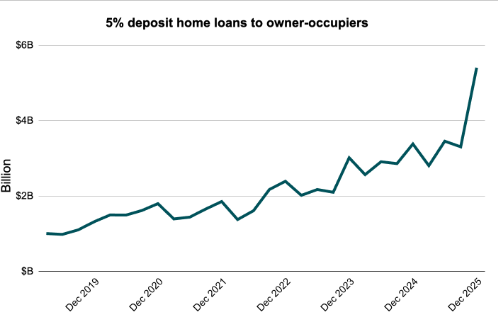

Low-deposit loans surge 63% following Home Guarantee stampede

The banks approved a record $5.4 billion worth of loans to owner-occupiers with deposits of 5% or less in the December quarter, following the uncapping of the government’s Home Guarantee Scheme.

This was an increase of $2.1 billion or 63% – the biggest spike in the history of the dataset – according to APRA property exposure statistics released yesterday.

The Home Guarantee Scheme, which lets first home buyers take out a loan with as little as a 5% deposit, was expanded on 1 October, with the removal of the cap on the number of places in the scheme and income people could earn to qualify.

These risky low-deposit loans now account for 4% of all new owner-occupier mortgages, the highest proportion on record since the APRA dataset began in 2019.

← Mobile/tablet users, scroll sideways to view full table →

| Value of owner-occupier mortgages taken out with 5% deposit or less | |

|---|---|

| December quarter | Change from Sept quarter |

| $5.4 billion | +$2.1 billion +63% |

Source: APRA Quarterly ADI Property Exposure statistics, prepared by Canstar.com.au. Based on all authorised deposit-taking institutions.

- Source: APRA Quarterly ADI Property Exposure statistics, prepared by Canstar. Based on all authorised deposit-taking institutions.

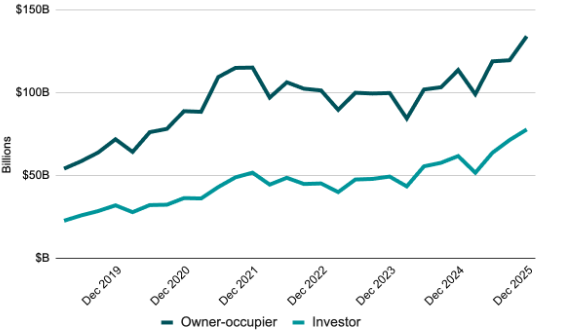

Borrowers continue to pile into already hot mortgage market

The total home loan market continued to surge in the December quarter with a record-breaking $211.9 billion in new loans written by the banks.

Owner-occupier lending had a bumper quarter, no doubt spurred on by first home buyer activity in the market, with a 12.1% increase in the three months to December.

However, looking over the year, investors out-paced owner-occupiers, growing by a staggering 25% from the previous year.

← Mobile/tablet users, scroll sideways to view full table →

| Value of new loans funded December 2025 quarter | |||

|---|---|---|---|

| Dec 25 quarter | Change from previous quarter | Change from Dec 24 quarter | |

| Owner-occupier | $134.1 billion – record high | +$14.5 billion +12.1% |

+$20.4 billion +17.9% |

| Investor | $77.8 billion – record high | +$6.3 billion +8.9% |

$16.0 billion +25.9% |

Source: APRA Quarterly ADI Property Exposure statistics, prepared by Canstar. Based on all authorised deposit-taking institutions.

Value of new residential mortgages per quarter

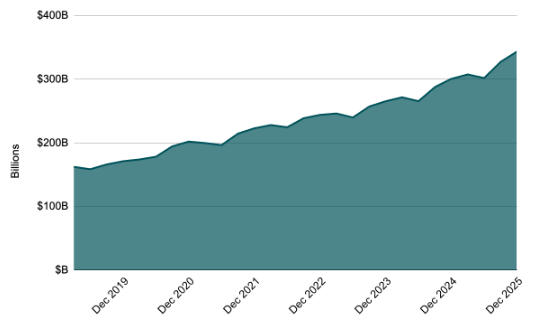

Offset balances hit record-breaking $343.5 billion

Australians continue to pile money into their offsets to mitigate the impact of their home loan rate and build up their rainy day buffer. The total amount in mortgage offset accounts now stands at $343.5 billion, with Australians stashing an additional $16.2 billion in their offsets in the space of three months.

Offset balances now account for 12.3% of credit limits owing across the mortgage books of authorised deposit-taking institutions, up from 11.9% in the September quarter.

← Mobile/tablet users, scroll sideways to view full table →

| Total amount in residential offset accounts | ||

|---|---|---|

| December 25 quarter | Change from previous quarter | Change from Dec 24 quarter |

| $343.5 billion – record high | +$16.2 billion +4.9% |

+$42.8 billion +14.2% |

Source: APRA Quarterly ADI Property Exposure statistics. Based on all authorised deposit-taking institutions.

Balances in offset accounts

High debt-to-income lending continues to accelerate

New lending with a debt-to-income ratio of six times or more, which is considered risky by the regulator, rose by $2.8 billion from the previous quarter. This risky lending now accounts for 6.8% of all new owner-occupier and investor lending, up from 5.5% six months prior.

The rise in this risky lending, and the marked acceleration in investor lending, prompted APRA to announce new caps on high debt-to-income (DTI) loans in November of last year, with the cap coming into effect on 1 February.

That said, it is well below both the new 20% cap and the record high back in late 2021 when over 24% of new loans had a DTI ratio of six times or more.

← Mobile/tablet users, scroll sideways to view full table →

| Loans with debt-to-income six times or more | ||

|---|---|---|

| Value of new lending | Share of all owner-occupier and investor loans | |

| June 2025 | $10.0 billion | 5.5% |

| Sept 2025 | $11.6 billion | 6.1% |

| Dec 2025 | $14.4 billion | 6.8% |

Source: APRA Quarterly ADI Property Exposure statistics. Based on all authorised deposit-taking institutions.

Canstar’s data insights director, Sally Tindall, says, “The Home Guarantee scheme has removed a key barrier for first home buyers who have surged on to the market, wafer-thin deposits in hand.”

“Saving a 20 per cent deposit had become an almost impossible task for many would-be buyers. This latest APRA data confirms new borrowers are now jumping at the option of a 5 per cent deposit loan.

“These loans now make up 4 per cent of new owner-occupier lending, which sounds small, but is actually the highest proportion on record. This won’t have passed the regulator by.

“Australians are continuing to stash large sums in their offset accounts, with balances hitting a record $343.5 billion.

“For mortgage holders who can afford it, parking spare cash in an offset is one of the most effective ways to cut interest costs while building a financial buffer. It helps soften the blow of last month’s rate hike and put households in a stronger position if the two additional hikes banks are forecasting materialise.

“Borrowers piled into the property market in the December quarter, with a record $211.9 billion worth of new home loans written in just three months.

“While owner-occupiers dominated in this quarter, over the year, investors posted the biggest growth, with the value of new investor loans 25 per cent higher than the same quarter a year ago.

“This staggering growth in investor lending has caught the eye of the regulator, as has the rise in loans with a debt-to-income ratio of six times or more, with APRA introducing a new limit on these mortgages.

“This new cap only kicked in on 1 February, so the real test will be whether investor activity starts to cool in the next set of data.”

This article was reviewed by our Consumer Editor Meagan Lawrence before it was updated, as part of our fact-checking process.