ANZ has today cut its 2- and 3-year fixed home loan rates by up to 0.10 percentage points, a move in the opposite direction from its big four bank peers.

As a result, the bank’s lowest fixed rate is now 6.29% for a 2-year term.

ANZ fixed rate cuts | |||

|---|---|---|---|

Term | Old rate | New rate | Change |

2-year | 6.39% | 6.29% | -0.10 |

3-year | 6.54% | 6.49% | -0.05 |

Source: Canstar - 05/06/2026. Rates based on owner-occupier fixed-rate loans. LVR requirements apply.

ANZ is not the only bank that has reverted back to fixed rate cuts. Australia’s fifth largest lender, Macquarie Bank, has also made sweeping cuts to its fixed rates today, dropping its lowest rate to 6.09% for a 3-year term.

Macquarie fixed rate cuts | |||

|---|---|---|---|

Term | Old rate | New rate | Change |

1-year | 6.44% | 6.19% | -0.25 |

2-year | 6.54% | 6.14% | -0.40 |

3-year | 6.59% | 6.09% | -0.50 |

4-year | 6.64% | 6.29% | -0.35 |

5-year | 6.74% | 6.29% | -0.45 |

Source: Canstar - 05/06/2026. Rates based on owner-occupier fixed-rate loans. LVR requirements apply.

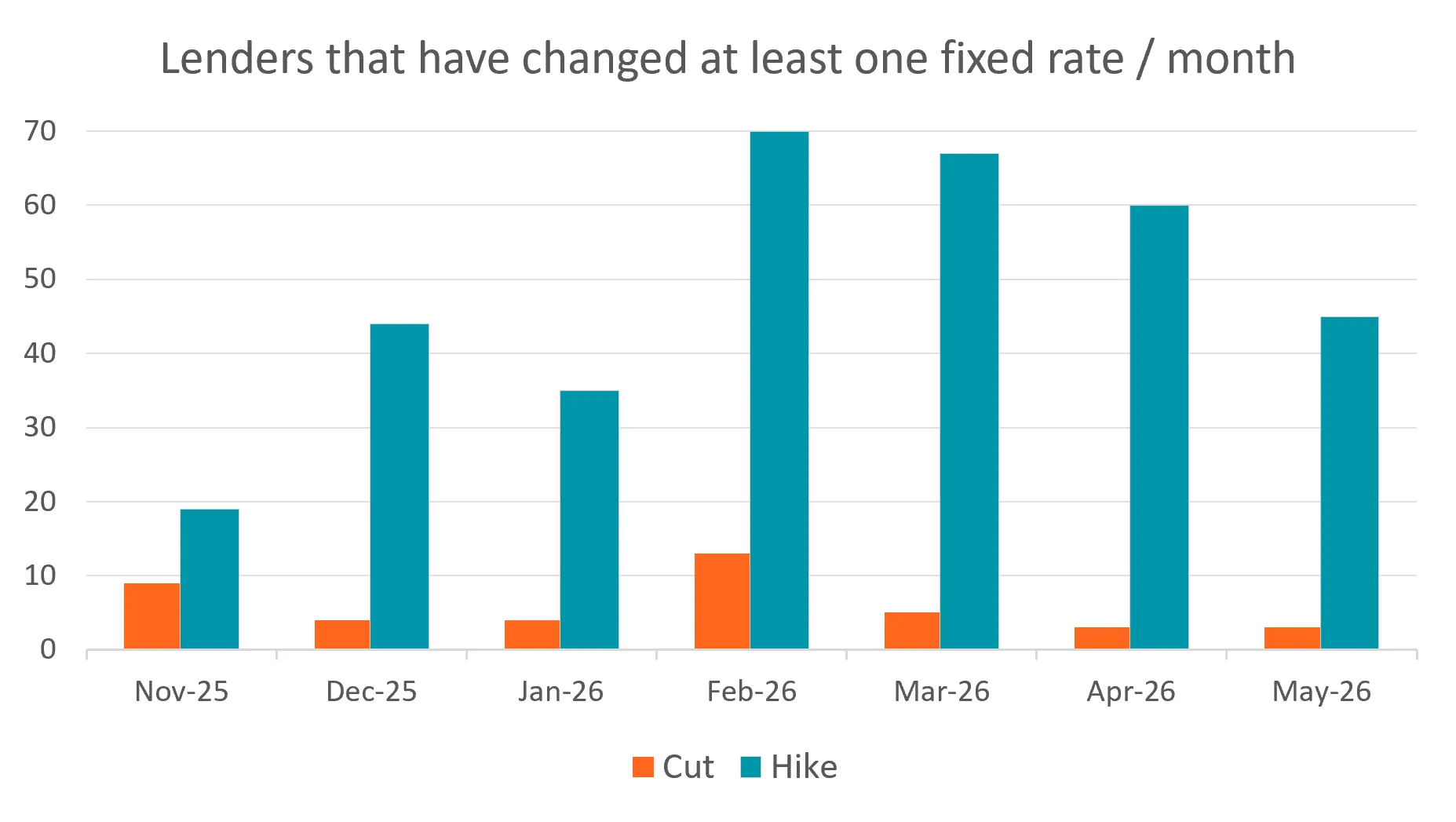

Majority of lenders still hiking

ANZ and Macquarie Bank’s cuts today go firmly against the tide, following months of fixed rate hikes from lenders big and small.

