Headline and trimmed mean inflation have risen for the third quarter in a row, putting pressure on the RBA to hike the cash rate for the third time in three meetings.

However, the decision is not a foregone conclusion, with other indicators such as consumer confidence suggesting households have their purse strings firmly shut amid recession fears.

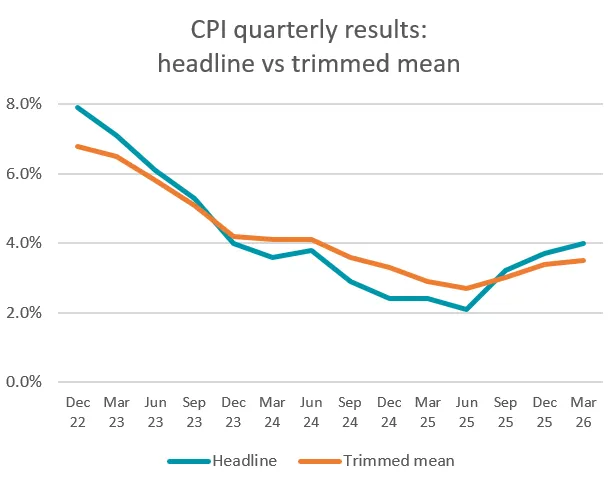

Today’s ABS results

Looking at the monthly dataset, headline inflation jumped to an annual rate of 4.6% in March, up from 3.7%. However, this was primarily due to two volatile factors: electricity, which rose to an annual rate of 25.4% on the back of the end of the rebates, and fuel prices, which rose 24.2% as a result of the war in the Middle East, and 32.8% between February and March.

Trimmed mean, which removes much of the volatility, stabilised in March at 3.3% in seasonally adjusted terms. However, looking across the quarter, it rose to 3.5% – the third rise in three consecutive quarters.

ABS CPI - Monthly | ||

|---|---|---|

Annual rate | Change from | |

Headline | 4.6% | up from 3.7% |

Trimmed | 3.3% | steady |

Source: ABS CPI Appendix 1a, seasonally adjusted data.

ABS CPI - Quarterly | ||

|---|---|---|

Annual rate | Change from | |

Headline | 4.0% | up from 3.7% |

Trimmed | 3.5% | up from 3.4% |

Source: ABS CPI Appendix 1a, seasonally adjusted data.

Big four banks all expect May cash rate hike

All four big bank economic teams are forecasting a 0.25 percentage point cash rate hike next Tuesday.

CBA, NAB and ANZ expect the cash rate to remain on hold thereafter, while Westpac predicts there will be two more in June and August.

Current big four bank | ||

|---|---|---|

Bank | Forecast | Cash rate |

CBA | 1 x 0.25 May | 4.35% |

Westpac | 3 x 0.25 in May, | 4.85% |

NAB | 1 x 0.25 May | 4.35% |

ANZ | 1 x 0.25 May | 4.35% |

Impact of a 0.25 cash rate hike in May

For someone with a $600,000 mortgage and 25 years remaining at the start of the hikes, a 0.25 percentage point cash rate hike in May would increase a borrower’s monthly repayments by $91.

Across what would then be three hikes for the year in February, March and May, the total increase would be $272.

Impact of three | ||||

|---|---|---|---|---|

Debt | Feb | March | May | Total |

$600,000 | +$90 | +$91 | +$91 | +$272 |

$800,000 | +$120 | +$121 | +$122 | +$363 |

$1 million | +$150 | +$151 | +$152 | +$453 |

Source: Canstar. Based on an owner-occupier paying principal & interest with 25 yrs remaining in Feb 2026 on the RBA av. variable rate. Calculations assume banks pass on the hikes the month after. Changes are to minimum repayments.

Some repayment buffers could vanish if the RBA hikes on Tuesday

A further 0.25 percentage point rate hike, should it materialise next week, could wipe out repayment buffers households have built over the past year.

That's because borrowers who kept repayments the same despite last year’s three 0.25 percentage point cash rate cuts would effectively be back where they started. This is likely to affect a large share of customers with CBA, NAB and ANZ home loans, as these banks held direct debits steady after each cut, unless borrowers actively reduced them.

Borrowers should brace for higher repayments and act now, particularly if Westpac’s cash rate forecast plays out, because the window to get ahead of further increases is closing fast.

How Australia’s inflation and cash rate compare around the world

Australia stands out with one of the highest cash rates around the world at 4.10%, following back-to-back hikes, while inflation remains relatively elevated compared to economies globally.

At the same time, unemployment is comparatively low in Australia, highlighting a resilient labour market.

Cash rates, | |||||

|---|---|---|---|---|---|

Official | Last | Headlin | Core | Unemployment | |

Australia | 4.10% | (+0.25%) | 4.60% | 3.30% | 4.30% |

United | 3.75% | (-0.25%) | 3.30% | 3.10% | 4.90% |

United | 3.50% - | (-0.25%) | 3.30% | 2.60% | 4.30% |

Canada | 2.25% | (-0.25%) | 2.30% | 2.20% | 6.70% |

New | 2.25% | (-0.25%) | 3.10% | 2.70% | 5.40% |

European | 2.15% | (-0.25%) | 2.60% | 2.30% | 6.20% |

Japan | 0.75% | (+0.25%) | 1.50% | 2.40% | 2.70% |

Source: Canstar. Notes: ECB refers to the main refinancing options.

Households already feeling the strain

Canstar's Data Insights Director, Sally Tindall, says, “Today’s CPI figures are undeniably hot and could be enough to push the RBA into firing off a third consecutive hike.”

“One of the central bank’s primary roles is to keep prices in check and right now, its report card is looking pretty precarious. Four long years into the battle with high inflation and quarterly trimmed mean inflation has just clocked up its third rise in a row.

“Another hike on Tuesday would help get the inflation job done, but at what cost? This is what will be weighing heavily on the Board’s mind. Push too hard and the economy could buckle.

“Many households are already feeling the strain. Consumer confidence is sitting deep in the doldrums and Australians have already tightened their purse strings on the back of higher petrol prices and global uncertainty.

“The March Board decision was clearly on a knife’s edge, with a five-four split in favour of a hike. When the Board is that divided, it tells you just how finely balanced things are now.

“Such a narrow vote at the last meeting suggests the Board might be more cautious about backing up with another increase, particularly when more recent data points to a nation that has already made significant spending cutbacks.

“A hike on Tuesday would effectively neutralise all three of the rate cuts we saw in 2025, taking the cash rate back to where it was at the start of last year.

“For those borrowers who didn’t adjust their repayments when the cash rate was on the way down, a hike on Tuesday will spell the end of this repayment buffer.

“For those paying the minimum, a 0.25 percentage point increase in May would add about $91 a month to their monthly repayments on a $600,000 loan with 25 years remaining. Across what would then be three hikes, the total increase would tally up to $272, not as a one-off hit, but every single month for the foreseeable future.

“Do the maths on a hike on Tuesday. In fact, do the maths on a further three cash rate hikes as per Westpac’s forecast and make sure you can clear this amount. While this prediction is still an outlier, it’s better to be overcooked on the mortgage than underdone.”