Big four bank ANZ has today hiked fixed rates by up to 0.40 percentage points, just 19 days after the bank last lifted its fixed loans.

As a result, ANZ no longer has a fixed rate under 6%, with the lowest rate now 6.34% for a 1-year term.

Changes to ANZ’s lowest fixed rates

Term

Old rate from

New rate from

Change %-pts

1-year

5.99%

6.34%

+0.35

2-year

6.04%

6.39%

+0.35

3-year

6.14%

6.54%

+0.40

4-year

6.19%

6.54%

+0.35

5-year

6.34%

6.59%

+0.25

Source: Canstar - 1/04/2026. Rates based on owner-occupier fixed-rate loans. LVR requirements apply. Looking at the big four bank mortgage rates, Westpac still offers the lowest fixed rate out of the majors at 5.79% for a 1-year term.

Big four banks’ lowest fixed rates

CBA

Westpac

NAB

ANZ

1-year

6.49%

5.79%

6.04%

6.34%

2-year

6.34%

5.89%

6.09%

6.39%

3-year

6.59%

5.99%

6.19%

6.54%

4-year

6.64%

6.09%

6.19%

6.54%

5-year

6.79%

6.09%

6.19%

6.59%

Source: Canstar.com.au. Rates based on owner-occupier fixed rate loans. LVR requirements apply.

ANZ part of a broader fixed rate shift

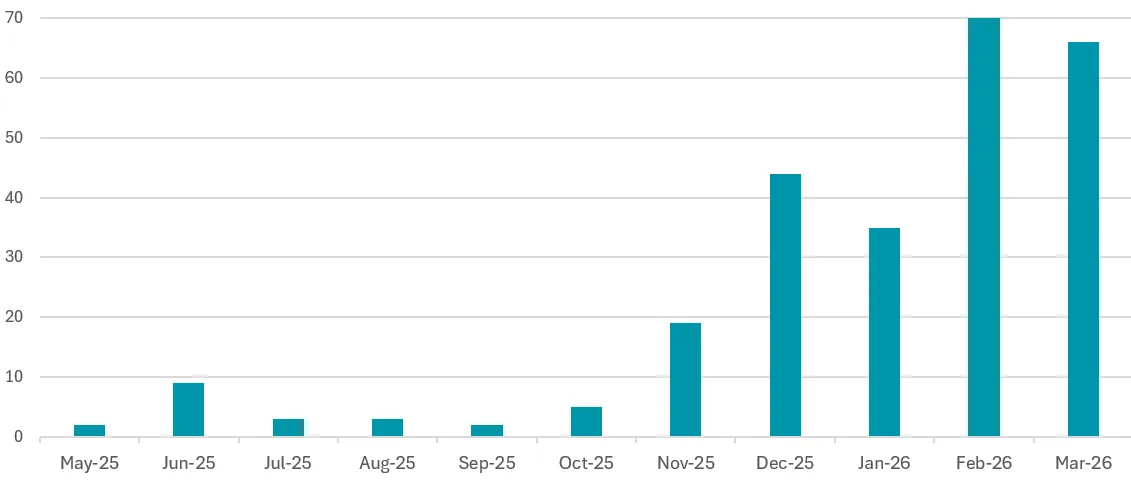

Rate tracking by Canstar shows 52 lenders have hiked at least one fixed rate since the last RBA hike just 15 days ago. This includes three of the big four banks – CBA, NAB and ANZ – but also Macquarie, Bendigo, ING and BOQ.

Lenders that have hiked at least one fixed rate per month

Source: Canstar.

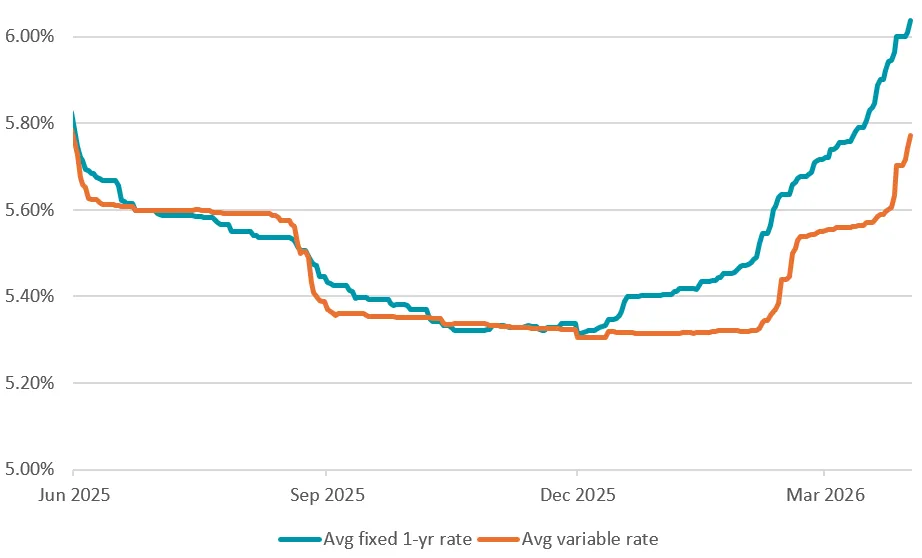

As a result of the hikes, the average 1-year fixed rate is now 0.27 higher than the average variable rate, a noticeable change from late last year when they were on par with each other.

Note: the averages are of the lowest available rates from each lender in the database.

Average rates: Variable vs 1-year fixed

Source: Canstar. Rates are the average of lenders’ lowest rates. Excludes green and introductory loans.

Lowest fixed rates also edging higher

As a result of the rate hikes, the lowest fixed rate is now 5.59% from Regional Australia Bank, Pacific Mortgage Group and Northern Inland Credit Union.

