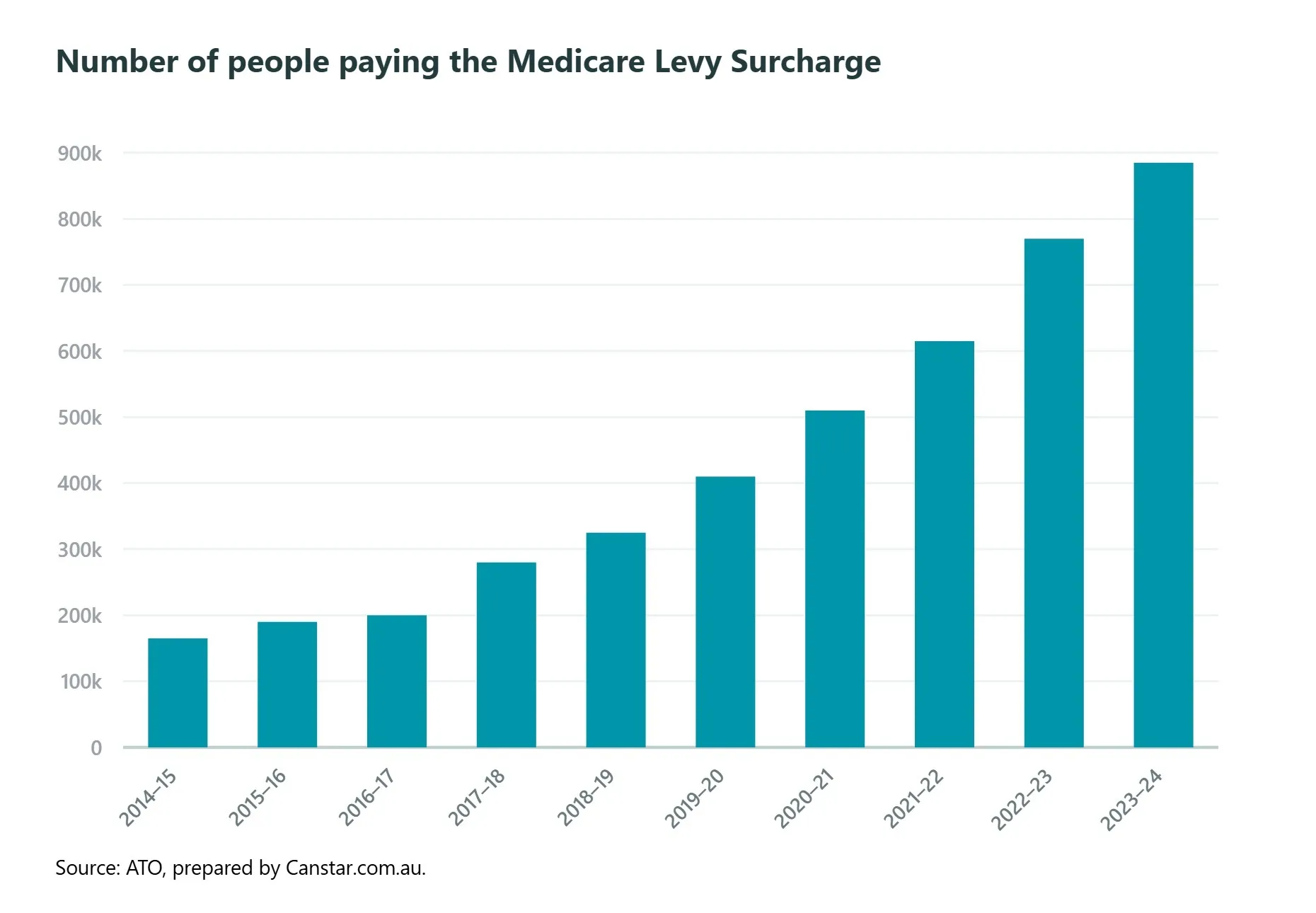

The number of Australians paying the Medicare levy surcharge has risen sharply, increasing 15% over a 12-month period and 74% over three years, according to the latest ATO figures released last week.

In total, 885,087 taxpayers paid this additional tax in the 2023-24 tax year, at an average of $1,284.

The Medicare levy surcharge is paid by Australian taxpayers who earn over a certain amount and do not have private hospital cover. The surcharge is between 1%-1.5% of a person’s taxable income and is in addition to the 2% Medicare levy all taxpayers pay to support the public health system.

