The total value of residential home loans has hit another record high of $2.46 trillion in March, despite two cash rate hikes, which have taken some of the heat out of the property market.

APRA statistics, released yesterday, show housing loans among authorised deposit-taking institutions (ADIs) increased by $13.9 billion in March, up 0.6% from the previous month.

Macquarie recorded the largest monthly increase among all ADIs, rising by $3.6 billion or 2.1% in the month, consolidating its position as the fifth largest lender.

Loans to households: | ||||

|---|---|---|---|---|

Amount | Market | Monthly | Year-on-year | |

CBA | $624.5 | 25% | +0.5% | +7.1% |

Westpac | $509.0 | 21% | +0.5% | +5.3% |

NAB | $347.0 | 14% | +0.4% | +5.5% |

ANZ | $324.2 | 13% | +0.5% | +3.7% |

Macquarie | $173.7 | 7% | +2.1% | +27.1% |

All ADI | $2.46 | 100% | +0.6% | +6.9% |

Source: APRA Monthly Authorised Deposit-taking Institution Statistics, March 2026, released 30 April 2026, prepared by Canstar. Includes both owner-occupied and investor loans to households for the big four banks and Macquarie. ANZ figures do not include former Suncorp mortgages.

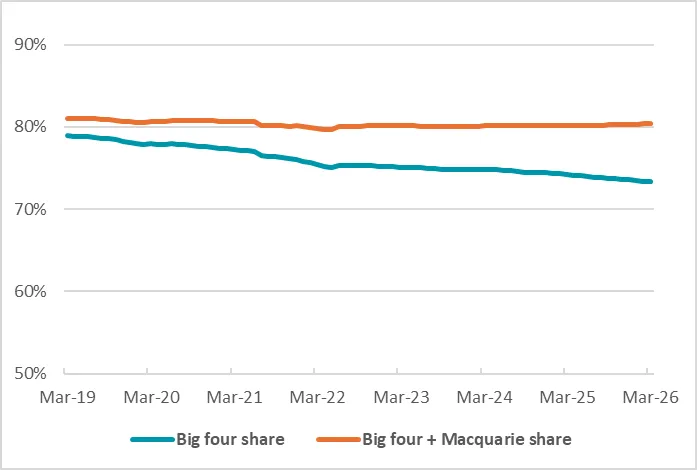

Big four banks lose ground to Macquarie

The big four banks currently hold 73% of household mortgages out of the banks – a noticeable slide from seven years ago, when they held 79% of the share.

Looking at the data, much of this ground has been conceded to Macquarie Bank, which has increased its residential mortgage book by an eye-watering 380% in this time. However, the bank still holds a relatively-small 7% share of all mortgages with ADIs.

Major banks market share – last seven years

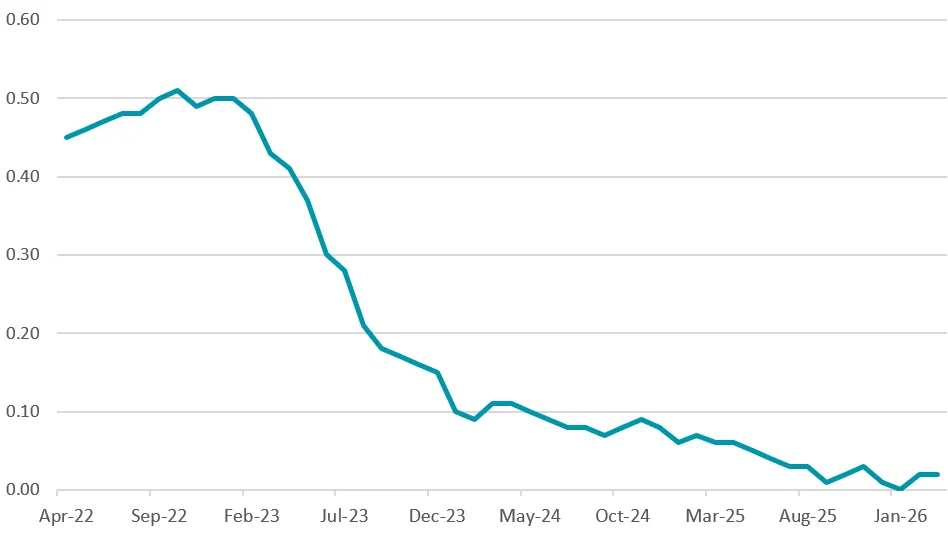

The fight for new customers softening

Unlike the last cash rate-hiking cycle, banks are not using as many perks and lures to win new customers. The sharp new customer discounting, big cashback offers, and out-of-cycle rate cuts that defined 2022 to early 2023 are largely absent.

