What Business Owners Need To Know In 2017

Running a small business – or a large one? Here’s what business owners need to know about business loans and business overdrafts in 2017, based on Canstar’s expert ratings and analysis.

The latest ABS data shows the number of actively trading businesses is on the rise, with an increase of 2.4% from 30 June 2015 to end June 2016 (ABS, 2017). With more than 2.1 million businesses actively operating in Australia, it’s more important than ever for business owners to find the products that will help their businesses grow.

Canstar is here to help, releasing our 2017 expert star ratings of term loans and overdrafts, along with our analysis of the current state of the market for businesses in Australia. We look at the current fees and interest rates, the current business lending pledges from major lenders, and more business lending trends in 2017.

Business loan interest rates in 2017

Canstar has observed the following movements in advertised business loan interest rates in 2017:

| Business Loans – Overview of Reference Rate Movements | |||||||

|---|---|---|---|---|---|---|---|

| Profile | Loan Amount | No. of Movements | Average Movement | Increases | Average Increase | Decreases | Average Decrease |

| Commercially Secured – Overdraft | $50,000 | 22 | -0.30 | 0 | n/a | 22 | -0.30 |

| Residentially Secured – Overdraft | 20 | -0.41 | 0 | n/a | 20 | -0.41 | |

| Commercially Secured – Term Loan | $250,000 | 27 | -0.28 | 2 | 0.30 | 25 | -0.33 |

| Residentially Secured – Term Loan | 26 | -0.40 | 1 | 0.05 | 25 | -0.42 | |

| Commercially Secured – Overdraft | $125,000 | 22 | -0.30 | 0 | n/a | 22 | -0.30 |

| Residentially Secured – Overdraft | 20 | -0.41 | 0 | n/a | 20 | -0.41 | |

| Commercially Secured – Term Loan | $500,000 | 27 | -0.28 | 2 | 0.30 | 25 | -0.33 |

| Residentially Secured – Term Loan | 26 | -0.40 | 1 | 0.05 | 25 | -0.42 | |

| Source: www.canstar.com.au | |||||||

| Based on reference rates for the relative loan amounts, security and product type. | |||||||

It would be difficult for Canstar to show minimum, maximum, and average interest rates for business lending, because it all depends on the loan’s risk margin applied.

But we will say this – the market is currently offering largely the same interest rates across the board, although it may not look like it. Don’t be confused by the varying interest rates advertised by lenders.

For example, if you see a business loan with an advertised rate of 4% p.a., and a loan with a different lender that has an advertised rate of 10% p.a., you can’t assume that 4% p.a. is a better deal as there may be a margin applied. A loan with a lower advertised rate may have a higher margin applied so that the business might pay around 7% p.a., while a loan with a higher advertised rate may have a negative margin applied so that the business pays roughly the same 7% rate.

We have more information on how business loan margins work and how advertised rates work in the other articles on our site.

Fees on business loans in 2017

The following fees apply to business loans and overdrafts on the Canstar database in 2017:

| Upfront Fees | ||||

|---|---|---|---|---|

| Type | Loan Amount | Minimum | Average | Maximum |

| Commercially Secured – Overdraft | $50,000 | $125.00 | $596.30 | $820.00 |

| Commercially Secured – Overdraft | $125,000 | $312.50 | $788.91 | $1,500.00 |

| Residentially Secured – Overdraft | $50,000 | $125.00 | $607.86 | $820.00 |

| Residentially Secured – Overdraft | $125,000 | $312.50 | $759.05 | $1,250.00 |

| Commercially Secured – Term Loan | $250,000 | $0.00 | $1,090.24 | $2,500.00 |

| Commercially Secured – Term Loan | $500,000 | $0.00 | $1,941.43 | $5,000.00 |

| Residentially Secured – Term Loan | $250,000 | $0.00 | $1,136.00 | $2,500.00 |

| Residentially Secured – Term Loan | $500,000 | $0.00 | $2,011.00 | $5,000.00 |

| Ongoing Fees | ||||

| Type | Loan Amount | Minimum | Average | Maximum |

| Commercially Secured – Overdraft | $50,000 | $0.00 | $443.89 | $860.00 |

| Commercially Secured – Overdraft | $125,000 | $120.00 | $953.67 | $2,150.00 |

| Residentially Secured – Overdraft | $50,000 | $120.00 | $453.41 | $860.00 |

| Residentially Secured – Overdraft | $125,000 | $120.00 | $970.67 | $2,150.00 |

| Commercially Secured – Term Loan | $250,000 | $0.00 | $255.00 | $480.00 |

| Commercially Secured – Term Loan | $500,000 | $0.00 | $255.00 | $480.00 |

| Residentially Secured – Term Loan | $250,000 | $0.00 | $237.33 | $480.00 |

| Residentially Secured – Term Loan | $500,000 | $0.00 | $237.33 | $480.00 |

| Source: www.canstar.com.au

Fees based on relative loan amounts and product types or security. |

||||

Learn more about the fees you can expect to pay on business loans and overdrafts.

