NAB the second big bank to hike fixed rates in 2026 as lenders pre-empt cash rate decision

Big four bank, NAB, has today hiked fixed rates by up to 0.40 percentage points, as banks continue to factor in the possibility of a cash rate hike, potentially as soon as February.

This is the second time NAB has increased its fixed rate in six weeks, and follows fixed rate hikes from CBA last Thursday.

← Mobile/tablet users, scroll sideways to view full table →

| NAB’s lowest fixed rate changes | |||

|---|---|---|---|

| Term | Old rate from | New rate from | Change %-pts |

| 1-year | 5.39% | 5.74% | +0.35 |

| 2-year | 5.39% | 5.79% | +0.40 |

| 3-year | 5.44% | 5.84% | +0.40 |

| 4-year | 5.79% | 5.99% | +0.20 |

| 5-year5 | 5.79% | 6.09% | +0.30 |

Source: Canstar – 23/01/2026. Rates based on owner-occupier fixed-rate loans. LVR requirements apply.

As a result of these changes, ANZ now offers the lowest fixed rate out of the majors at 5.44% for a 2-year term.

← Mobile/tablet users, scroll sideways to view full table →

| Big four banks’ lowest fixed rates | ||||

|---|---|---|---|---|

| CBA | Westpac | NAB | ANZ | |

| 1-year | 5.94% | 5.49% | 5.74% | 5.49% |

| 2-year | 5.79% | 5.59% | 5.79% | 5.44% |

| 3-year | 6.04% | 5.69% | 5.84% | 5.64% |

| 4-year | 6.09% | 5.89% | 5.99% | 5.89% |

| 5-year | 6.24% | 5.89% | 6.09% | 5.89% |

Source: Canstar. Rates based on owner occupier fixed rate loans. LVR requirements apply.

Fixed rates continue to rise with the tide

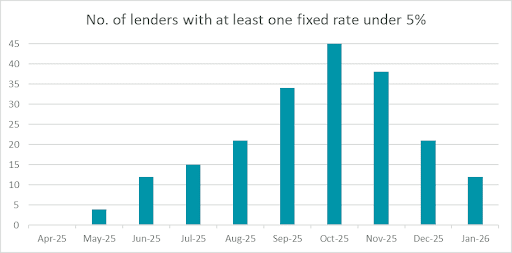

Canstar rate tracking shows a total of 54 lenders have hiked at least one fixed rate since the last cash rate decision on December 9.

There are now just 12 lenders offering a fixed rate below 5%, down from 38 two months ago.

Fixed rates under 5 per cent could be relegated to the past within weeks

Canstar data insights director, Sally Tindall, says, “Fixed rates continue to steadily march north with NAB the latest big bank to hike rates, this time by up to 0.40 percentage points.”

“When the RBA Governor says a cash rate hike is a live option, banks take notice, and so it’s no surprise to see 54 of the lenders on Canstar have hiked at least one fixed rate since the last RBA board meeting, including all of the majors.

“Fixed rates are surging out of the 4’s, and well into the 5’s and 6’s. As a result, there are now just 12 lenders offering a fixed rate under 5 per cent – a significant retreat from the 38 recorded two months ago.

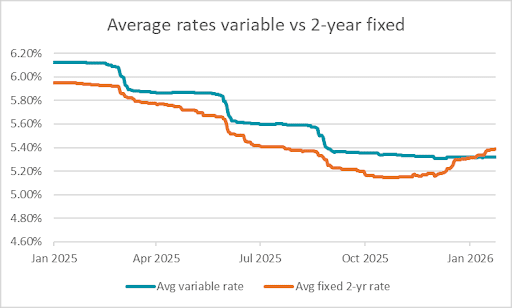

“While the majority of borrowers are on a variable rate and intend on sticking with this strategy, the mass migration of fixed rates is a pre-emptive move by the banks to counter a higher cash rate in 2026. This is yet another sign borrowers need to start getting prepared.

“A rate hike in 2026 is not a foregone conclusion, but yesterday’s ABS Labour Force data certainly isn’t standing in the central bank’s way. The bottom line is, Australia still has an inflation problem, four long years into this battle.

“Next Wednesday’s quarterly inflation results will be critical to the Board’s decision-making. If it shows we’re making genuine inroads towards the mid-point of 2.5 per cent, then it should be enough to fend off a hike in February. However, if inflation is just spinning on its wheels, or worse still, on the rise, then we’ll more than likely see a hike.

“For those still hoping to fix under 5 per cent, know you could be on borrowed time. Fixed rates under 5 per cent could be relegated to the past within weeks.

“If you are thinking about fixing, know the window is closing, but don’t cut corners in your due diligence. Fixed rates come with plenty of extra rules and caveats, such as caps on extra repayments, often no access to an offset account and break fees if you want to get out early. These are all things you’ll need to weigh up before you lock in.”

This article was reviewed by our Finance Editor Jessica Pridmore before it was updated, as part of our fact-checking process.