Business Loan Report For 2014

Written by

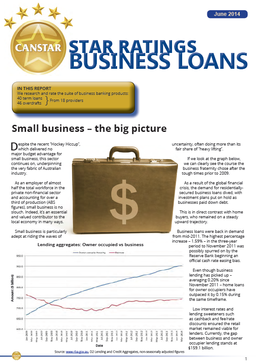

In this report we research and rate the suite of business banking products: 40 term loans, 46 overdrafts from 18 providers.When it comes to loans, what does small business require from financial institutions?

Obviously, a competitively-priced product is essential; however there are more considerations than just the interest rate when it comes to determining outstanding value for money. Canstar considers the following features, among others, to be important components of determining value.For both

1. Lending terms – The basic conditions of the loan such as minimum and maximum amounts and term;

2. Loan purposes availability – The different purposes for which the loan is available;

3. Security accepted – The types of equity that can be used as security;

4. Online security – Additional security features such as secondary authentication that keeps your money safe;

5. Portability – the option to transfer a loan from one security to another.For term loans

1. Redraw facility – The ability to withdraw additional payments from the loan;

2. Relationship bonus – Additional discounts or bonuses that may be available;

3. Repayment capabilities – How additional repayments can be made and any limits that apply;

4. Split & switching facility – The ability of a loan to be split or switched between fixed and variable as well as the fees applicable.For overdrafts

1. Overdraft terms – the transaction accounts that are linked to the overdraft, in particular the functions and transaction costs.

Obviously, a competitively-priced product is essential; however there are more considerations than just the interest rate when it comes to determining outstanding value for money. Canstar considers the following features, among others, to be important components of determining value.For both

1. Lending terms – The basic conditions of the loan such as minimum and maximum amounts and term;

2. Loan purposes availability – The different purposes for which the loan is available;

3. Security accepted – The types of equity that can be used as security;

4. Online security – Additional security features such as secondary authentication that keeps your money safe;

5. Portability – the option to transfer a loan from one security to another.For term loans

1. Redraw facility – The ability to withdraw additional payments from the loan;

2. Relationship bonus – Additional discounts or bonuses that may be available;

3. Repayment capabilities – How additional repayments can be made and any limits that apply;

4. Split & switching facility – The ability of a loan to be split or switched between fixed and variable as well as the fees applicable.For overdrafts

1. Overdraft terms – the transaction accounts that are linked to the overdraft, in particular the functions and transaction costs.