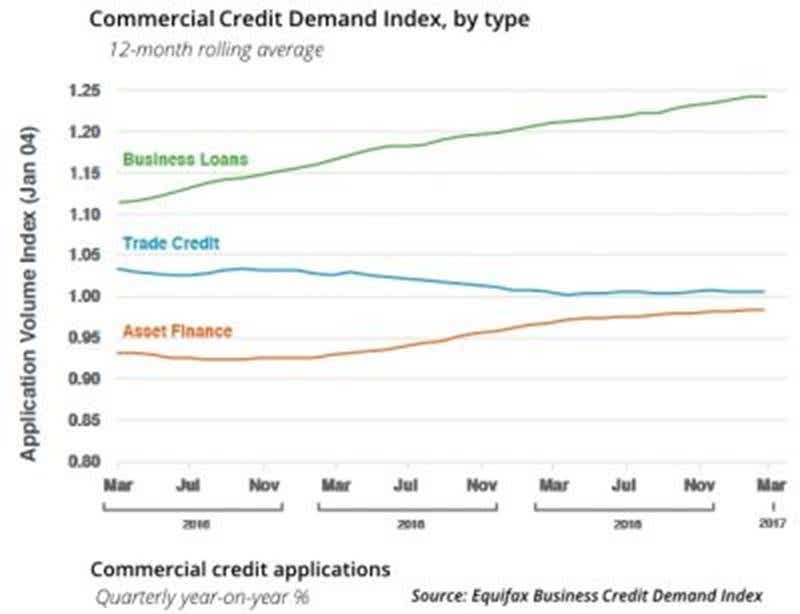

Business lending is up in 2017

Business lending has seen a 1.6% year-on-year increase in the March 2017 quarter, according to the latest Business Credit Demand Index from credit reporting agency Equifax.

The March 2017 quarter compared to the March 2016 quarter showed year-on-year increases in the number of applications for business loans (3.4%) and asset finance applications (1.8%).

Source: Equifax Business Credit Demand Index

Most interestingly, commercially secured mortgage applications rose a staggering 25.7% year-on-year, including loans secured by everything from warehouses and factories to investment properties.

“This activity is driven in large part by the fact that interest rates remain at record lows, encouraging the investment housing boom to continue, despite regulators’ attempts to cool the market,” explains Neil Shilbury, general manager of commercial and property products at Equifax.

Shilbury added that Australia’s economy is showing signs of improvement despite the slow collapse of the mining boom.

“According to the Reserve Bank of Australia’s assessment, Australia is now 90% of the way back to normal levels of business investment from the peak in mining investment in 2012,” Shilbury told Roy Morgan Research.

Business lending pledges by major lenders in 2017

Some of the major lenders have offered significant pledges to lend to businesses in Australia in 2017.

ANZ has upped their effort in business lending by pledging $2 billion in lending to small businesses. Throughout 2014, during their last business pledge of $1 billion, ANZ approved 74% of loan applications during this period. The usual credit approval criteria apply to loans and overdrafts from ANZ.

NAB offered a similar pledge campaign in 2016, pledging to lend $2 billion per month to Australian businesses large and small. This doubled their 2015 pledge of $1 billion.

NAB Group Executive for Business Banking, Angela Mentis, said, “Now, more than ever, Australians are focused on the future.

“Businesses across the country are energised by the renewed focus on a prosperous and productive economy powered by innovation and agility.

“From my time on the road meeting with our customers it is clear there is strong entrepreneurial drive and desire to innovate as businesses look to take their services and expertise to the rest of Australia and beyond.”

Innovation research by NAB in 2015 found that Australian businesses that identify as ‘highly innovative’ are stronger performers, both in terms of business conditions and levels of confidence.

“The improvement in confidence levels and sustained level of business conditions echo the faith we have in Australian business, and supporting them remains our biggest priority,” said Ms Mentis.

Credit cards for start-ups

The latest ABS data shows that more new businesses entered the market in 2015-16 than in the year before (14.6% compared to 13.4%) – and the times are a-changin’ when it comes to start-up funding.

The latest Startup Muster 2016 Annual Report from the Department of Industry, Innovation and Science shows that more start-ups are getting started with a business credit card than a traditional business loan.

Around 15% of startups receive funding from credit cards, while a bank loan sits at close to half of that at 8.2% (Startup Muster).

It’s worth start-ups considering the case for a business credit card versus a business loan. There are some high-profile cases of companies that have started up off the back of a simple business credit card.

