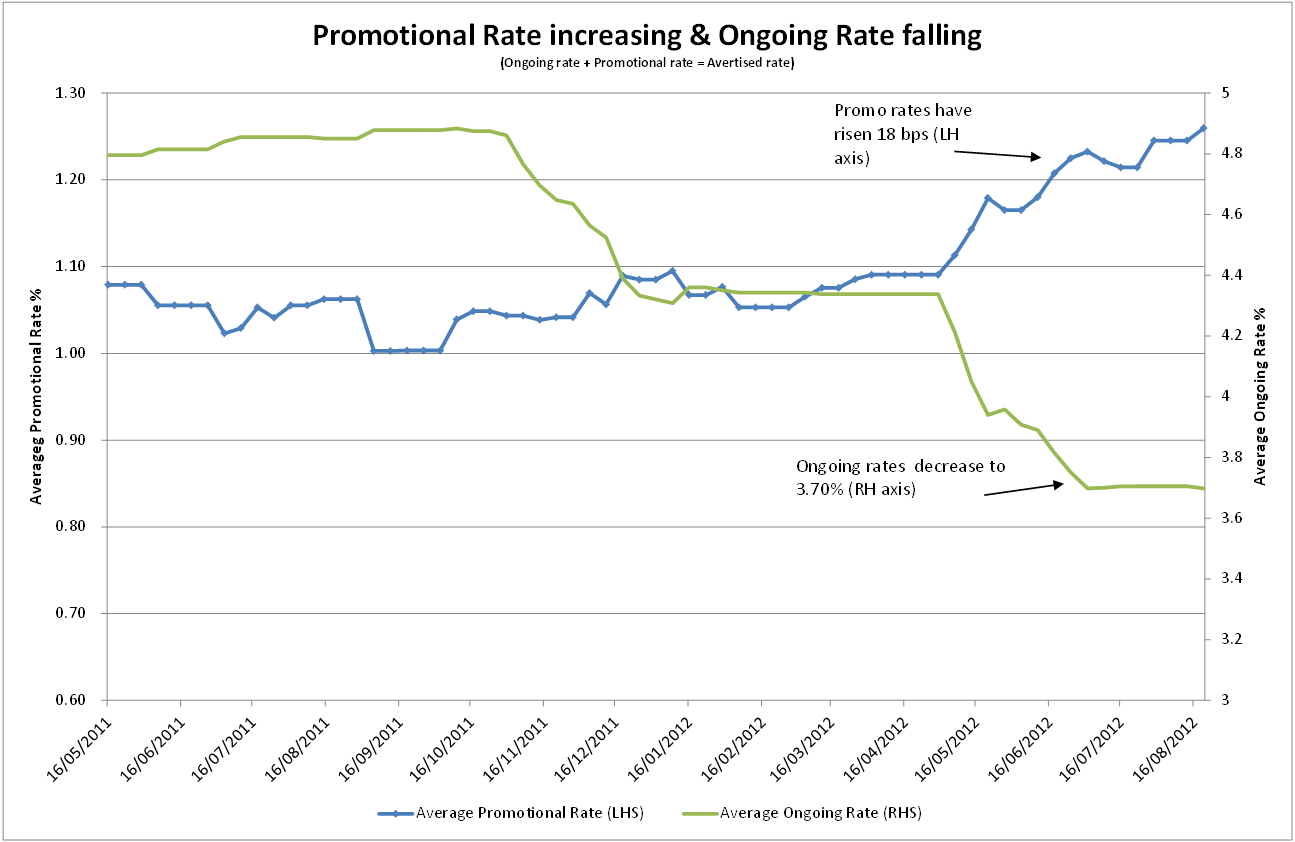

The chart below illustrates promotional rates (left hand axis) are being used as a tool to maintain attractive headline interest rates without the cost of paying high ongoing interest. As base rates (right hand side) have declined since the Reserve Bank rate decreases, promotional rates have likewise decreased.

CANSTAR research shows that rates can decrease by as much as 105 basis points at the end of the promotional period if you’re on the current maximum bonus rate of 3.40%. It may not sound like much, but that difference can be almost 35% of the advertised rate! So it pays to know the conditions attached to your account and how long the attractive rate is guaranteed.

Moving larger sums of money into term deposits is one way of making sure your money works harder and your rate is guaranteed for the entire term. But for those savers who want rates up there with term deposits but want access to use their money at any time, then bonus savings accounts are still the best fit. Providing you are aware of any bonus conditions or promotional periods, you can make these accounts work for you.

The low-rate environment we are in right now is not good news for the cashed-up. To throw further confusion into the mix, savings rates often move independently of the official Reserve Bank rates. It’s more important than ever to keep on top of what financial institutions are offering and take advantage anywhere you can.

This usually starts by making sure your money is in the right account. Canstar can help you there. We regularly research and rate savings accounts, term deposits, and more, as well as providing educational resources explaining how different types of accounts work. Make our website your one stop shop when it comes to finding an outstanding value place to store your savings.

Try our Savings Accounts comparison tool to instantly compare Canstar expert rated options.