The RBA is set to officially hit pause on the cash rate hikes tomorrow for the first time this year, however, borrowers should do anything but.

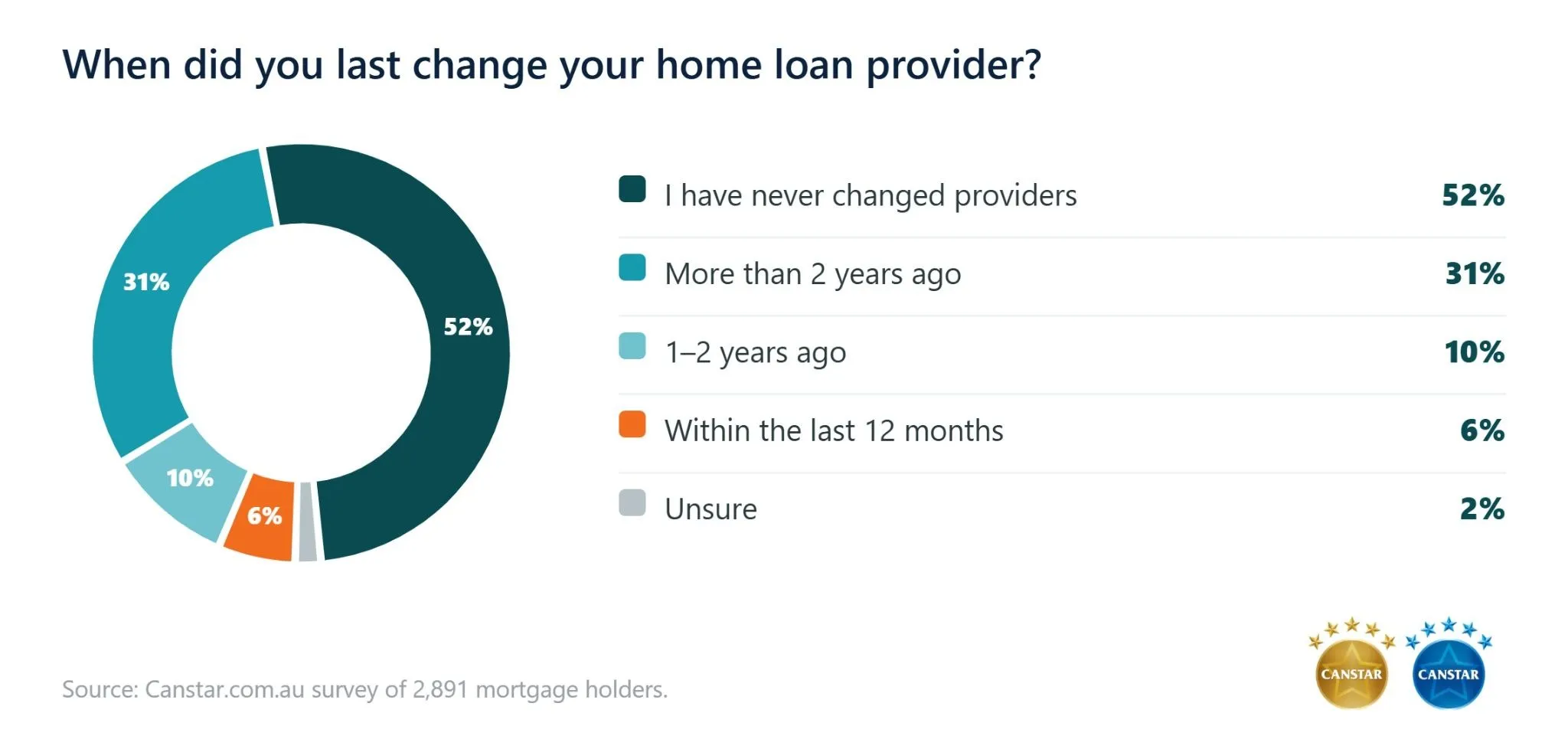

A new Canstar survey of 2,891 home loan borrowers found just 6% have switched to a new lender in the past 12 months, while more than half (52%) have never changed providers at all.

Complacent borrowers likely to be on uncompetitive rates

An owner-occupier who took out a loan five years ago and hasn’t renegotiated since is likely to be on a rate of 6.98%. Yet Canstar data shows there are 40 lenders offering variable rates under 6%.

Assuming a borrower has a $600,000 balance today with 25 years remaining on their loan, refinancing to a rate under 6% could save at least $10,713 over the next two years, even after allowing for $1,150 in switch costs. This assumes rates move in line with CBA’s current cash rate forecast.

Potential impact from refinancing a $600k loan

Variable rate today

Repayments

Cost - next 2 yrs

Complacent borrower

6.98%

$4,233

$79,686

Refinance to a competitive rate

5.99%

$3,862

$68,973

Difference

-0.99

-$371

-$10,713

Source: Canstar. Notes: calculations are estimates based on an owner-occupier paying principal and interest who took out a loan in June 2021 and today has $600k owing and 25 years remaining. Assumes the person has not renegotiated their rate since. Costs include $1,150 in switch costs, but not ongoing fees. Calculations assume rates change in line with CBA's cash rate forecast.

