A third cash rate hike remains firmly on the cards, with the latest round of CPI data confirming Australia’s inflation rate remains well above target.

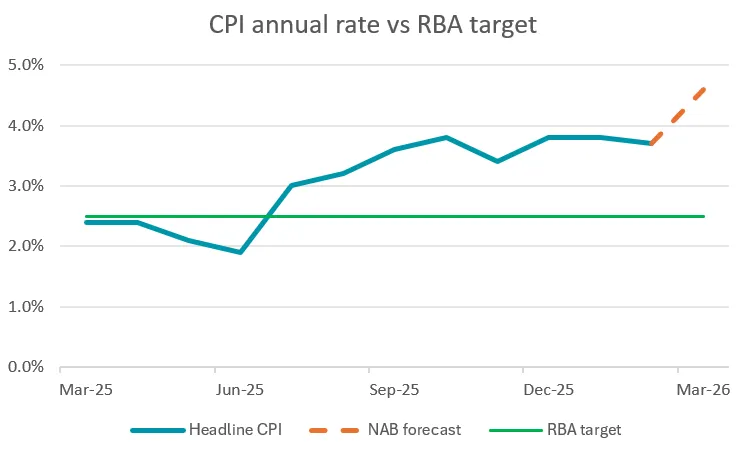

Data from the ABS for February, released today, saw headline inflation drop from an annual rate of 3.8% to 3.7%, while core inflation remained relatively steady at 3.3% p.a, where it has broadly been hovering for the last six months.

Add in the current oil crisis, which was not captured by today’s data, and the picture deteriorates dramatically, with NAB economists forecasting headline inflation could spike in March to an annual rate of 4.6%.

CPI: last six months, annual movement | ||

|---|---|---|

Month | Headline CPI % | Trimmed mean % |

September 2025 | 3.6 | 3.2 |

October 2025 | 3.8 | 3.3 |

November 2025 | 3.4 | 3.2 |

December 2025 | 3.8 | 3.3 |

January 2026 | 3.8 | 3.3 |

February 2026 | 3.7 | 3.3 |

Source: ABS.

What would another cash rate hike mean for borrowers?

A further cash rate hike in May, as is predicted by all four big banks, could add an extra $91 a month to a $600,000 debt with 25 years remaining.

Over what would then be three hikes in three meetings, Canstar analysis shows this borrower would see their monthly repayments rise in total by $272 a month.

That’s an estimated increase of 7.4% in just four months – that’s double Australia’s current annual inflation rate, across a much shorter time period.

Potential impact of rate hikes if the cash rate gets to 4.35% | |||

|---|---|---|---|

Loan size start of hikes | Hike in May | Total increase across three hikes | New monthly repayment |

$600,000 | +$91 | +$272 | $3,960 |

$800,000 | +$122 | +$363 | $5,280 |

$1 million | +$152 | +$453 | $6,600 |

Source: Canstar - Notes: based on an owner-occupier paying principal and interest with 25 years remaining in Feb 2026 at the RBA average existing customer variable rate. Calculations assume the RBA hikes the cash rate in May 2026 and banks pass on the Feb, March and May hikes the month after.

How many rate hikes can you avoid by haggling?

Canstar analysis shows that if a typical owner-occupier took out a loan five years ago and hasn’t negotiated since, they would be on a variable rate of 6.78%.

If, with $600,000 owning, they knocked 0.50 off their rate, their monthly repayments would drop by $188. This would effectively undo the February and March hikes and save them more than $6,000 in interest over the next two years.

While getting down to 5.75% is unlikely by negotiation alone, refinancing could achieve it. Canstar research shows around 40 lenders are expected to offer at least one variable rate below this mark, potentially saving the borrower as much as $11,205 over two years, even after factoring in $1,150 in switch costs.

Potential savings from haggling and refinancing: $600k loan | |||

|---|---|---|---|

Rate | Drop in repayments | Cost saving - next 2 yrs | |

Do nothing | 6.78% | ||

Haggle (0.50 cut) | 6.28% | -$188 | -$6,002 |

Refinance (1.03 cut) | 5.75% | -$382 | -$11,205 |

Source: Canstar - Notes: based on an owner-occupier paying principal and interest with 25 years remaining in April 2026. Rates are estimates based on RBA data. Assumes there is one further cash rate hike in May and that the banks pass it on a month after. Repayment amounts are minimum monthly repayments. Refinancing scenario assumes $1,150 in switch costs.

The 3 things you can say to help get a decent cut:

- Mention you are considering refinancing: Let them know you’ve been researching lenders and name-drop rates you’ve seen. If they know you’ve done your homework, they should take the request more seriously.

- Ask to speak to the retention team: They are the ones with the authority to hand out bigger discounts.

- If they still don’t budge, ask for a mortgage discharge form: This signals you’re serious about leaving and may prompt them to come back with a better offer.

Canstar data insights director, Sally Tindall, says, “Today’s CPI figures offer little reprieve in the fight against inflation.”

“There’s no calm before the storm, but instead, persistent inflation that is set to spike once the Middle East conflict hits next month’s data, just six days out from the RBA’s next meeting.

“If the RBA ratchets up the cash rate lever for the third time in as many meetings, borrowers will be back to the highest cash rate setting since November 2011.

“This would translate into a 7.4 per cent increase in a typical borrower’s monthly repayments, on top of which will almost certainly be elevated petrol, grocery and services costs.

“While a lot of the noise is coming from the sharp rise in electricity prices, with the data recording an annual rise of 37 per cent primarily due to the end of the government rebates, that’s still a financial hit households are having to work through.

“What’s particularly frustrating for borrowers is that they’re the ones that get forced to do much of the heavy lifting in the fight against inflation.

“The silver lining here is that borrowers aren’t powerless. Many are sitting on uncompetitive rates, simply because they haven’t picked up the phone.

“Haggling with your bank could potentially wipe out the last two rate hikes. In today’s environment, a 10-minute phone call could be worth thousands.

“Getting down to a rate below the 6 per cent mark is unlikely by haggling alone. However, refinancing could potentially achieve this. Canstar estimates that there will still be around 40 lenders offering at least one variable rate under 5.75 per cent after the March hike filters through.

“Banks are still keen to hold onto quality customers, but they’re unlikely to hand you a discount unprompted. You need to be prepared to ask, and if necessary, be willing to walk.”