5 small changes that could make you $120,000 richer in retirement

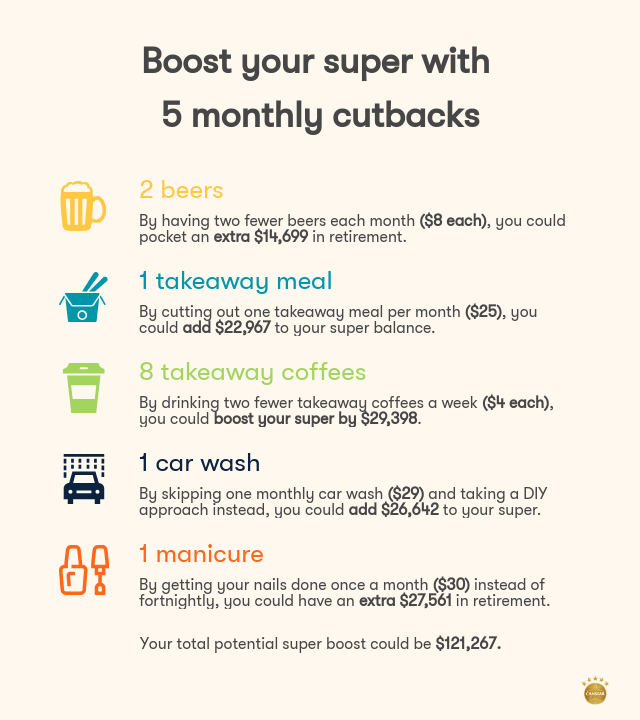

By cutting down on just one takeaway meal a month, you could be almost $23,000 richer by the time you reach retirement. By skipping your daily latte once in a while, you could save over $29,000.

These are just some of the small changes you could make that could boost your retirement balance by tens of thousands of dollars if you’re willing to put that extra cash into your super instead, Canstar’s analysis found.

Of course, there are plenty of ways to save money without giving up your caffeine fix or resisting a takeaway meal after a long day. The point is – when it comes to your super, a little can go a long way.

This is thanks to the power of compounding, where you can earn investment returns on top of returns your super may have already made. It means that the sooner you start socking a little bit extra away, the better.

We crunched the numbers to see how much better off you could be if you gave up some of life’s little luxuries every once in a while. This scenario assumes you are currently 30 years old and will retire at 67.

How much can you save by cutting back on spending?

Canstar Research has estimated potential savings based on a hypothetical individual cutting back on five example costs. Even if these exact items don’t match your spending habits, it may still help give you an idea of the difference small changes could make by the time you retire.

Source: www.canstar.com.au. Prepared on 15/07/2021. Scenario begins at the start of the 2021-22 financial year and is based on a 30-year-old with a starting balance of $25,096 (per APRA Annual Superannuation Bulletin), starting gross annual income of $74,516 (per ABS Characteristics of Employment – median employee earnings), and retiring at age 67. SG Contribution amounts per Government-announced rates, and along with the extra after-tax contributions, is assumed to be paid into superannuation fund quarterly. Employer contributions are assumed to be taxed at 15%. Net investment returns assumed to be 7.48% p.a. based on the average annual 5-year return of balanced investment options available for a 30-year-old on Canstar’s database (with returns effective to 31 May 2021). Average life and TPD insurance premium of $289.33 is assumed charged at the end of each year based on products available for a 35-year-old on Canstar’s database. Annual income, after-tax contributions and insurance premiums are assumed to increase with inflation each year. Inflation is assumed to be 2.5% p.a. due to the rising cost of living plus a further 1.5% p.a. due to the cost of rising community living standards (per the Moneysmart Superannuation calculator). End balance at retirement is shown in “today’s dollars”, i.e. it has been adjusted for inflation. Please note all information on income and superannuation performance returns are used for illustration purposes only. Actual returns and the value of your investment may fall as well as rise from year to year; this example does not take such variation into account. Past performance is not a reliable indicator of future performance.

By going without two beers ($16), one takeaway meal ($25), eight takeaway coffees ($32), one car wash ($29) and one manicure ($30) per month, you could save around $132 per month or about $33 a week. If you put those savings into your super as extra contributions instead, you could have an extra $121,267 by the time you retire.

How do you make extra contributions to your super?

You can make extra contributions to your super from your after-tax pay. These are known as non-concessional contributions. It’s usually as simple as setting up a direct debit from your bank account or BPAY.

You can currently make up to $110,000 in non-concessional contributions each financial year. But, by using the bring-forward rule, you may be able to contribute up to $330,000 to your super per year.

Low and middle income workers may be able to give their super an extra boost through the government’s super co-contribution. If you are eligible, the government will match up to 50% of your after-tax contributions (up to $500).

You may also be able to claim a tax deduction for your personal contributions. However, this will affect your eligibility for the super co-contribution. The Australian Taxation Office (ATO) notes that your contributions will then be counted towards your concessional contributions cap (currently $27,500 per financial year) and will be subject to 15% tax when they go into the fund.

You’ll need to let your fund know that you are intending to claim a deduction. The ATO has a notice of intent form that you can give your super fund or your fund may provide a form that you can fill out.

Another option is making additional contributions from your before-tax pay through a salary sacrificing arrangement with your employer. Your employer will pay part of your pre-tax salary into your super as a contribution. It will typically be taxed at 15%, the ATO says, which may be lower than your marginal tax rate.

How else can I boost my super balance?

If you’re not able to make extra contributions to your super, you can still help out your future self by looking for a better performing super fund, bearing in mind that past performance doesn’t necessarily mean a fund will repeat that performance in the future.

The average return for a balanced fund is currently 7.48%, but by switching to a fund that gives returns of just 1% more (8.48%) you could give yourself an extra $201,927 in retirement. It’s another relatively small change that could make a big difference to your retirement fund.

You should also check the fees you are being charged and make sure you aren’t paying too much. If you have multiple super accounts, you could consider consolidating them into one account so you aren’t doubling up on fees. You can do this through the ATO via myGov or your super fund may offer a consolidation tool. Lastly, it’s worth considering your investment options and making sure your investments suit your life stage and risk appetite. You may want to get professional advice to help you.

Cover image source: Efetova Anna/Shutterstock.com

This article was reviewed by our Sub Editor Jacqueline Belesky and Deputy Editor Sean Callery before it was updated, as part of our fact-checking process.

Try our Superannuation comparison tool to instantly compare Canstar expert rated options.