6.24% is the lowest fixed rate for 1- and 2-year terms.

Lowest variable rates on Canstar

Lender

Rate from

LCU

5.69%

Horizon Bank, Pacific Mortgage Group

5.74%

Unity Bank

5.80%

Virgin Money, Police Bank

5.84%

Freedom Lend, Gateway Bank, Mortgage House, Police Credit Union, RACQ, Transport Mutual, Unloan

5.89%

Source: Canstar. Rates based on owner occupier loans. LVR and other requirements apply. Excludes green loans.

Impact of another 0.25 cash rate hike in 2026

While the RBA is set to pause in June, borrowers should not take this as confirmation the rate hikes are over, with Westpac expecting another hike at the next meeting in August.

For someone with a $600,000 mortgage and 25 years remaining at the start of the hikes, a 0.25 percentage point cash rate hike in August would increase monthly repayments by $92.

Across what would then be four hikes for the year in February, March, May, and potentially August, the total monthly increase would be $364.

Impact of a further 0.25 hike on monthly repayments

Loan size at start of hikes

Hike in August

Cumulative increase (Feb + Mar + May + Aug)

$600,000

+$92

+$364

$800,000

+$122

+$485

$1 million

+$153

+$606

Source: Canstar. Notes: based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2026 at the RBA avg variable rate. Assumes next rate hike falls in August in line with Westpac’s forecast. Calculations assume banks pass on the hikes the month after. Changes are to minimum repayments.

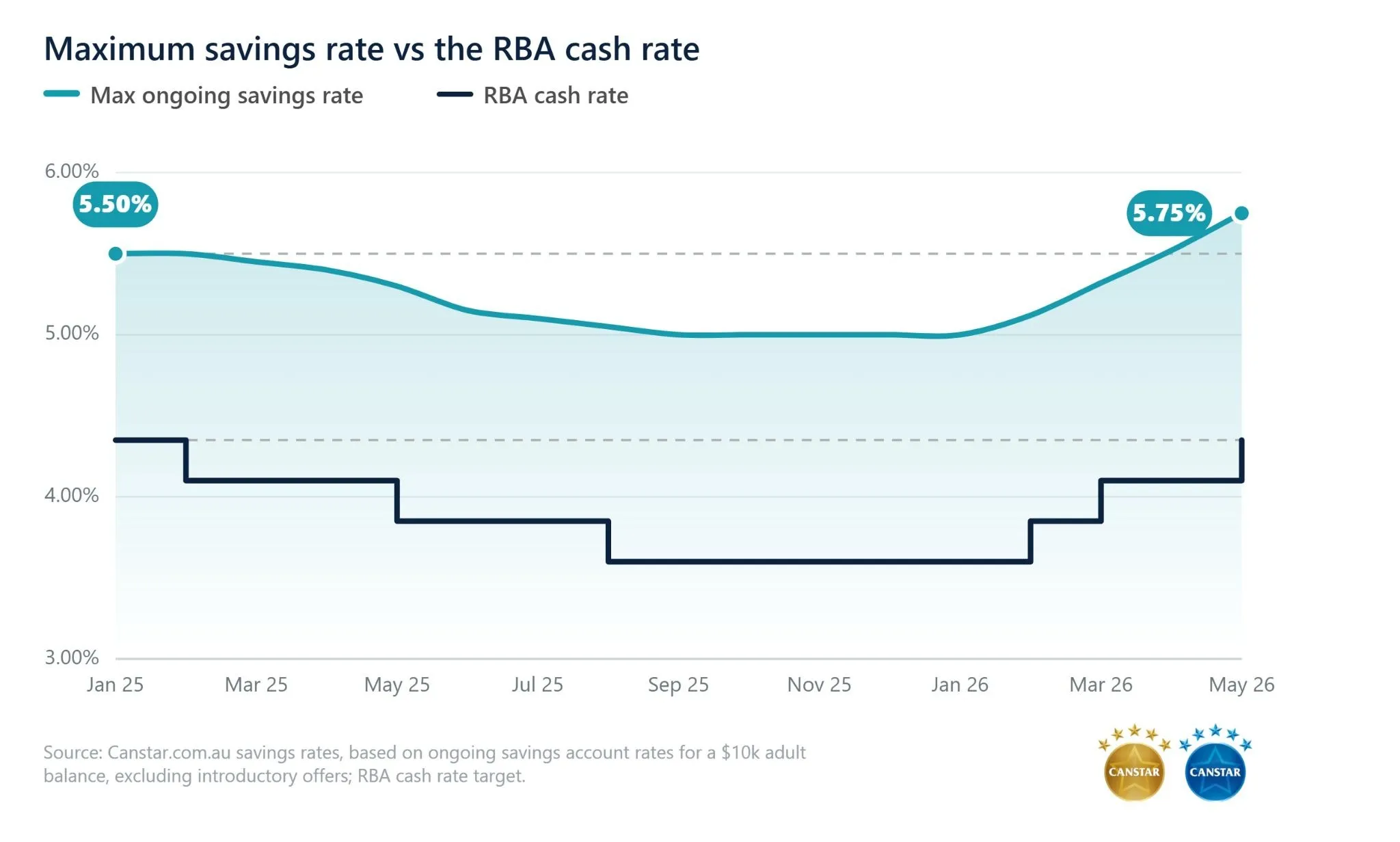

Savings rates continue to climb

Rate tracking by Canstar shows savings rates are now sitting at 14-year high, based on Canstar’s tracking, with the highest ongoing savings rate now sitting at 5.75% – 0.25 higher than what it was back when the cash rate was last at 4.35%.

