The nation is bracing itself for the prospect of a third consecutive rate hike at the end of the RBA Board meeting tomorrow, taking the cash rate back up to 4.35%, where it sat 16 months ago.

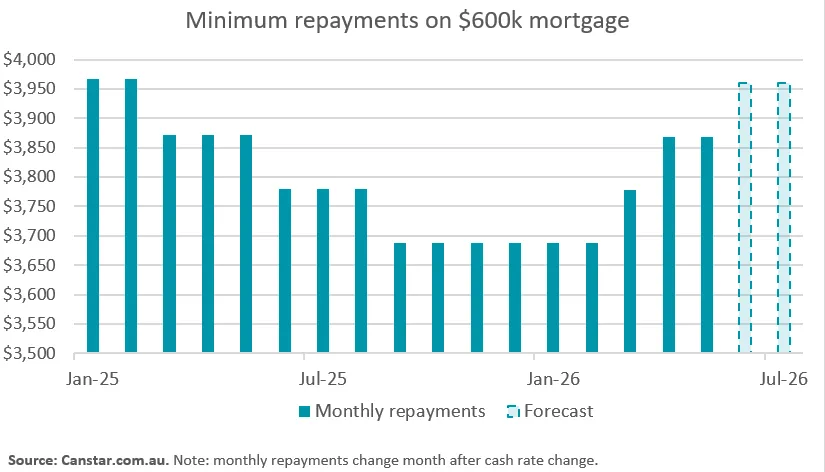

For an owner-occupier with a $600,000 mortgage and 25 years remaining at the start of this year’s hikes, another 0.25 rise in May would add $91 to their minimum monthly repayments. The total increase across the three hikes would be $272 a month.

Impact of a | ||

|---|---|---|

Debt | Hike in | Cumulative |

$500,000 | +$76 | +$227 |

$600,000 | +$91 | +$272 |

$700,000 | +$107 | +$317 |

$800,000 | +$122 | +$363 |

$900,000 | +$137 | +$408 |

$1 million | +$152 | +$453 |

Source: Canstar. Notes: based on an owner-occupier paying principal & interest with 25 years in Feb 2026 at the RBA avg variable rate. Calcs assume banks pass on hikes the month after. Changes are to min repayments.

Back to square one for many borrowers

A hike tomorrow to a cash rate of 4.35% would effectively finish unwinding last year’s three rate cuts and erase the repayment buffers many borrowers had built into their mortgages by not reducing their repayments across this time.

RBA hike to push average owner-occupier variable rate to 6.26%

A 0.25 percentage point hike tomorrow would push the average owner-occupier variable rate to 6.26%, taking it above 6.25% for the first time since January 2025.

That said, Canstar estimates there will still be over 40 lenders offering at least one variable rate below 6%, with the lowest rate likely to be at or below 5.75%.

Estimated owner-occupier | |

|---|---|

Average | 6.26% |

Competitive | below |

Lowest | sub |

Source: Canstar.com.au. Note: rates are estimates based on Canstar and RBA data.

Estimated investor | |

|---|---|

Average | 6.50% |

Competitive | 6.15% |

Lowest | sub |

Source: Canstar. See notes above.

Banks baking in May rate hike

Rate tracking by Canstar shows in April, 60 lenders hiked at least one fixed rate, a key indicator banks are factoring in at least one more cash rate hike.

Lenders that have changed | ||

|---|---|---|

Month | Cut | Hike |

Nov-25 | 9 | 19 |

Dec-25 | 4 | 44 |

Jan-26 | 4 | 35 |

Feb-26 | 13 | 70 |

Mar-26 | 5 | 67 |

Apr-26 | 2 | 60 |

Source: Canstar.com.au. Note: excludes green loans.

What should borrowers do?

- Run the numbers: Work out what your repayments would look like if the RBA hikes this week, but also if there are two further hikes in June and August, as Westpac is forecasting. While this forecast is an outlier, it’s worth preparing for.

- Ask for a better rate: Contact your lender and request a rate review. A 0.25 reduction can offset a hike, while 0.50 off your current rate will neutralise two.

- Consider switching: Haggling will only take your rate so far. Those who want the sharpest rates are likely to have to refinance.

- Know your support options: If repayments are becoming difficult and you’ve already negotiated with your lender, ask about hardship assistance. Also seek independent financial advice via the National Debt Helpline: 1800 007 007.

Millions of borrowers back to square one

Canstar’s Data Insights Director, Sally Tindall, says, “A rate hike tomorrow would essentially put millions of borrowers back to square one.”

“For those who kept their mortgage repayments the same following the cash rate cuts in 2025, the repayment buffer they had built up will be essentially erased by a third cash rate hike in 2026.

“While more than a year of higher repayments won’t have been in vain, the strategy will have delivered only a limited cushion against rising rates.

“Haggling should be borrowers’ first port of call, because picking up the phone can potentially produce near-immediate relief. However, banks aren’t handing out discounts as freely as they were a couple of years ago. If your bank won’t budge when you haggle, don't take it personally, instead, take your business elsewhere.

"Many borrowers are still wedded to the majors, but the sharpest rates sit firmly with the smaller players. If the RBA hikes the cash rate this week, most owner-occupier rates will start with a ‘6’, but we expect around 40 lenders will still offer at least one variable rate under this mark.

“You might not recognise most of the names in the list, but that shouldn’t automatically rule them out of consideration.

"If you are staring at your budget and the numbers simply don't work, act before you miss a repayment.

“Step one is calling your bank’s hardship team – they are legally required to assist. The options can range from interest-only or part-payments for a period, to extending out your loan term to bring monthly costs down.

“These tools might help you keep your head above water in the short term, but most come at a cost, so understand what it is and whether there’s a better alternative for your finances.”