One example is Atlassian, the creators of project management, collaboration, and coding software including JIRA, Confluence, Trello, HipChat, and more.

Naturally, there are pros and cons to consider for different types of business lending. While a credit card is easier for a business to obtain than a loan or overdraft facility, a business loan or overdraft can generally offer a much higher credit limit.

If you’re not yet at the stage of applying for a credit card or a business loan, consider the business start-up accelerator and incubator programs on offer in Australia in 2017. These programs can give your business idea the boost it needs to launch as a fully-fledged business.

What to look for in a business loan or overdraft

First, you need to choose the type of product you need – whether a business loan or business overdraft – then consider which lenders meet your requirements. Thankfully, Canstar can help you there.

If you’re looking for business credit, consider the top 5-star rated business loans and overdrafts listed in our latest star ratings. In general, look for a business lending product that:

- Suits your long-term vs short-term business purpose:

- Long-term: Term loans are best suited for asset purchases such as equipment, vehicles, and real estate.

- Short-term: Overdrafts are best suited for financing temporary liabilities such as inventory and accounts payable.

- Features that suit your business needs:

- Term Loan: Look for features such as redraw facilities, portability (ability to switch the security of the loan), repayment options and flexibility, split loan facilities, and the ability to switch between a variable or fixed interest rate.

- Overdraft: Look at what type of fees the transaction account attached to the overdraft will attract against the transactions your business needs to make.

- Functionality of the product: Look for portability (ability to switch security), the number of free transactions allowed, any withdrawal limits, and anything else your business may need.

Find out what other business owners are looking for in a business loan or overdraft, based on Canstar’s database of business owners comparing products using our website.

Canstar compares business loans and business overdrafts based on a number of factors including:

- Interest rates (base rate with negative/positive margin)

- Upfront, ongoing, and discharge fees

- Minimum loan amount required

- Repayment frequency allowed

- Options for interest only payments or interest payments when in credit

- Redraw facility

- Lump sum repayments allowed

- Repayment holidays allowed if additional payments made in advance

- Split interest rate option available

- Switch from variable rate to fixed rate allowed

- Overdraft functionality including overdraft service fee and number of free transactions

See our comparison table below for a snapshot of the current 5-star business loans available for a loan amount of $250,000, secured by a commercial property in NSW.

Business Loans

Business Overdrafts

Compare business loans and business overdrafts using our website and filter your search to find a 5-star rated business lending option:

Read our detailed Business Loans & Overdrafts Star Ratings Methodology to understand why a loan or overdraft might receive a 5-star rating for a particular business lending profile.

Discover more trends businesses need to know about in 2017 with our latest star ratings report:

Business Loans & Overdrafts Star Ratings - Canstar

Important Notes:

The Star Ratings in this table were awarded in April 2017. The search results do not include all providers and may not compare all features relevant to you. View the Canstar Business Loans & Overdrafts Star Ratings Methodology and Report. The rating shown is only one factor to take into account when considering products.

To the extent that the information in this article constitutes general advice, this advice has been prepared by CANSTAR Research Pty Ltd A.C.N. 114 422 909 AFSL and ACL 437917 (“CANSTAR”). The information has been prepared without taking into account your individual investment objectives, financial circumstances or needs. Before you decide whether or not to acquire a particular financial product you should assess whether it is appropriate for you in the light of your own personal circumstances, having regard to your own objectives, financial situation and needs. You may wish to obtain financial advice from a suitably qualified adviser before making any decision to acquire a financial product.

CANSTAR provides information about financial products. It is not a product provider and in giving you information it is not making any suggestion or recommendation to you about a particular product. If you decide to apply for a business loan or overdraft, you will deal directly with a financial institution, and not with CANSTAR. Rates and product information should be confirmed with the relevant financial institution. For more information, read our detailed disclosure, important notes and additional information. Read the comparison rate warning.

All information obtained by CANSTAR from external sources is believed to be accurate and reliable. Under no circumstances shall CANSTAR have any liability to any person or entity due to error (negligence or otherwise) or other circumstances or contingency within or outside the control of CANSTAR or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication, or delivery of any such information. Copyright 2014 CANSTAR Research Pty Ltd A.C.N. 114 422 909. The word “CANSTAR”, the gold star in a circle logo (with or without surmounting stars), are trademarks or registered trademarks of CANSTAR Pty Ltd. Reference to third party products, services or other information by trade name, trademark or otherwise does not constitute or imply endorsement, sponsorship or recommendation of CANSTAR by the respective trademark owner.

Products displayed above that are not “Sponsored” are sorted by Star Rating and then alphabetically by company. CANSTAR may receive a fee for referral of leads from these products. See How We Get Paid for further information.

The table above does not include all providers and may not compare all features relevant to you. View the CANSTAR Business Loans and Overdrafts Star Ratings Methodology and full report.