The highest term deposit rate has now hit 5.70%, available from Rabobank for a 5-year term for balances over $500k up to $2 million.

Market leading savings rates

Type of account

Rate if conditions met

Bank

Bonus saver

5.75%

Westpac (ages 18-40)

Unconditional saver

5.25%

Teachers Mutual Group, Police Bank (young adults)

Introductory saver

5.90% for 4 mths, then 4.00%

Rabobank

Term deposit

5.70%

Rabobank

Source: Canstar. Note: monthly conditions for bonus interest vary between accounts.

The RBA might be standing still, but you shouldn't

Canstar's Data Insights Director, Sally Tindall, says, “The RBA is expected to pause the rate hikes at the end of tomorrow's meeting. The Board previously expressed a desire to assess how households and the economy are holding up, and recent data provides it with the opportunity to do so.”

“The RBA might be standing still, however, borrowers who follow suit could end up paying a premium.

“Canstar’s research shows half of borrowers surveyed have never switched lenders and those who haven't negotiated in years are likely overpaying.

“If this sounds like you, run the numbers on refinancing while the cash rate is on hold. You might uncover a substantial saving at a time when you need it most.

“Borrowers often assume loyalty will be rewarded, but in the mortgage market that’s rarely the case. In the last round of rate hikes, we saw a smattering of lenders cut variable home loan rates, but only for new customers.

“On the flipside, savers continue to benefit from higher rates, although it’s worth checking the fine print on any rate hike you might have received from your bank.

“The highest ongoing savings rate is now an extremely healthy 5.75 per cent, however, you have to be aged 18 to 40 to qualify.

“Meanwhile, the highest term deposit rate is now 5.70 per cent but only for amounts over half a million dollars with a half a decade commitment.

“What is highly uncertain is which direction the cash rate will go next and when. With inflation sitting at 4.2 per cent, the RBA is likely to keep the country on notice as more hikes could still be necessary.”

Belinda leads Canstar’s external communications and media relations strategy, bringing over a decade of expertise in the financial services industry. A passionate finance enthusiast and seasoned spokesperson, she is a regular fixture in the national conversation—appearing across television, radio, and major print publications to demystify the financial topics that matter most to Australians.

Before joining Canstar, Belinda served as Head of Corporate Affairs for one of Australia’s largest listed mortgage brokers, managing everything from investor relations to government affairs. Her international experience includes leading high-impact media and influencer strategies in North America for Canada’s top tech and real estate brands.

Important Information

For those that love the detail

This advice is general and has not taken into account your objectives, financial situation or needs. Consider whether this advice is right for you.

This advice is general and has not taken into account your objectives, financial situation, or needs. It is not personal advice. Consider whether this advice is right for you. For more information, read Canstar’s Financial Services and Credit Guide (FSCG) and our detailed disclosure. Canstar may receive a fee for referring you to a product provider – for further information, see how we get paid. Payment of fees for ads does not influence our Star Ratings or Awards. Canstar is a comparison website, not a product issuer, so it’s important to check any product information directly with the provider. Consider the Product Disclosure Statement (PDS), Target Market Determination (TMD) and other applicable product documentation before making a decision to purchase, acquire, invest in or apply for a financial or credit product. Contact the product issuer directly for a copy of the PDS, TMD and other documentation. Canstar is an information provider and in giving you product information Canstar is not making any suggestion or recommendation about a particular credit product or loan. If you decide to apply for a credit product or loan, you will deal directly with a credit provider, and not with Canstar. Rates and product information should be confirmed with the relevant credit provider. For more information, read the credit provider’s key facts sheet and other applicable loan documentation for that product. Read the Comparison Rate Warning.

Research provided by Canstar Research AFSL and Australian Credit Licence No. 437917. Canstar Pty Ltd AR 443019 CR 538715.

a. The views, opinions, and positions expressed in this piece are the views of the author(s) alone, and do not necessarily reflect the views of Canstar.

b. The views, opinions and advice quoted in this piece are those of the author(s) or interviewee(s) expressing them, and do not necessarily reflect the views of Canstar. Any other views expressed and advice given by Canstar or its employee(s) in the above article are not necessarily those of the same author(s) or interviewee(s).

The examples provided in the article are not based on actual products or real consumer circumstances. The information in this article is of a general nature only, and does not take into consideration your objectives, financial situation or needs. It is not personal advice, and you should not rely on it, even if the example is similar to your own circumstances. You should make your own enquiries and calculations based on your own personal circumstances as well as finding out specific product costs, rates or features that may be relevant to you. You should consider seeking independent advice before making a purchase, credit, or investment decision.