What is risk aversion?

When you invest you have to understand the risks involved and assess what level of risk you are comfortable taking on. We explain risk tolerance and what it means to be risk averse.

What is risk aversion?

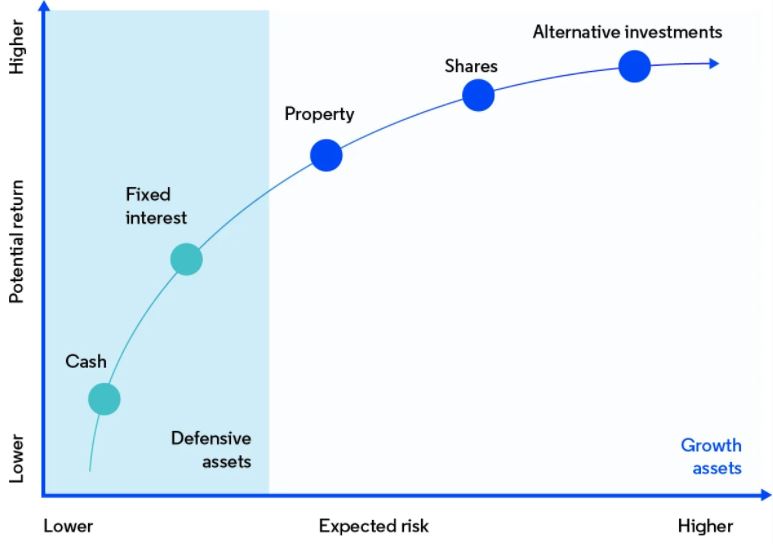

Those who are risk averse are generally willing to accept lower returns for less risk and volatility, over potentially higher returns with unknown risks and more volatility. For example, a risk averse investor will likely be more comfortable investing in defensive assets, such as cash or fixed interest products, as opposed to growth assets like property or shares. Or, if they do invest in shares they are likely to prefer stable blue chips stocks over more volatile stocks.

Source: MoneySmart.gov.au

Is risk aversion good for investors?

Investing is very personal and when you invest you have to consider your risk tolerance. Some investment products can be very risky and although they have the potential for higher returns, for some investors experiencing the highs and lows of the market may not be worth it. There are ways to make your money work harder for you without taking on too much risk. The best level of risk to adopt is one that doesn’t keep you up at night.

Related article: What are the different financial risks?

Risk vs reward

The risk/reward trade-off is an important part of investing and is a concept that all investors should understand. The trade-off for the potential of greater returns is adopting a great level of risk. And, if you choose to play it safe, often you have to accept the possibility of lower returns. Identifying your tolerance for risk can help you determine the products to invest in and your investment strategy.

How to determine your risk tolerance

When considering your risk tolerance there are two things to ask yourself:

How long do you plan on investing?

If your time horizon is relatively short, the volatility often seen in growth assets like stocks, may see you have to liquidate your investment at a loss. For example, someone saving for their first home with a time horizon of five years might be attracted to a high growth asset like shares, as it could potentially maximise your deposit. However, the risk is that just before achieving their goal, the market hits a downturn which puts them back a whole year in savings. Whereas, if you have a longer time to invest, those downturns can be overcome by subsequent rallies in the market.

What is the amount of money you can stand to lose?

If you only invest the money that you can stand to lose, you might find it less tempting to respond to a downturn in the market and be more level-headed when investing. Often, the more money you have the greater risk you can take. However, at the end of the day you should be comfortable with the amount you’ve invested.

Cover image source: Halfpoint

Try our Investor Hub comparison tool to instantly compare Canstar expert rated options.