First Home Buyer Survey 2022

First Home Buyer Survey

July : 2022

From stress levels to savings barriers, a new Canstar survey reveals the top trends among prospective first home buyers planning to crack the property market.

Soaring living costs, stagnant wage growth and skyhigh house prices are causing an alarming number of first home buyers to feel stressed about scraping a house deposit together, according to new research from Australia’s biggest financial comparison site¹, Canstar.

Canstar’s new First Home Buyer Survey of 679 Australians found a staggering 42% feel very or extremely stressed about building a big enough house deposit to purchase a home and a further 48% feel somewhat stressed. This equates to 90% of first time buyers anguishing over their ability to save.

When looking at the price range in which they plan to purchase, close to two thirds (63%) of first home buyers are aiming for a home valued between $400,001 to $800,000, 16% are planning to spend $400,000 or less, while 21% have their eye on a property worth more than $800,000.

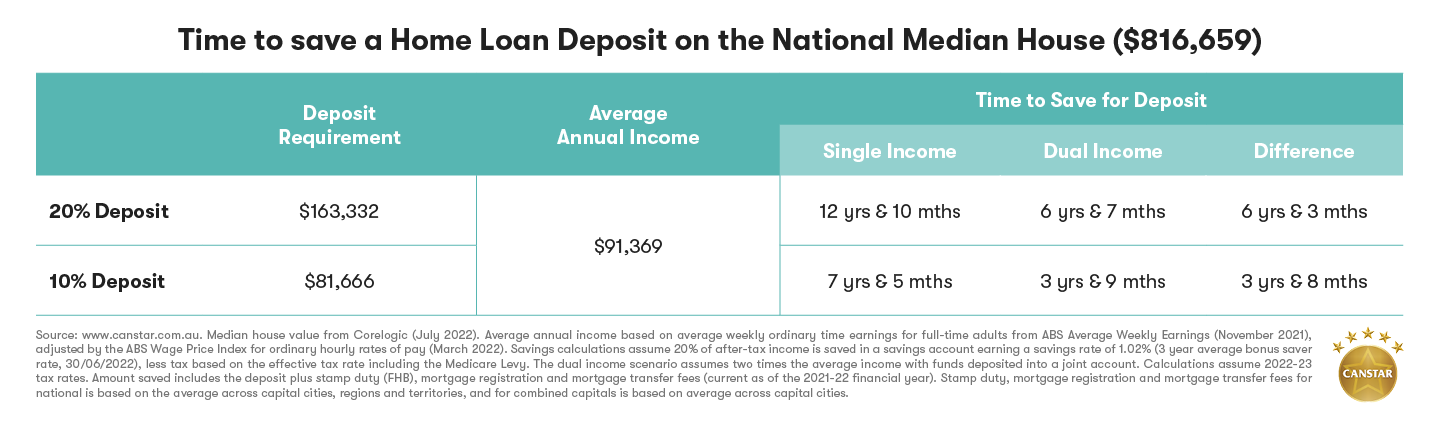

First home buyers are fairly evenly split when it comes to deposit size, with 36% aiming to save a deposit of up to 10%, and 37% planning to save a 11%-20% deposit. With the national median house price sitting at $816,659 according to CoreLogic, first home buyers would need to scrape together $81,666 for a 10% deposit and $163,332 for a 20% deposit, Canstar analysis shows.

Canstar’s Editor-at-Large and Money Expert, Effie Zahos, says, “There’s a few market forces working against first home buyers right now but like other buyers before them, there’s always going to be a way to buy.”

“Faced with costly living expenses, rising rents, sky high property prices, lower borrowing limits and all of this coupled with little to no wage growth, first time buyers can be discouraged from thinking it’s possible to buy in today’s market.

“A saving grace is property prices are starting to fall and buyers will be looking at the trade-off between lower prices and higher mortgage costs compared to rising rents. Striking while the iron is hot and prices are off the boil could be the sweet spot for first home buyers as long as they take a realistic view of the market and buy what they can afford.

“Saving a 20 percent deposit for an $800,000 house could put anyone off when they realise it could take them more than a decade to reach that goal. Switching focus to a unit in an entry level suburb with a lower price point to cut the time to save will still be challenging, but it can mean getting on the ladder sooner.”

