The maximum amount people can borrow from the bank is set to drop within the next fortnight, following yesterday’s 0.25 cash rate hike.

Canstar analysis shows someone earning the average full-time wage of $106,950 will be able to borrow an estimated $12,000 less as a result of the March RBA rate increase, as lenders continue to announce they’re passing on yesterday’s cash rate hike to mortgage rates.

This is based on a person taking out an owner-occupier loan with no other debts, no dependents and minimum expenses.

Estimated decrease in borrowing capacity as a result of RBA hikes | ||

|---|---|---|

Borrower | Hike in March | Cumulative impact across March + Feb |

Individual (av. wage) | -$12,000 | -$25,000 |

Couple (2 x av. wage) | -$24,000 | -$49,000 |

Source: Canstar. Based on an owner-occupier taking out a 30-year loan at the average RBA rate. Assumes minimal expenses, no debts, no dependents, average wage based on ABS data. Borrowing capacity figures are estimates and can vary from lender to lender. See full notes below.

If a third hike materialises in May, as the big bank economists expect, the same person’s borrowing capacity could shrink by around $37,000 in total.

Estimated decrease in borrowing capacity after three RBA hikes | |

|---|---|

Borrower | Cumulative impact: March + Feb + May |

Individual (av. wage) | -$37,000 |

Couple (2 x av. wage) | -$73,000 |

Source: Canstar. Based on an owner-occupier taking out a 30-year loan at the average RBA rate with a 0.25 hike in May. Assumes minimal expenses, no debts, no dependents, average wage based on ABS data. See full notes below.

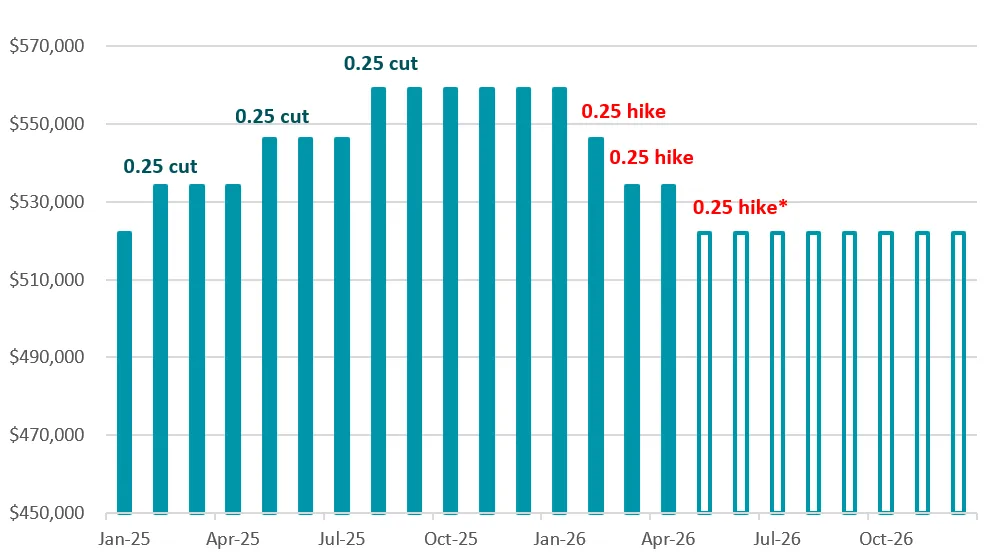

Estimated impact of RBA changes on borrowing capacity for person on average wage

Source: Canstar. * Forecasted RBA hike. Note: y axis starts at $450k.

Big banks all expect a rate hike in May

CBA, Westpac, NAB and ANZ all still expect a further 0.25 rate hike in May, which would take the cash rate to 4.35% – effectively wiping out the three rate cuts delivered in 2025.

Current big four bank cash rate forecasts | ||

|---|---|---|

Bank | Forecast | Cash rate at end of 2026 |

CBA | 1 x 0.25 in May | 4.35% |

Westpac | 1 x 0.25 in May | 4.35% |

NAB | 1 x 0.25 in May | 4.35% |

ANZ | 1 x 0.25 in May | 4.35% |

How to boost your borrowing capacity

There are ways to boost the maximum amount your bank will lend you and improve the chances of it green lighting your mortgage application.

- Ditch the credit card: If you have a credit card, ditch it, at least temporarily. It can lower your chance of getting approved for a mortgage, even if you don’t have a single cent owing on it.

- Clear any other loans you might have: A student debt that’s been hanging around like a bad smell, a car loan, even multiple buy now, pay later transactions can act as a red flag.

- Boost your income: A permanent part-time job or a pay rise in your existing job can go a long way in the eyes of the bank. Provided the money coming in is consistent, the bank should take it into consideration.

- Know that rate does matter: If you’re applying for the new estimated average rate of 6.01%, the bank will assess you at 9.01%. However, if you aim for one of the lowest rates at 5.60%, then you might be able to borrow $20k more, and still have lower monthly repayments despite the fact you’ve taken on more debt.

- Don’t bite off more than you can chew: These tips can help you get approved for a mortgage but don’t overlook the big picture which is how much debt you’re taking on and whether it's manageable.

Canstar’s data insights director, Sally Tindall, says, “Tuesday’s rate hike will slice roughly $12,000 off the average Australian’s maximum home buying budget. For couples joining forces on the property hunt, this one move has potentially lost them as much as $24,000."

She added: “Every rate hike doesn’t just hit borrowers in the hip pocket, it also quietly chips away at how much they can borrow. For many buyers, that can mean the difference between getting into the market or missing out altogether.

“If inflation continues to soar and the RBA is forced to hike again as soon as May, as the banks are forecasting, buyers could be staring down an almost $40,000 hit to their budgets in just four months.

“Right now, home buyers are facing the second highest cash rate setting this country has seen in the last 14 years, at the same time property prices in key areas continue to march north, albeit at a slower pace. This makes what was already a tricky equation a near-impossible puzzle to solve for many prospective home owners.

“Governor Bullock says the RBA doesn’t want a recession but may have to accept one to get inflation under control. This is a clear signal the fight against rising prices isn’t over yet. Prospective home buyers should factor in the high possibility rates will rise higher and stay that way for the foreseeable future.

“While borrowers can’t control the cash rate, they do have some levers they can pull. Knocking off existing debts, boosting your income and securing a sharper rate can make a difference to whether the bank green-lights your loan application or not.

“That said, pushing the envelope on how much debt you take on should not be done lightly. Banks have these checks and balances in place for a reason. It’s important you run these tests too so you know exactly how much your mortgage repayments would be at an interest rate that’s 3 percentage points higher. An unlikely scenario right now, but a mortgage can hang around for up to three decades and a lot can happen during this time.”

Borrowing power notes: Based on someone taking out a 30-year owner-occupier loan at the average new customer variable rate (RBA). Assumes $24k p.a. of expenses for one individual with no debts and no dependents. Income is based on the ABS weekly ordinary time full-time earnings in original terms. Does not factor in wages growth. Borrowing power based on 90% of post-tax income available to service the loan and expenses, and a 3.00% interest rate buffer. Tax calculations based on the current financial year, excluding Medicare Levy. Borrowers should seek personal financial advice before deciding how much to borrow and know the actual amount will vary depending on their personal circumstances and between lenders.