Just yesterday, Australia’s second largest bank, Westpac, hiked select fixed rates, albeit by a minor 0.05 percentage points, while NAB hiked fixed rates last Friday.

Out of Australia’s five largest lenders, Macquarie now has the lowest fixed rate at 6.09% for a 3-year term, followed by ANZ with a rate of 6.29% for 2 years.

Big four banks + Macquarie | |||||

|---|---|---|---|---|---|

CBA | Westpac | NAB | ANZ | Macquarie | |

1-year | 6.49% | 6.44% | 6.49% | 6.34% | 6.19% |

2-year | 6.34% | 6.34% | 6.54% | 6.29% | 6.14% |

3-year | 6.59% | 6.54% | 6.49% | 6.49% | 6.09% |

4-year | 6.64% | 6.69% | 6.49% | 6.54% | 6.29% |

5-year | 6.79% | 6.69% | 6.49% | 6.59% | 6.29% |

Source: Canstar. Rates based on owner-occupier fixed rate loans. LVR requirements apply.

Uncertainty around the future of the cash rate playing a role

While the majority of economists expect the cash rate to remain on hold following the RBA’s June meeting in 11 days' time, the central bank’s next move is highly contested.

Westpac is still expecting two more cash rate hikes. NAB expects one further hike, while ANZ and CBA believe the cash rate has now peaked, with CBA pencilling in the prospect of two cash rate cuts in May and August next year.

Current big four bank | ||

|---|---|---|

June | Forecast | |

CBA | Hold | 2 x 0.25 cuts in |

Westpac | Hold | 2 x 0.25 hikes, |

NAB | Hold | 1 x 0.25 hike, |

ANZ | Hold | No change |

Majority of fixed rates no longer competitive

After months of hikes, fixed rates have become far less competitive than variable.

At the start of the year there were 83 lenders offering at least one fixed rate under 6 per cent on the Canstar database. Today, there are just two. In comparison, there are still over 40 lenders offering at least one variable rate under 6 per cent.

On the Canstar database 90% of lenders’ lowest rates are variable, not fixed, and the gap is currently sitting at an average of 0.26%.

Lowest rates on | ||

|---|---|---|

Rate | Lender | Lowest rate |

Variable | LCU | 5.69% |

1-year | Northern Inland | 5.99% |

2-year | Pacific Mortgage | 6.14% |

3-year | Macquarie | 6.09% |

4-year | Macquarie | 6.29% |

5-year | Macquarie | 6.29% |

Source: Canstar. Rates based on owner occupier loans. LVR requirements apply.

Could fixing still come out ahead?

Canstar analysis shows if the average owner-occupier with a $600,000 debt and 25 years remaining took out the lowest 1-year fixed rate in the database, at 5.99%, instead of the lowest variable, at 5.69%, and the cash rate remained on hold for the next 12 months, then fixing would clearly fall behind.

However, if there were two more cash rate hikes, as Westpac is forecasting, then fixing would inch ahead, but only by $314.

Lowest 1-year fixed rate vs | |

|---|---|

No. of | Which comes out |

0 | Variable by |

1 more | Variable by |

2 more | Fixed by |

Source: Canstar. Based on an owner-occupier paying principal and interest with a $600k loan in June 2026 and 25 years remaining. Assumes further hikes are in August and September 2026. Calculations are for illustrative purposes only. They only reflect the interest charges and do not include fees or any extra repayments. Lowest rates exclude eco and introductory rate loans.

Banks are giving mixed signals

Canstar’s Data Insights Director, Sally Tindall, says, “ANZ and Macquarie have today shifted gears, cutting fixed home loan rates at a time when the majority of the market is still trending up.”

“While these cuts are modest, they are enough to put Macquarie and ANZ in front of their big bank competitors.

“The mixed signals from these fixed rate changes highlights just how uncertain the outlook remains.

“While two of Australia’s bigger banks might be cutting, fixed rates have a decent way to fall before they get back to being competitive.

“Right now there are just two lenders offering fixed rates under 6 per cent. In contrast, there are over 40 lenders with at least one variable rate under this mark.

“Canstar analysis shows that if the RBA delivers two more hikes this year, as forecast by Westpac, a borrower fixing at the lowest available rate would be an estimated $314 better off after a year compared to taking out the cheapest variable rate.

“That slim margin highlights the challenge facing borrowers hoping to fix. If rates stay on hold, the move is likely to cost them more. If rates rise further, fixing could potentially save money, but probably not enough to be considered a game changer.

“For many borrowers, the appeal of fixing isn’t about securing the lowest rate, but instead, locking in certainty.

“If that’s you, spend time looking for a competitive offer before you lock in, and as always, read the fine print so you’re fully across the limitations of a fixed rate mortgage.”