Bills, rent and brunches: The top three barriers to saving

Close to two thirds (62%) of prospective first home buyers put money towards their house deposit each month, setting aside $1,417 on average. However, just under one third (31%) don’t know how much they’re saving, while a worrying 7% aren’t saving anything.

The top three measures preventing first home buyers from growing their house deposit quicker are bills and household expenses (59%), rent (53%) and going out and/or eating out (43%).

![]()

This suggests key obstacles to saving stem from both factors beyond their control, such as living costs, as well as personal lifestyle choices, explains Zahos.

“Rising living costs and surging rents mean first home buyers are facing an uphill battle when it comes to their savings. Property affordability remains a major obstacle first home buyers are desperately trying to overcome, which certainly isn’t easy given wage growth remains slow,” says Zahos.

“Consistency is key for anyone wanting to grow their house deposit savings, and it’s important to look for ways to cut back wherever possible. While the notion of expensive cafe breakfasts has been a major point of contention in the property affordability debate, Canstar’s research shows our food delivery habits and eating out is in fact a major savings barrier for many prospective buyers.

“Potential buyers who are serious about saving need to create a bare bones budget to supercharge their savings. It’s possible to do this a number of ways. One way is to change your living situation such as moving from renting a house to a unit, which in Canberra could bring in an immediate saving of $186 per week or $132 per week in Sydney and a saving of $51 each week in Melbourne².

“Another way to save is cutting back on everyday expenses. One less meal delivery, store-bought coffee and cafe breakfast each week could save you around $55, or close to $3,000 in a year. It’s not to be sniffed at. Earning an extra $3,000 per year on the average weekly full-time earnings of $1,748³ would mean working an extra two weeks, the equivalent of half your annual leave each year.”

Bank of Mum and Dad tightens the purse strings

Despite being hailed as one of Australia’s most generous lenders – at least anecdotally – the Bank of Mum and Dad appears to have tightened the purse strings.

Canstar’s survey found the majority (79%) of first home buyers aren’t receiving any financial contributions from a parent or family member to help get their deposit over the line, compared to just 21% who are.

“The bank of mum and dad is likely to be shut for some time. With super funds delivering negative returns for the first time in 13 years, inflation yet to peak and interest rates continuing to rise, many parents will be forced to focus on their own financial scorecard. First home buyers can either sit back and wait for mum and dad’s support or use this time effectively to surcharge their savings,” says Zahos.

Nearly three quarters (70%) of first home buyers are seeking help elsewhere having applied or are planning to apply for a state or Federal government first home buyer grant or scheme to help with their purchase.

First home buyers aren’t all coupled up either – the survey results found that while 51% are planning to buy with one other person, a surprising 45% are flying solo and intend to snap up a property on their own. A further 3% are purchasing with multiple people and 1% are unsure who they are buying with at this stage.

Zahos explains, “It would take a dual income couple over six and a half years to save a 20 percent deposit for the national median house price of $816,659, while a single buyer would take close to 13 years. Even a 10 percent deposit would take a couple almost four years and a single more than seven years. This is a long time to be saving, and it’s easy to see how buyers could become disheartened as living costs rise.”

Zahos adds, “The recent government announcements around extensions to home buyer grants should hopefully improve the situation for some buyers and speed up the buying process, especially for those going it alone without a cash boost from family members.”

“Other ways prospective first home buyers can grow their deposit quicker is to put any bonuses or windfalls towards your savings, avoid lifestyle creep if you get a pay rise, and make simple swaps where possible.

“You should also have a dedicated savings account with the highest interest rate available, and keep your deposit savings out of sight to avoid the temptation to dip into them. With savings account interest rates rising, the returns will start doing some of the heavy lifting rather than contributions.”

![]()

First home buyers are encouraged to download Canstar’s free Bright Starters Report that identifies the most affordable and promising locations for first home buyers with a list of more than 100 ‘Bright Starter’ towns and suburbs.

For further information:

Belinda Williamson

Group Manager, Corporate Affairs

Ph: 0418 641 637

Belinda.williamson@canstar.com.au

Notes to Editors

¹ Please refer to: www.canstar.com.au/biggest-original

² CoreLogic’s Quarterly Rental Review for Q2 2022

³ ABS Average Weekly Earnings, Australia, November 2021