ANZ is the only big four bank advertising a cashback offer, but this deal is limited to first home buyers.

New customer rate cuts have also fallen by the wayside. Canstar analysis shows the average new customer variable rate for owner-occupiers is estimated to be 5.98%, compared to the average existing customer rate of 6.00% – just 0.02 percentage points different.

This is a stark difference from October 2022, when new customers were getting, on average, a 0.51 percentage point discount compared to existing customers, as banks fought hard to win new business.

Difference between av. new and existing owner-occupier variable rates (%-pts)

Customers looking for the lowest rates will have to look beyond the big banks

Canstar shows around 42% of lenders still offer at least one variable rate below 5.75%, with Westpac the only big bank under this mark.

However, if the RBA fires off one more cash rate hike on Tuesday, this could drop to just a few lenders, if banks pass it on to customers as they are expected to do.

Lowest | |

|---|---|

Lender | Lowest rate |

LCU | 5.44% |

Horizon Bank*, | 5.49% |

Virgin Money, | 5.59% |

Source: Canstar. Rates based on owner occupier variable rate loans, excludes green loans. LVR requirements apply. *Horizon Bank and Police Bank rates are for first home buyers only.

Lowest variable rates | |

|---|---|

Lender | Lowest rate |

CBA | 5.84% |

Westpac | 5.74% |

NAB | 6.19% |

ANZ | 6.00% |

Macquarie | 5.84% |

Source: Canstar. Rates based on owner occupier variable rate loans, excludes green loans. LVR requirements apply.

Investor growth continues to outpace owner-occupiers, despite debt-to-income speed limits

Growth in investor mortgages was stronger than owner-occupier lending in March, with investor housing credit growing 1.0% compared to 0.4% for owner-occupied loans.

This growth comes despite APRA’s new 20% cap on new mortgages with debt-to-income ratios of six times or more, which came into effect on 1 February in a move predominantly designed to keep investor lending in check.

Loans to households: | |||

|---|---|---|---|

Amount | Monthly | Year-on-year | |

Owner-occupier | +$1.66 | +0.4% | +6.1% |

Investor | +$800.5 | +1.0% | +8.5% |

Source: APRA Monthly Authorised Deposit-taking Institution Statistics, March 2026, released 30 April 2026, prepared by Canstar.

Gone are the days of banks tripping over themselves to win new customers

Canstar's Data Insights Director, Sally Tindall, says, “Macquarie is eating into the big banks’ mortgage dominance and doing it at speed. While the majors are inching forward, Macquarie is taking big strides.”

“A 27 per cent jump in Macquarie’s loan book in just 12 months is solid growth, and a 380 per cent increase over five years is a land grab. The big banks still hold the lion’s share, but they’ve quietly lost ground over those past five years.

“At $2.46 trillion, the home loan market is hitting fresh records. Rate hikes might have taken some heat out of the market, but they haven’t stopped the overall loan book from climbing.

“Growth in investor lending is once again outpacing owner-occupiers in percentage terms, showing that appetite for property investment is holding firm despite higher rates and APRA trying to keep a lid on risky lending.

“The mortgage wars have cooled. The days of banks tripping over themselves to win new customers appear to be largely on ice.

“In the last rate hiking cycle in 2022 to 2023, banks were dangling cashbacks and sharp discounts to lure borrowers in – a phenomenon we’re not seeing much of this time around.

“Right now, there’s barely daylight between new and existing customer rates. People have been out there negotiating with their banks and switching to more competitive deals, which is fantastic to see. If you’re not one of these proactive mortgage customers, it could be time to turn yourself into a nuisance for your bank by piping up.”