Investing For Beginners | Part 3: Markets

Investing can be a bamboozling topic for some people but like many complex things, if you break it down into smaller components it can become easier to get your head around.

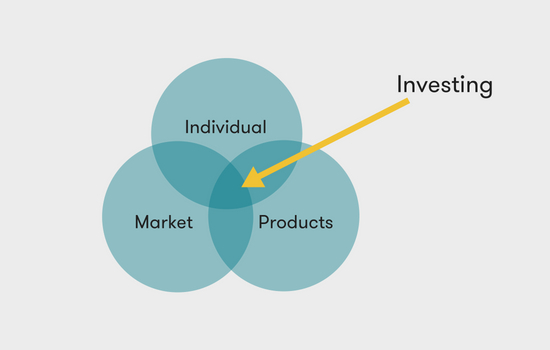

That has been the purpose of this investment series for beginners, as I’ve broken down the concept of investing into three parts: the individual, products and market.

Part one of this series spoke about the consumer and part two provided a cook’s tour of investment products. In this third and final instalment, we’ll look at the market dynamics and how it all comes together in an investment portfolio.

Individual markets

Effectively a ‘market’ is quite simply where buyers and sellers come together to agree on the price of an asset. In the case of stocks, that’s done via an exchange like the ASX, whereas residential property and other assets may be exchanged directly between the two parties.

We covered it in a little more detail in part two of this series, but the market dynamics of a product determine things like the risk (in terms of volatility) and liquidity.

Generally speaking, high risk is driven by the surety of the valuation of a product. A term deposit, for example, is generally very low risk as the terms of the investment are all known up front. The value of a share on the other hand is subject to a number of factors that require investors to include objective measures into their assessment and as a result, the market value can change dramatically.

Liquidity on the other hand, is determined by demand for the product and ease of access. Perhaps an easy way to demonstrate this is in the share market with stocks like Commonwealth Bank or BHP, where the daily value of shares exchanged is in the hundreds of millions. Conversely, small companies can have days where no shares are exchanged at all.

In Australia, one of the drivers of that demand is our superannuation system. According to APRA in the 12-month period ending March 2018, there was over $38 billion in superannuation contributions in Australia. All of that money has to go somewhere, and due to the way super funds invest, it makes for a relatively liquid market in quality assets such as blue-chip shares and government bonds.

Market relationships

Where this gets interesting is the interplay between products and the assets underneath them. Having a mix of products in a portfolio can help to create a more stable return and potentially increase the long-term effect of compounding.

A classic example of two markets that usually move in the opposite direction of each other is shares and bonds. There was a recent period where they both correlated (moved in the same direction together), but over the long term typically when the share market goes up, bond values go down and vice versa.

This is basically due to economic cycles and the flow of money around the market looking for yield. In a growing economy, companies also tend to grow and as a result, investors enter the share market to capture some of that growth. At the same time, inflation tends to increase and therefore central banks respond by increasing interest rates. As interest rates increase, the value of bonds tend to decrease (check out the explainer here), and so shares typically go up while bonds go down. The opposite is generally also true.

The goal for many investors is to build a portfolio of assets that behave differently in different economic environments. Exposure to different risks should mean that you won’t have a single point of failure that can bring your investment portfolio unstuck. This can be achieved by holding various types of products with exposure to various markets in various geographies. In the investment world, this is known as diversification. You can find more on that here.

Bringing it all together

Now’s the part where I take these three elements of investing that I’ve briefly covered and put them together into a neat little package that you can go away and implement… impossible!

However, if I’ve done my job, then this short series has pointed you to a few key areas of investing for you to explore further.

In this series we’ve covered:

Part 1. The Individual – consider your investment goals, risk tolerance, time horizon, liquidity requirements and how much you’re investing in order to frame up your expectations and requirements.

Part 2. Products – at the very core of investing is the concept of the risk-return trade-off. Investors need to consider this when choosing asset classes and products to ensure that it matches their individual needs.

Part 3. Markets – product characteristics are largely determined by the markets that they operate in. Understanding how the market behind a product operates should help investors recognise economic cycles and external factors that may affect the value of a product.

These elements should all come together to form an investment portfolio.

During your investigation into investing you may feel yourself going down a rabbit hole and if that rabbit hole gets too complex, don’t give up! Take a step back, find another source and start searching for the answers there.

This article was reviewed by our Content Producer Marissa Hayden before it was updated, as part of our fact-checking process.

Try our Investor Hub comparison tool to instantly compare Canstar expert rated options.