How to consolidate your super funds

About one in four people with super have an account with more than one fund which could see them losing out by paying multiple fees. Many people choose to consolidate their multiple super accounts into one fund as they plan for their retirement.

But consolidating might not always be possible, and it might not be right for you, so here are some of the things you need to consider.

How many people have multiple super funds?

More than 12.6 million people – about three out of four of the superannuation population – had only one super account at 30 June, 2022, according to the Australian Tax Office (ATO). The rest – about 3 million people – had two or more accounts. About 1% – or one in 100 – had four or more accounts.

Percentage of accounts held by an individual

→ Learn more: How to choose a super fund

If that’s you, you might want to consider consolidating your accounts. The ATO says you could be paying unnecessary fees and charges on these multiple accounts, and that could reduce your overall retirement income.

“Fewer super accounts usually means less fees and more money for your future,” an ATO spokesperson told Canstar.

The reason why you may have multiple accounts could be because you’ve changed jobs and your new employer opened up an account for you in its preferred or ‘default’ super fund. You don’t have to accept that preferred fund and can ask your employer to contribute to your existing super fund.

The number of people with multiple super accounts has declined over a four-year period as people opt to consolidate their accounts. The ATO says it’s easy to consolidate your super by using the myGov website, and we’ll explain how later.

Consolidated super accounts

Should you consolidate your super funds?

It may be helpful to seek some independent advice on whether consolidating your multiple super accounts is right for you, and which would be your fund of choice that meets your retirement plan.

Check to see if there is any life insurance or other benefits with any of the accounts and whether you’d lose those. You also need to check whether your employer contributes more than the minimum required to its preferred fund if you are thinking of consolidating away from that to one of your other funds.

Compare Superannuation with Canstar

The table below displays some of the superannuation funds currently available on Canstar’s database for Australians aged 30 to 39 with a super balance of up to $55,000. The results shown are sorted by Star Rating (highest to lowest) and then by 5 year return (highest to lowest). Performance figures shown reflect net investment performance, i.e. net of investment tax, investment management fees and the applicable administration fees based on an account balance of $50,000. To learn more about performance information, click here. Consider the Target Market Determination (TMD) before making a purchase decision. Contact the product issuer directly for a copy of the TMD. Use Canstar’s superannuation comparison selector to view a wider range of super funds. Canstar may earn a fee for referrals.

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Included

Included

Not included

Not included

Not applicable

Not applicable

Data not captured

Data not captured

Canstar Star Rating

Canstar Star Rating

Indicative Canstar Star Rating

Indicative Canstar Star Rating

In the end you may decide it’s in your interest to keep some or all your multiple accounts because of the benefits they provide, or you may decide it’s time to consolidate.

The Association of Superannuation Funds of Australia says the main reason why people haven’t consolidated their multiple accounts is because they haven’t got around to doing it. One in five people also said they didn’t know how to consolidate their accounts.

So if you do decide to transfer any of your multiple accounts into another fund, here’s what you need to know.

How to consolidate your super funds

There are several ways you can consolidate your multiple super accounts and perhaps the easiest is via the myGov website.

If you haven’t already signed up for an account, then you can do so at my.gov.au.

Once you’ve logged into your account, you can link to the ATO.

When you have done that:

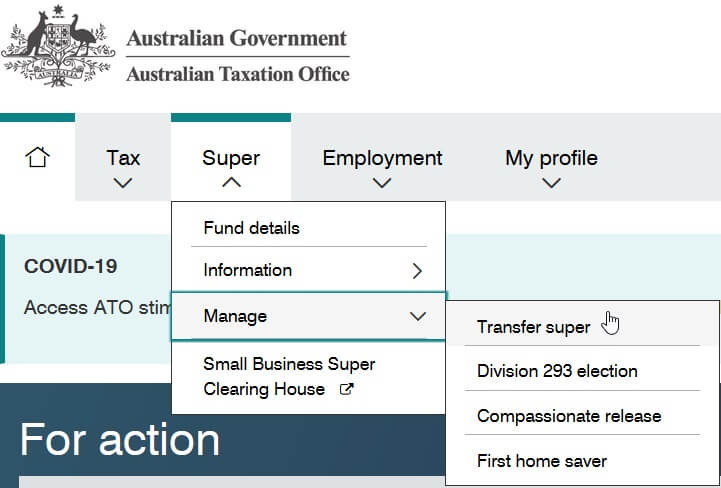

- Click through to the ATO.

- From the top menu, select the Super option.

- In the dropdown menu, select Manage.

- Then, select Transfer Super.

If you only have one super account registered with the ATO, or you have other funds that don’t allow funds to be transferred, you won’t be able to progress any further online. For example, the public sector super funds PSS and CSS don’t allow you to transfer your account to another fund.

If you think you should see multiple accounts, then you may need to check with each super fund provider to find out why the fund isn’t showing up.

“Remember to ensure that all of your contact information is up to date, both with the ATO and your super fund/s,” said the ATO spokesperson.

“This will help us reunite you with any unclaimed super accounts held by the ATO and reduce the chance that your super fund loses track of you.”

If you do see multiple accounts listed, you can then select the ones you wish to transfer, and to which account.

“About five minutes and a couple of clicks is all it takes, and it could save you hundreds or even thousands of dollars,” said the spokesperson.

If you don’t want to consolidate the accounts online via the myGov website, then you can contact the provider of the account you wish to transfer from, and get them to help.

Or you use the ATO’s rollover request form.

What does your employer need to know about your preferred super?

Whatever you decide to do with your multiple super accounts, make sure you tell your current employer so it can pay its contribution into your preferred fund.

→ Learn More: What superannuation details does your employer need?

If you don’t, and your employer’s preferred fund is one you’ve transferred away from and now closed the account, this could cause problems.

The ATO says this could result in your employer making those contributions to its own default fund.

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Online rollover

Online application

Included

Not included

Not applicable

Data not captured

Canstar Star Rating

Indicative Canstar Star Rating

Cover image source: maradon 333/Shutterstock.com

This article was reviewed by our Deputy Editor, Canstar Amanda Horswill before it was updated, as part of our fact-checking process.

Try our Superannuation comparison tool to instantly compare Canstar expert rated options.