Growth And Recovery Of Business Banking After The Global Financial Crisis

business-recovery-still-to-emerge "> Business recovery still to emerge

Business recovery still to emerge

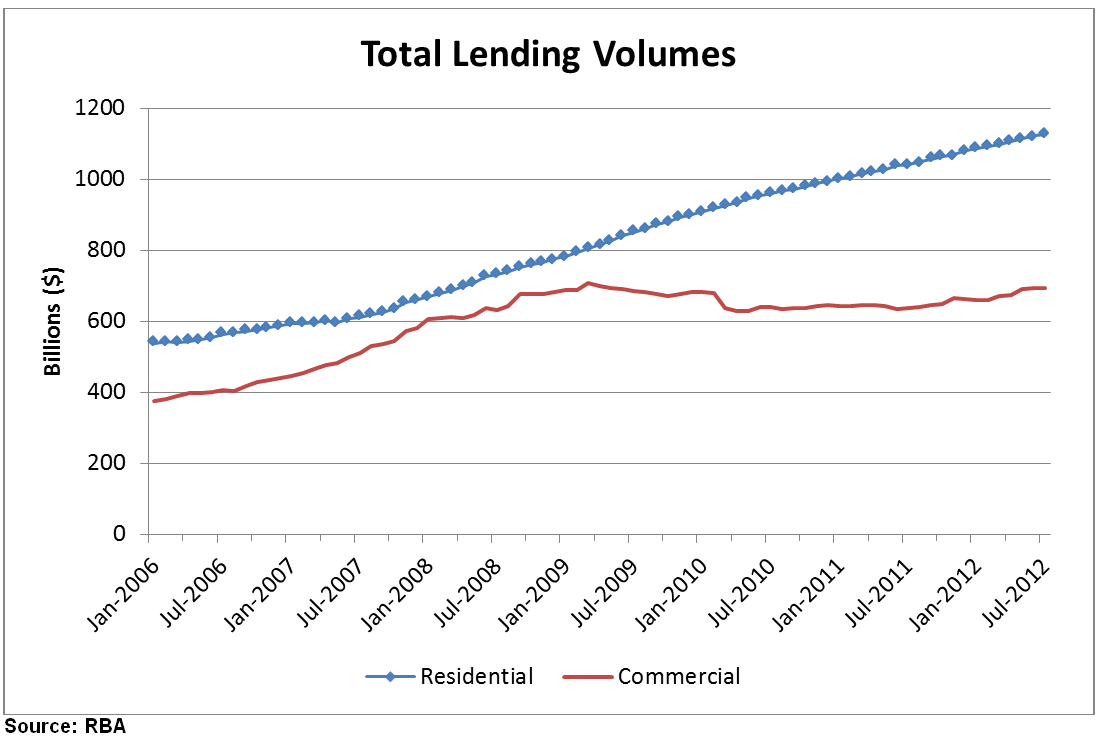

A look at the chart below confirms commercial lending continues to remain in the doldrums. With business confidence being lacklustre and the bank?s risk appetite appearing to be fragile it appears that an economic recovery remains some time off.

The graph shows that from the start of 2006 through to 2008 business lending was trending upwards at a much faster pace than residential loans. These were heady times it seemed economic growth would never end and the only way for house prices was up.

At this time residentially secured business base rates were at parity with home loans and bankers were actively marketing to small business.

However, not long after October 2008, the risk appetite for new business lending evaporated and small business owners suddenly found it much more difficult to obtain finance. For the ?lucky? ones that were approved their borrowing rates became more expensive.

By Oct 2009 small business base rates were 1.19% higher than standard variable home loan rates and almost 4% above the cash rate. In addition, customer risk margins are added to the base rate and the banks, now risk adverse, were increasing these as well.

Three years on and business base rates remain 4% above the official cash rate (excluding the customer margin). However, there has been a narrowing of the margin compared to the standard variable home loan rate which is now 0.74%.

The latest RBA data shows an increase in business lending from February to July 2012 but it would seem that a strong upward trend remains sometime away.

business-looking-forward,-looking-back">Business looking forward, looking back

A healthy recovery is a two way street. Businesses looking towards the future must be accommodated by willing lenders so appropriate opportunities and investments can be made to keep the economy moving forward at all levels.

It’s doubtful, however, that business lending will quickly outstrip home loan lending again.

During the GFC we heard many complaints of credit availability drying up for small businesses, as well as small businesses facing sudden re-risk rating, requiring them to provide greater security for their loans, or pay higher rates.

On the other hand, the Australian Bankers? Association has been vocal in citing cost of funding and increased risk as contributors to the cost of business finance.

what’s-good-for-business?">What’s good for business?

Keeping a close eye on cashflow is an essential part of operating a business. Monitoring ingoings and outgoings and switching to better, more cost-effective ways of doing things also includes banking. How do your current banking accounts stack up? Is there an easy alternative that will save you money?

It’s very unlikely anyone on the payroll has the time to compare the myriad of business banking products on offer. The number of products in the market is sizeable, which can make product comparisons an exhaustive task.

That’s why the CANSTAR business banking star ratings are so valuable. We assess business credit cards, deposit accounts and loans covering residential and commercial lending for both term loan and overdraft categories.

We compare rates and features to award five stars to products that offer outstanding value. This enables you to make an informed choice of suitable banking products, even if it is just to see how competitive your bank is.

Article updated 12/09/2012

Business recovery still to emerge

Business recovery still to emerge