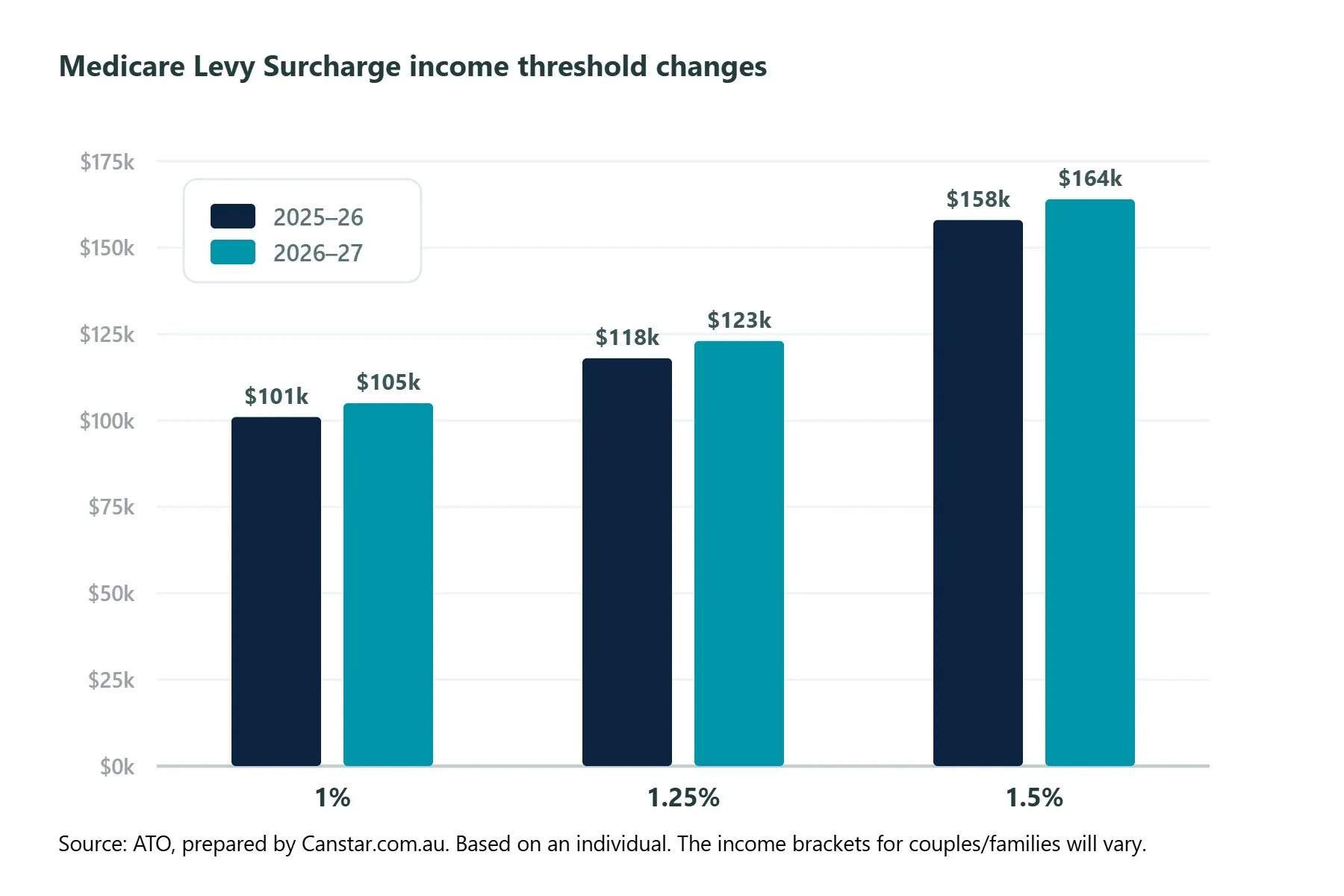

2026-27 income threshold increase not enough to spare average earners

The income threshold for the Medicare levy surcharge is increasing from $101,001 to $105,001 from 1 July 2026.

However, this rise won’t spare the average full-time worker, with the average wage now sitting at $106,950 according to the ABS.

From 1 July, those earning over $105k who don’t have private hospital cover will pay a surcharge of 1% of income, in addition to the 2% Medicare levy.

Those earning over $123k will pay a 1.25% surcharge, while those earning over $164k will pay the maximum surcharge rate of 1.5%.

Cover could be cheaper than the surcharge

From 1 July, the minimum amount a taxpayer who doesn’t have hospital cover could pay under the surcharge will be $1,050, while the average full-time worker will pay around $1,070.