Lowest 1-year fixed rates

Lowest 2-year fixed rates

Lender

Lowest rate from

Lender

Lowest rate from

Regional Australia Bank

5.59%

Pacific Mortgage Group

5.59%

Pacific Mortgage Group

5.69%

Northern Inland Credit Union

5.59%

Transport Mutual

5.74%

Regional Australia Bank

5.64%

Source: Canstar. Rates based on owner occupier fixed rate loans. LVR requirements apply.

Have fixers missed the boat?

This will come down to the borrower, but also the future of the cash rate – something that, at this stage, is highly uncertain.

Canstar compared the average of the three lowest 1-year fixed rates (5.67%) against the average of the three lowest variable rates (5.56%) under a range of different cash rate scenarios.

Based on a $600,000 debt and 25 years remaining, if there were no more rate hikes, opting for one of the lowest variable rates could potentially see the person pay $659 less interest in the next 12 months.

However, if there is just one more rate hike, fixing comes out ahead in the 1-year term, saving about $586 in interest.

These scenarios are estimates and do not include fees or extra repayments.

Lowest 1-year fixed rate vs the lowest variable on a $600,000 loan

No. of 0.25% pt hikes

Which comes out on top after 2 yrs?

0 hikes

Variable by $659

1 more hike

Fixed by $586

2 more hikes

Fixed by $1,705

3 more hikes

Fixed by $2,573

Source: Canstar. Notes: based on an owner-occupier paying principal and interest with a $600k loan in April 2026 and 25 years remaining. Lowest rates are the average of the 3 lowest rates on the Canstar database. For variable rates, the average only includes those lenders that have passed on the March RBA hike. Assumes further hikes are in May, June and August 2026. Calculations are for illustrative purposes only. They only reflect the interest charges and do not include fees or any extra repayments. Lowest rates exclude eco and introductory rate loans.

ANZ far from alone in hiking fixed rates

Canstar data insights director, Sally Tindall, says, “Seeing ANZ’s lowest fixed rate jump to 6.34 per cent is a stark reminder of how quickly the interest rate tide has turned.”

“With over 50 lenders hiking fixed rates in just the last 15 days, it’s clear the market is pricing in further hikes to come, as the fallout from the war in the Middle East starts to hit costs across Australia.

“Fixed rates are typically the early warning signal for where rates are headed. When a bank ratchets them up twice in less than three weeks it’s a sign there’s a lot more turbulence ahead.

“ANZ is far from alone in hiking fixed rates. Three of the big banks have now hiked these rates in the space of five days. Westpac, now the lowest out of the big banks in the fixed rate space, is likely to be days away from lifting rates as well.

“Westpac’s own economists have ramped up their forecast of how many hikes we still have waiting in the wings, with the bank now predicting we’ll see another three in the next three RBA meetings.

“As a result, some borrowers could now be thinking about flipping over to fixed.

“If that’s you, take a clear-headed approach, weigh up the risks on both sides, keeping in mind the extra conditions and restrictions that come with locking in your rate.

“The cash rate could well rise again as soon as next month, but the fallout from the war, if it hits the Australian economy and jobs market hard, could also push the RBA into reverting back to cuts in the not too distant future.”

With nearly 20 years of experience across journalism and public relations, Laine Gordan excels at translating complex financial data into clear, compelling stories for everyday Australians. Before joining Canstar, she held senior editorial and research roles covering everything from banking and credit cards to budgeting and lifestyle.

As a strategic communicator and seasoned spokesperson, Laine specialises in spotlighting the trends that matter most—from interest rate movements to cost-of-living pressures. Her work aims to help Australians navigate the complexities of the financial landscape and take control of their personal finances.

Important Information

For those that love the detail

This advice is general and has not taken into account your objectives, financial situation or needs. Consider whether this advice is right for you.

This advice is general and has not taken into account your objectives, financial situation, or needs. It is not personal advice. Consider whether this advice is right for you. For more information, read Canstar’s Financial Services and Credit Guide (FSCG) and our detailed disclosure. Canstar may receive a fee for referring you to a product provider – for further information, see how we get paid. Payment of fees for ads does not influence our Star Ratings or Awards. Canstar is a comparison website, not a product issuer, so it’s important to check any product information directly with the provider. Consider the Product Disclosure Statement (PDS), Target Market Determination (TMD) and other applicable product documentation before making a decision to purchase, acquire, invest in or apply for a financial or credit product. Contact the product issuer directly for a copy of the PDS, TMD and other documentation. Canstar is an information provider and in giving you product information Canstar is not making any suggestion or recommendation about a particular credit product or loan. If you decide to apply for a credit product or loan, you will deal directly with a credit provider, and not with Canstar. Rates and product information should be confirmed with the relevant credit provider. For more information, read the credit provider’s key facts sheet and other applicable loan documentation for that product. Read the Comparison Rate Warning.

Research provided by Canstar Research AFSL and Australian Credit Licence No. 437917. Canstar Pty Ltd AR 443019 CR 538715.

a. The views, opinions, and positions expressed in this piece are the views of the author(s) alone, and do not necessarily reflect the views of Canstar.

b. The views, opinions and advice quoted in this piece are those of the author(s) or interviewee(s) expressing them, and do not necessarily reflect the views of Canstar. Any other views expressed and advice given by Canstar or its employee(s) in the above article are not necessarily those of the same author(s) or interviewee(s).

The examples provided in the article are not based on actual products or real consumer circumstances. The information in this article is of a general nature only, and does not take into consideration your objectives, financial situation or needs. It is not personal advice, and you should not rely on it, even if the example is similar to your own circumstances. You should make your own enquiries and calculations based on your own personal circumstances as well as finding out specific product costs, rates or features that may be relevant to you. You should consider seeking independent advice before making a purchase, credit, or investment decision.