The majority of variable borrowers across the country have had their mortgage rate increased this morning as big four banks CBA, NAB and ANZ pass on last Tuesday’s 0.25 hike in full.

Westpac variable mortgage customers will see their rates rise on Tuesday (31 March).

When all four big banks’ new rates are in effect, Westpac will offer the lowest advertised variable rate out of the majors at 5.74%, while NAB and ANZ’s lowest variable rates are now in the 6s.

Big four banks’ lowest home loan rates, post March RBA hike | ||

|---|---|---|

Old rate from | New rate from | |

CBA | 5.59% | 5.84% |

Westpac* | 5.49% | 5.74% |

NAB | 5.94% | 6.19% |

ANZ | 5.75% | 6.00% |

Source: Canstar. Rates are for owner-occupiers paying principal and interest. LVR requirements apply. *Westpac rate effective 31 March.

CBA and NAB raise fixed rates as well

In addition to the variable hikes this morning, CBA and NAB have increased fixed rates by up to 0.30 and 0.35, respectively (see tables at end).

As a result of these changes, NAB no longer offers a fixed rate starting with a ‘5’.

Westpac now offers the lowest fixed rate out of the majors at 5.79% for a 1-year term, however, these fixed rates could rise in coming days.

Big four banks’ lowest fixed rates | ||||

|---|---|---|---|---|

CBA | Westpac | NAB | ANZ | |

1-year | 6.49% | 5.79% | 6.04% | 5.99% |

2-year | 6.34% | 5.89% | 6.09% | 6.04% |

3-year | 6.59% | 5.99% | 6.19% | 6.14% |

4-year | 6.64% | 6.09% | 6.19% | 6.19% |

5-year | 6.79% | 6.09% | 6.19% | 6.34% |

Source: Canstar.com.au. Rates based on owner occupier fixed rate loans. LVR requirements apply.

As a result of the hikes, Canstar analysis of owner-occupier rates shows:

Variable:

- 6.01% will be the average owner-occupier variable rate once all the lenders pass on the March rise.

- 5.75% will be a competitive variable rate, expected to be offered from around 40 lenders.

- 5.50% is likely to be one of the lowest variable rates on Canstar.

Fixed:

- 5.49% is the lowest fixed rate on Canstar, available from The Mac on a 2-year term.

- 2 lenders still offer fixed rates under 5.50%. One month ago, over 20 lenders had a fixed rate under 5.50%.

- 6.00% is the average of each lender’s lowest available 2-year fixed rate.

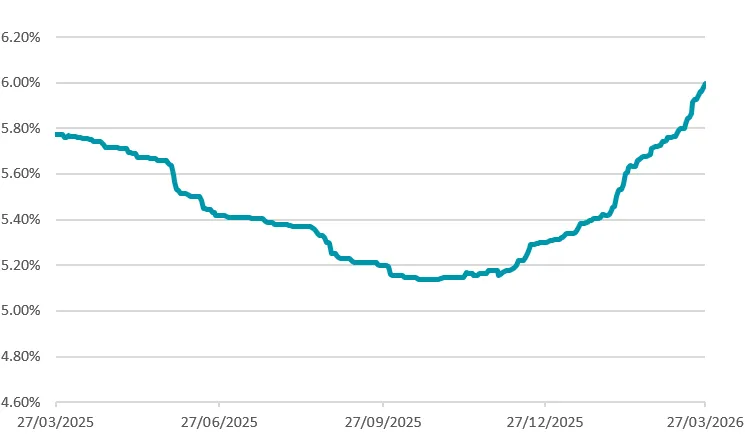

Average 2-year fixed rate – last 12 months

Rates rise from today but mortgage repayments will stay put for at least a couple of weeks

While the majority of borrowers will see their rate rise from this morning, those paying the minimum on their monthly repayments won’t see it increase straight away.

The big four banks send out letters via post and email with the following notice periods from the date of the letter:

- CBA: minimum of 20 days’ notice.

- Westpac, NAB and ANZ: minimum of 30 days’ notice.

What if you can’t meet the new repayment amount?

Borrowers who think they might not be able to afford their mortgage should take the following steps:

- Ask for a rate review. If you aren’t in a position to refinance, that doesn’t preclude you from asking for a rate cut from your own bank.

- If you secure a rate reduction, check your new minimum monthly repayments to see if you can clear this amount.

- If you can’t, call your bank, tell them you will have trouble meeting your new repayments and ask what your options might be. Do this before you miss a repayment.

- Get independent financial advice. The National Debt Helpline can help you get this advice for free.

What are some of the options the bank might offer?

Banks are required to offer support to customers struggling to meet repayments. Potential options for home loan support might include:

- Switching to interest-only for a year or two.

- Making reduced payments for a period of time.

- Extending your loan term.

While each of these options can help reduce a customer’s minimum monthly repayments, they can be very costly in the longer term. It’s important to get independent advice before going down this road.

Canstar’s data insights director, Sally Tindall, says, “Variable borrowers across the country are now having to brace for the second cash rate hike in as many months, while staring down the barrel of a potential third hike as soon as May.”

“Make no mistake, banks are starting to charge customers higher rates from today, but be aware there’s a significant delay between today and when that extra money comes out of your bank account, for those paying the minimum.

“Customers might think they’ve successfully accounted for two hikes, when in actual fact they might not have even started paying for the first one.

“If you’ve got a variable mortgage, understand what your new minimum monthly repayment is and make sure you can clear this amount.

“Be proactive: owner-occupiers should target rates below 5.75 per cent. If your rate starts with a 6, you’re still paying a loyalty tax to your bank.

“There’s almost certainly more pain ahead for borrowers, with all four big bank economists forecasting another 0.25 percentage point hike in May.

“If you’ve got a mortgage, work out what your repayments might look like if rates rose not just in May but again later in the year. You want to make sure this figure fits in your budget alongside the other rising cost-of-living pressures.

“Customers seriously considering fixing may need to act sooner rather than later. While this kind of decision should not be taken lightly, and not without proper research, the clock is ticking on competitive fixed offers.

“Just one month ago, there were more than 20 lenders offering at least one fixed rate under 5.50 per cent. Today, there’s just two left on the Canstar database. That’s a significant shift in just a matter of weeks.”

CBA changes to its lowest fixed rates | |||

|---|---|---|---|

Term | Old rate | New rate from | Change % pts |

1-year | 6.19% | 6.49% | +0.30 |

2-year | 6.04% | 6.34% | +0.30 |

3-year | 6.29% | 6.59% | +0.30 |

4-year | 6.34% | 6.64% | +0.30 |

5-year | 6.49% | 6.79% | +0.30 |

Source: Canstar.com.au. Notes: rates for owner-occupiers paying principal and interest. LVR requirements apply

NAB changes to its lowest fixed rates | |||

|---|---|---|---|

Term | Old rate | New rate from | Change % pts |

1-year | 5.74% | 6.04% | +0.30 |

2-year | 5.79% | 6.09% | +0.30 |

3-year | 5.84% | 6.19% | +0.35 |

4-year | 5.99% | 6.19% | +0.20 |

5-year | 6.09% | 6.19% | +0.10 |

Source: Canstar. Notes: rates for owner-occupiers paying principal and interest. LVR requirements apply.