Yet, Canstar analysis shows the lowest-priced basic hospital policy is, on average across the states, $993 annually.

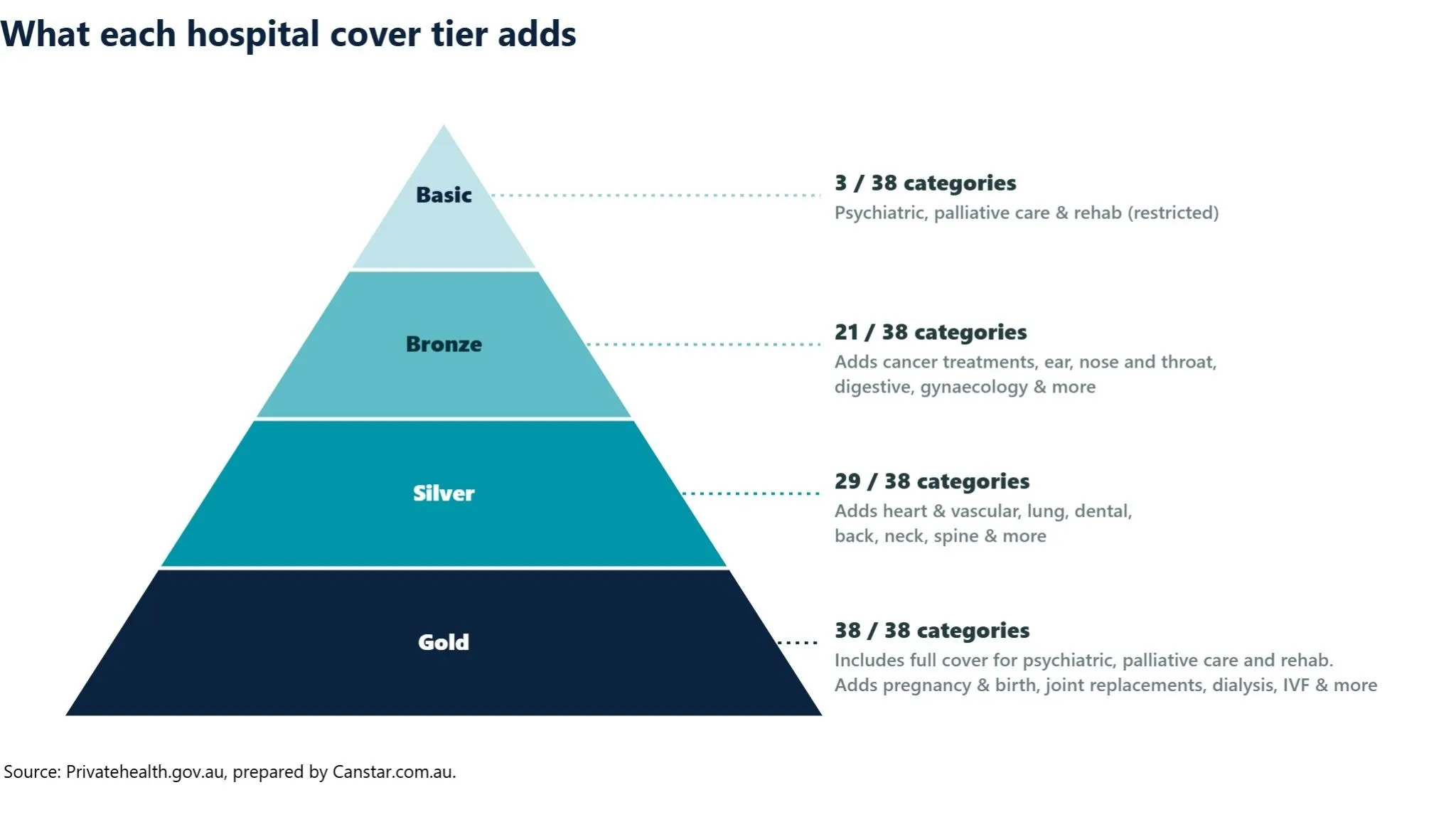

While basic cover helps people avoid paying the surcharge, it offers limited benefits. For just an extra $19 per month, on average, Australians could upgrade to a bronze policy and be covered for 18 additional services.

Annual hospital cover - | ||

|---|---|---|

Hospital | Lowest national | Difference to |

Basic | $993 | -$77 |

Bronze | $1,216 | +$146 |

Silver | $1,592 | +$522 |

Gold | $3,332 | +$2,262 |

Source: Canstar. Based on hospital insurance policies on Canstar’s database. Tier 1 rebate for under 65s of 16.079% applied. National average based on state averages weighted by proportion of hospital insured persons (APRA Mar 26).

Annual hospital cover - | ||

|---|---|---|

Region | Lowest-priced | Lowest-priced |

NSW | $1,033 | $1,226 |

VIC | $1,028 | $1,288 |

QLD | $1,037 | $1,311 |

SA | $995 | $1,210 |

WA | $794 | $948 |

TAS | $1,011 | $1,226 |

NT | $396 | $594 |

Source: Canstar. Based on hospital insurance policies on Canstar’s database. Tier 1 rebate for under 65s of 16.079% applied.

Weighing up your options

While many Australians prefer to pay the Medicare levy surcharge instead of private hospital cover, it’s important to understand your options.

- The public hospital system remains free for all. All Australians have access to the public hospital system when they need it, regardless of whether they do or don’t have private hospital insurance. Having insurance does not mean you have to go to a private hospital, while in a public hospital, you can choose whether you want to enter as a private or public patient.

- An excess applies to private hospital treatment, which can be as much as $750 per person. This is typically payable once a year, but only if you're admitted to hospital in that calendar year. An excess doesn’t typically need to be paid for an ambulance visit, but it does if you opt to be admitted into a public hospital as a private patient.

- The Medicare levy surcharge can’t be avoided by taking out cover on 30 June. If your annual income exceeds the threshold for that financial year, including any fringe benefits and extra super contributions you’ve made, you are liable to pay the surcharge for every day in the financial year you did not hold hospital cover. If you need to pay the surcharge, it will be combined on your notice of assessment with the Medicare levy, listed as: Medicare levy and surcharge.

- Don’t overlook Lifetime Health Cover loading. This is an extra charge Australians must pay if they take out hospital cover later in life. The loading is calculated at a rate of 2% for each year a person doesn't have cover from the year they turned 31, capped at a maximum of 70%. This fee is only removed after someone has held continuous hospital cover for 10 years. While a basic policy can cost less than the Medicare levy surcharge, it also stops the clock on Lifetime Health Cover loading.

- Basic hospital cover has extremely limited benefits, with partial cover for rehabilitation, hospital psychiatric services, and palliative care in a public hospital as a private patient. It typically also includes emergency ambulance cover in states where the cost is not covered by the government, which is over $1k per trip in most states.

Emergency ambulance | |

|---|---|

Region | Cost |

NSW | From |

VIC | Metro: $1,437 |

QLD | No cost |

SA | From |

WA | $1,253 |

TAS | No cost |

NT | From |

ACT | From |

Source: Canstar. Based on a life-threatening emergency. Exclusions and per km charges apply in some areas.

Think about which strategy to employ

Canstar's Data Insights Director, Sally Tindall, says, “The Medicare levy surcharge is fast becoming a thorn in the side of thousands of Australians who are getting hit with this extra cost at tax time. In some cases, it could be turning a tax return into a bill they weren’t expecting.”

“While the Medicare levy surcharge income threshold is on the rise to $105,001. What people might not realise is that it’s based on your income and any fringe benefits or extra super contributions that you’ve made in the financial year.

“Anyone who thinks they might end up over next financial year’s threshold who doesn’t yet have private hospital cover should think about which strategy they want to employ.

“Our research shows taking out the cheapest basic hospital cover is likely to be on par with, or cheaper, than paying the extra government tax, but only if you haven’t yet racked up a mountain of lifetime cover loading charges on the way through.

“It’s also worth realising that holding a basic policy tends to cover you for basically nothing. You might get ambulance trips included, which can be helpful if your local ambulance service charges a fee, but very little else, with just restricted cover for hospital psychiatric services, rehab, and palliative care, which typically includes paying an excess.

“Canstar’s research found that for the cost of a coffee each week, on average, you could upgrade from basic to bronze, giving you both tax protection and greater peace of mind.

“For many, the decision is more than a simple maths problem for the next financial year. It’s a bigger picture look at whether they want cover in the years ahead and at what level.

“Australia has a robust public health system that has your back, particularly in an emergency. For many, that’s more than enough, even if they have to pay an extra tax for not having private cover. However, others would rather the choice of both options – public and private.

“What’s important to understand is that taking out private hospital cover does not mean you're locked into being treated as a private patient. You can still use the public system and opt for private treatment as and when you want it.”